Picture this: you’re scrolling through social media, and an ad pops up – “Own a home in the USA with zero down payment mortgage options USA legit !” Sounds like a dream, right? Almost too good to be true. And let’s be honest, in the world of real estate, if something sounds too good, it often comes with a hefty asterisk. But here’s the thing: legitimate pathways to no down payment home loans do exist in the U.S. What fascinates me, and what we’re going to dive deep into today, isn’t just what these options are, but why they exist, why they matter, and why understanding their nuances is absolutely crucial for anyone dreaming of homeownership.

This isn’t just about reporting facts; it’s about peeling back the layers to understand the hidden context. We’ll explore the implications, the potential pitfalls, and the genuine opportunities these programs offer. So, grab your coffee, because we’re about to demystify the world of mortgages without a traditional down payment.

The “Why” Behind Zero Down | A Government-Backed Safety Net

When you hear “zero down payment,” your mind might immediately jump to risky subprime loans of yesteryear. But today, the most prominent and reliable zero down payment mortgage options USA legit are actually backed by the U.S. government. This isn’t some shady workaround; it’s a deliberate policy designed to make homeownership accessible to specific groups, and understanding why is key.

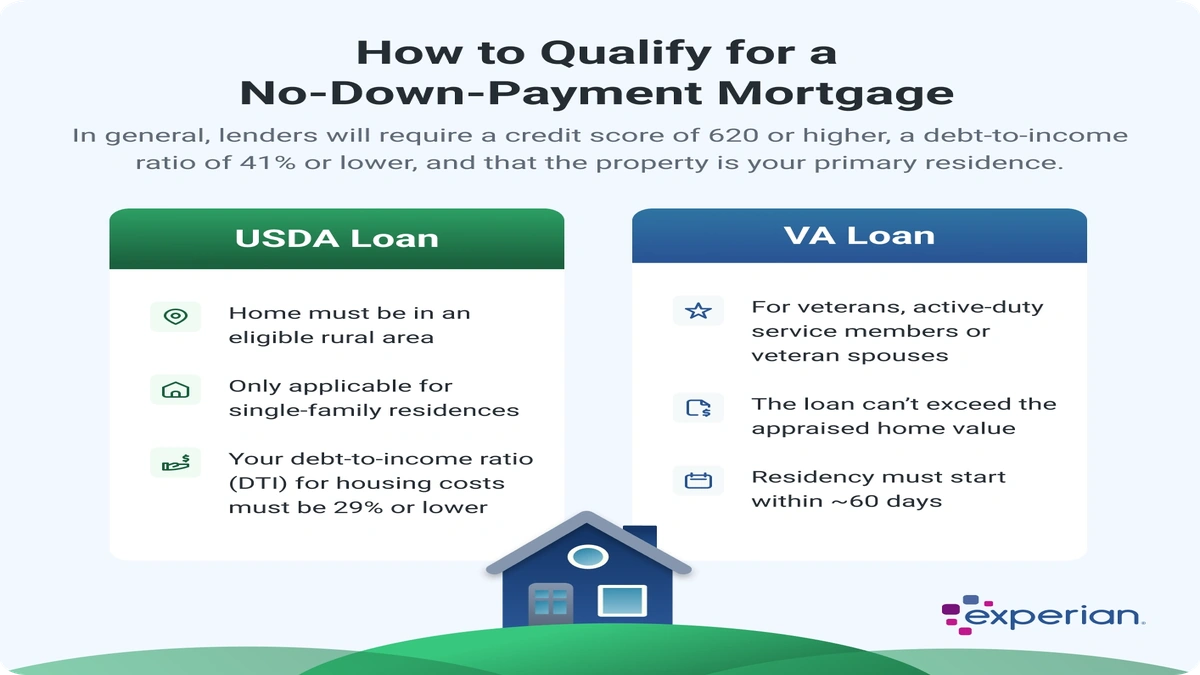

Think about it: the government has a vested interest in a stable housing market and supporting its citizens. This is why programs like the VA Loan and USDA Loan exist. The Department of Veterans Affairs (VA) home loan program, for instance, is a profound benefit for eligible service members, veterans, and their surviving spouses. It’s a thank you for their service, offering not just no down payment home loans but also competitive interest rates and often no Private Mortgage Insurance (PMI). The why here is clear: to honor and support those who served, recognizing that saving a large down payment can be challenging, especially for those who’ve dedicated their lives to the country.

Then there’s the U.S. Department of Agriculture (USDA) Rural Development Loan program. Now, don’t let the name fool you; it’s not just for farmers. This program targets eligible rural and suburban areas, helping to stimulate economic growth and ensure that even in less densely populated regions, homeownership remains attainable. The implication? If you’re looking to buy outside major metropolitan hubs, the USDA loan requirements might just open a door you didn’t know existed. It’s another example of a government initiative designed to fill a specific need, addressing the why of regional development and affordable housing.

Beyond the Hype | Understanding the Nuances of “Zero Down”

Okay, so the government isn’t just handing out free houses. I know, shocker! While zero down payment mortgage options USA legit truly mean no money required at closing for the down payment itself, it’s crucial to understand that buying a home involves other costs. This is where the hidden context comes in. We’re talking about closing costs, which can include appraisal fees, title insurance, origination fees, and more. These can easily add up to 2-5% of the loan amount.

A common mistake I see people make is assuming “zero down” means “zero out-of-pocket.” Let me rephrase that for clarity: you might still need funds for these closing costs. However, even here, there are strategies. Sellers might contribute to closing costs, or lenders might offer specific credits. Sometimes, you can even roll a portion of these costs into the loan, though that means borrowing more and paying more interest over time. This is why it’s so important to scrutinize the full financial picture.

Another big one? Private Mortgage Insurance (PMI). For most conventional loans where you put less than 20% down, lenders require PMI to protect themselves in case you default. While VA loans are famous for not requiring PMI, other low or no down payment home loans often do. This is a significant why for higher monthly payments. It’s an added expense that doesn’t build equity but is a necessary component for the lender to take on the increased risk. It’s a trade-off, and understanding that trade-off is part of being a savvy first-time home buyer.

Is a Zero Down Mortgage Legit for You? Unpacking the Pros and Cons

So, given all this, is a mortgage without down payment the right move? The answer, like most things in life, is: it depends. The why behind choosing this path is often about speed and preserving liquidity. For many, the biggest hurdle to homeownership isn’t the monthly payment, but saving up a substantial down payment while also paying rent and managing other expenses. Zero down options can accelerate your journey to homeownership, getting you into a home sooner and allowing you to keep your savings for emergencies or other investments. This can be a huge psychological and financial win.

However, the flip side is equally important. With no down payment, you start with zero equity (or even negative equity if home values dip slightly after purchase). This means you have less financial cushion if you need to sell quickly. Plus, as we discussed, higher monthly payments due to PMI (if applicable) and potentially slightly higher interest rates can impact your long-term financial health. It’s a delicate balance, and why your personal financial situation, your job stability, and your long-term goals should heavily influence your decision. When thinking about long-term financial commitments, it’s worth considering how different loan structures impact your overall financial journey, much like understandingstudent loan interest rates UKcan shape educational financing decisions.

Exploring Your Options | Beyond VA and USDA

While VA and USDA loans are the stars of the zero down payment mortgage options USA legit show, they aren’t the only players. It’s a vast landscape out there, and why exploring all avenues is smart. For instance, while FHA loans aren’t technically zero down (they typically require a 3.5% down payment), they are often grouped with low-down-payment options and have more flexible credit requirements than conventional loans, making them a viable alternative for many. Understanding these FHA loan alternatives can broaden your perspective.

Beyond federal programs, many states and local municipalities offer down payment assistance (DPA) programs. These can come in the form of grants (which don’t need to be repaid), second mortgages (often with deferred payments or low interest), or forgivable loans. When combined with a low-down-payment primary mortgage, these DPA programs can effectively result in zero out-of-pocket for the down payment. This is the why behind the complexity: the system is designed with layers of support, but you have to know where to look. Many of these are specifically geared towards first-time home buyer programs, aiming to give a leg up to those entering the market.

The Path Forward | Due Diligence and Expert Advice

So, you’re intrigued by these legitimate mortgage options? Great! But here’s the absolute truth: the most important step is due diligence. This is why rushing into any major financial decision without thorough research is a recipe for regret. Start by checking your eligibility for VA or USDA loans. If those don’t fit, explore state and local DPA programs in your desired area. Resources like the Department of Housing and Urban Development (HUD) website (for instance, you can find local housing counseling agencies onHUD.gov) are invaluable for finding certified housing counselors who can guide you through the maze of options.

Working with a knowledgeable loan officer who specializes in these types of loans is also critical. They can help you understand the fine print, compare different programs, and navigate the application process. Remember, their expertise is why you hire them. Don’t be afraid to ask a million questions – it’s your financial future on the line. Just like when consideringstudent financing, understanding all terms and conditions is paramount for making informed choices about your future.

Ultimately, while the dream of a mortgage without down payment is appealing, it’s about understanding the full picture. The closing costs, the potential for PMI, and the long-term financial implications are all part of the equation. It’s about making an informed decision that aligns with your financial readiness and long-term goals for homeownership.

Frequently Asked Questions About Zero Down Payment Mortgages

Are zero down payment mortgages always more expensive in the long run?

Not necessarily. While some zero down options might have higher interest rates or require Private Mortgage Insurance (PMI), programs like VA loans often come with very competitive rates and no PMI. The total cost depends on the loan type, interest rates, and fees, so it’s essential to compare different offers.

Can I get a zero down payment mortgage if I’m not a veteran?

Yes, absolutely! While VA loans are exclusive to eligible veterans and service members, USDA loans offer no down payment home loans for properties in designated rural areas, and these are open to non-veterans who meet income and property location requirements. Additionally, many state and local down payment assistance programs can effectively reduce your out-of-pocket down payment to zero.

What are closing costs, and do I still pay them with zero down?

Closing costs are fees associated with finalizing your mortgage loan and home purchase, including appraisal fees, title insurance, and lender fees. Even with zero down payment mortgage options USA legit, you typically still need to cover these costs. However, some programs allow these to be rolled into the loan, or sellers might offer credits to help cover them.

How do I find legitimate zero down payment programs?

Start by researching federal programs like VA and USDA loans. Then, look into state and local first-time home buyer programs and mortgage assistance programs in your specific area. Consulting with a mortgage lender specializing in government-backed loans or a HUD-approved housing counselor can also provide invaluable guidance.

Is it risky to buy a house with no down payment?

While legitimate zero down payment mortgage options USA legit are safe, buying a home with no equity does carry some inherent risks. If property values decline, you could find yourself owing more than your home is worth. It also means you might have higher monthly payments due to PMI. It’s crucial to assess your financial stability and the local housing market before making a decision.