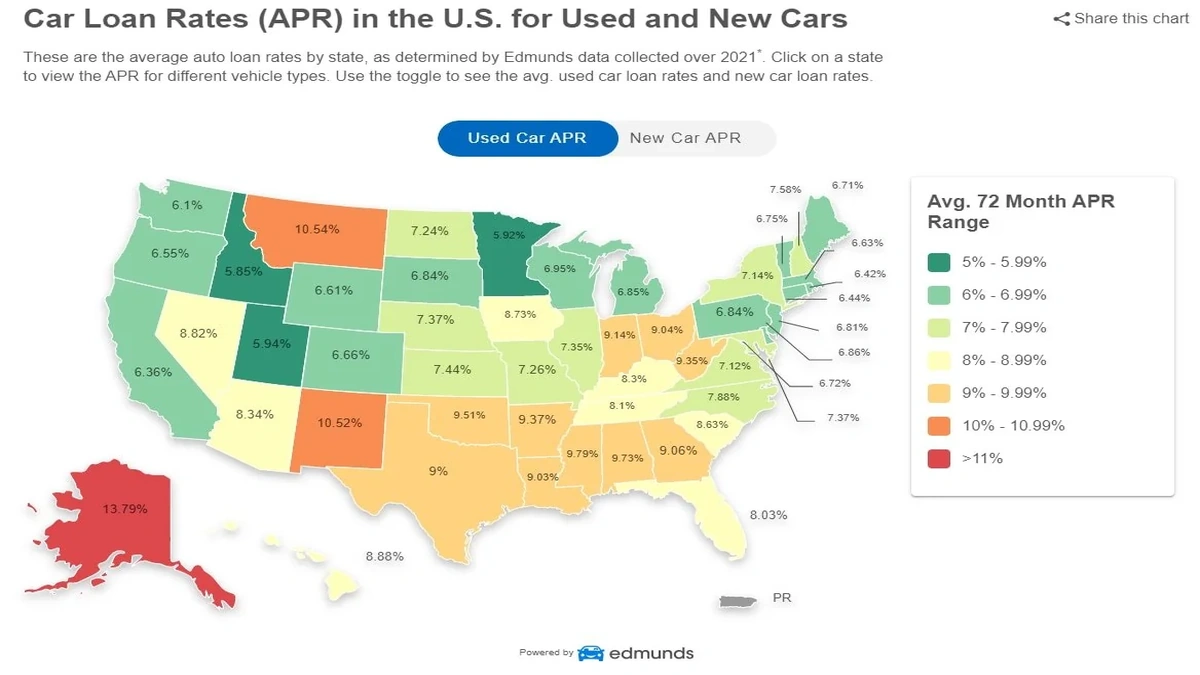

So, you’re eyeing that pre-loved beauty, huh? Maybe a trusty sedan, a family-friendly SUV, or perhaps even a zippy little commuter. The excitement is palpable, but then reality creeps in: the financing. Specifically, those dreaded used car loan interest rates USA . It’s not just a number on a screen; it’s a whole ecosystem of economic forces, personal circumstances, and market trends that can make or break your budget. And let me tell you, understanding the “why” behind these rates is far more crucial than just knowing the “what.”

Here’s the thing: most people just compare the headline APRs and call it a day. But that’s like judging a book by its cover when the real story, the one that impacts your wallet for years, is hidden within the pages. We’re going to dive deep, not just into what the averageauto loan ratesare, but why they fluctuate, why your credit score isn’t the only player, and why a seemingly small difference in interest can cost you thousands. This isn’t just about getting a loan; it’s about making a smart financial move in a complex market.

The Grand Economic Tapestry | Why Rates Are What They Are

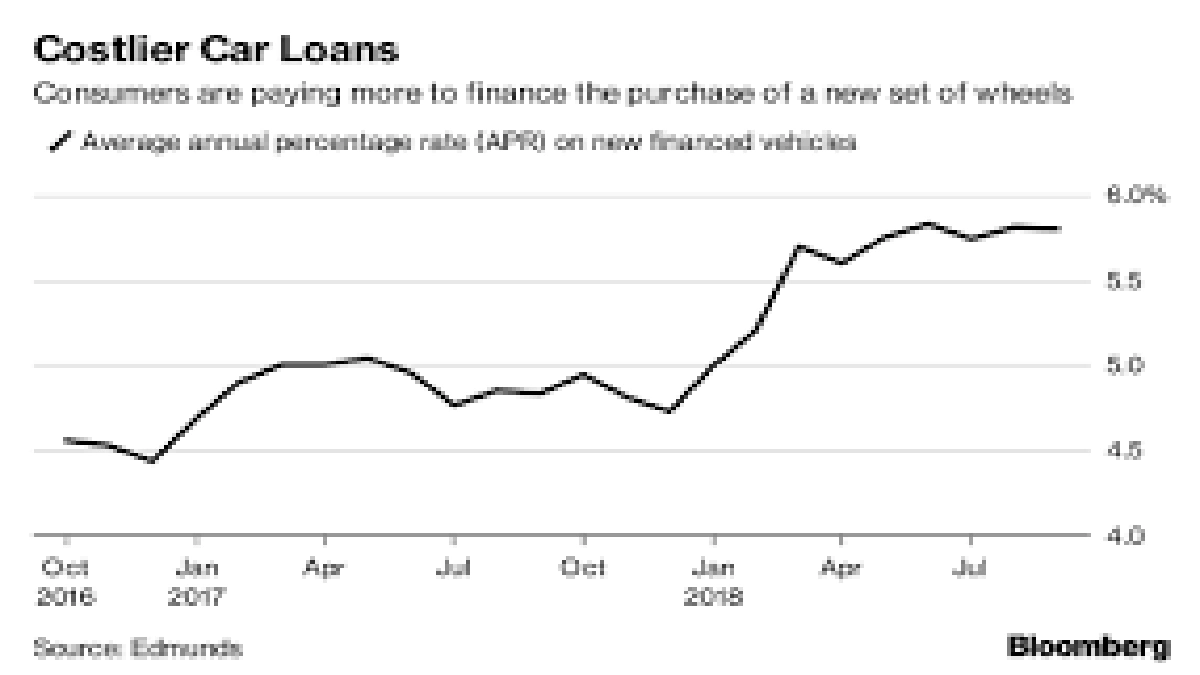

Ever wonder why used car loan interest rates USA seem to be a moving target? It’s rarely arbitrary. At the heart of it all lies the Federal Reserve’s monetary policy. When the Fed raises its benchmark interest rates, it trickles down through the entire financial system. Banks pay more to borrow money, and guess what? They pass those increased costs onto you, the consumer, in the form of higher interest rates on everything from mortgages to, yes, used car loans. It’s a direct cause-and-effect relationship, often making the difference between a good deal and a painful one.

But it’s not just the Fed. The broader economic climate plays a huge role. Are we in a recession? Is inflation rampant? During periods of economic uncertainty, lenders become more cautious. They perceive a higher risk in lending, and to compensate for that risk, they charge higher rates. Conversely, a robust economy with low unemployment might see more competitive rates as lenders vie for your business. It’s a constant dance between risk, reward, and the cost of money.

Beyond Your Credit Score | Other Unseen Influencers on Your APR

Okay, so everyone knows your credit score is king when it comes to securing a favorable loan. A stellar score (think 700+) usually unlocks the lowest car financing options . But what if I told you there are other significant factors at play that often get overlooked? This is where the real nuance of securing a great rate comes in.

The Age and Mileage of the Car Itself

Believe it or not, the vehicle you choose directly impacts your interest rate. Lenders view older cars with high mileage as higher risk. Why? Because they’re more prone to mechanical issues, which could lead to a borrower defaulting if the car breaks down and becomes a financial burden. A five-year-old car with 50,000 miles will often command a lower rate than a ten-year-old car with 150,000 miles, even for borrowers with identical credit scores. It’s about asset depreciation and collateral risk.

Loan Term and Down Payment | Your Hidden Levers

The length of your loan, or the loan terms explained , is another massive factor. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates because the lender’s money is tied up for a shorter period, reducing their risk exposure. Longer terms (60, 72, or even 84 months) might offer lower monthly payments, but you’ll almost always pay significantly more in interest over the life of the loan. It’s a classic trade-off: immediate affordability versus long-term cost. And don’t underestimate the power of a substantial down payment. The more you put down, the less you need to borrow, which signals lower risk to lenders and can translate into better rates.

Speaking of financial leverage, understanding your overall financial health is key. Sometimes, securing better terms for a vehicle loan can free up capital for other investments, perhaps even for improving your home. For those looking to optimize their financial portfolio, exploring tools like ahousing loan eligibility calculatorcan provide a broader perspective on managing debt and assets.

Dealership vs. Bank Financing | The Battle for Your Business

This is a decision point where many buyers go wrong. Do you go with the convenience of the dealership’s financing department, or do you brave the world of banks and credit unions? Each has its pros and cons, and understanding them can save you a bundle on used car market trends and rates.

Dealerships often offer promotional rates, especially on certified pre-owned vehicles. They can also be a one-stop shop, making the process seamless. However, their rates might not always be the absolute best, and sometimes they mark up the interest rate to boost their profit margins. Banks and credit unions, on the other hand, often have more competitive rates, particularly for borrowers with excellent credit. Credit unions, being member-owned, are notorious for offering some of the lowest APR vs interest rate options out there. The key? Get pre-approved by at least one or two external lenders before you step into the dealership. This gives you leverage and a benchmark to compare against any offers the dealer throws your way.

For businesses, similar strategic decisions apply when seeking capital. Just as an individual carefully weighs their auto loan options, businesses in India might exploreSME financing India guideto understand their best avenues for growth and investment.

When Bad Credit Strikes | Navigating Higher Rates

Let’s be honest, not everyone has a pristine credit history. Life happens. If you’re in the market for bad credit car loans , you’re likely to face higher interest rates. Lenders view borrowers with lower credit scores as higher risk, and they adjust their rates accordingly. It’s not personal; it’s just how risk assessment works in finance.

But here’s some good news: higher rates don’t mean no loan. It means being strategic. Focus on a larger down payment, consider a shorter loan term if possible, or even look for a co-signer with good credit. A co-signer essentially shares the risk, often making lenders more comfortable offering a better rate. Just ensure both parties understand the responsibilities involved. Remember, securing a subprime auto loan and making consistent, on-time payments can be a powerful way to rebuild your credit over time, opening doors to better rates in the future.

FAQs on Used Car Loan Interest Rates USA

What is a good used car loan interest rate in the USA?

A “good” rate depends heavily on your credit score. For excellent credit (720+), anything under 6-7% for a used car is generally considered good. For average credit (600-680), rates might be in the 8-15% range. Below 600, you could be looking at 15% or higher. It’s always best to compare offers from multiple lenders.

How can I lower my used car loan interest rate?

Improving your credit score is paramount. Pay down existing debts, make all payments on time, and avoid opening new credit lines before applying. Other strategies include making a larger down payment, choosing a shorter loan term, or finding a co-signer with good credit.

Is it better to get a used car loan from a bank or a dealership?

Often, banks and credit unions offer more competitive rates, especially if you have good credit. Dealerships provide convenience and sometimes special promotions, but it’s crucial to get pre-approved elsewhere first to ensure you’re getting the best deal. Always compare.

Do used car loan rates include APR?

Yes, the rate you’re quoted for a car loan is typically the Annual Percentage Rate (APR). The APR includes the interest rate plus any additional fees, giving you the total annual cost of borrowing. It’s the most accurate figure to use when comparing loan offers.

What impact do used car market trends have on interest rates?

When demand for used cars is high and supply is low, prices tend to rise. While this directly affects the purchase price, it can also indirectly influence interest rates. Lenders might adjust their risk models based on market volatility and the resale value of the collateral, potentially leading to slight shifts in rates, especially for specific vehicle types.

The Bottom Line | Be an Informed Buyer

Ultimately, navigating the world of used car loan interest rates USA isn’t about finding a magic bullet; it’s about being an informed, proactive buyer. It’s about understanding the intricate web of economic factors, personal financial health, and market dynamics that converge to determine your rate. Don’t just accept the first offer. Shop around, ask questions, and leverage every piece of knowledge you’ve gained here. Your future self, and your wallet, will thank you for it. Because when it comes to financing a used car, knowledge truly is your most powerful asset.