Let’s be honest, taking a loan can feel like navigating a maze. And while a gold loan often comes to the rescue in times of urgent need, the real challenge often begins when it’s time to pay it back. I’ve seen countless people get tripped up by the fine print, the different repayment options , and the sheer number of choices available. But what if I told you that understanding your gold loan repayment options explained isn’t just about avoiding penalties, but about empowering yourself financially? It’s true! This isn’t just a dry rundown of facts; consider me your knowledgeable friend, sitting across the table, ready to demystify the process for you.

The thing is, a loan against gold isn’t a one-size-fits-all product. Lenders in India, from big banks to local NBFCs, offer a surprising array of structures, each designed to cater to different financial situations. And choosing the right one can literally save you money, stress, and sleepless nights. So, let’s dive deep into the ‘how-to’ of smart gold loan repayment, ensuring you’re always in control.

Understanding the Basics | How Gold Loans Actually Work

Before we dissect the repayment part, a quick refresher on what a gold loan actually entails. Simply put, it’s a secured loan where you pledge your gold ornaments or coins as collateral to a lender. In return, you receive a loan amount, typically a percentage of the gold’s market value. The beauty of it is its speed and minimal documentation compared to other loan types. However, this convenience comes with the responsibility of timely repayment, and that’s where the various gold loan schemes come into play.

What often surprises people is the flexibility. Unlike, say, a personal loan, where you might be locked into rigid monthly payments, many gold loan schemes offer more leeway. But this flexibility also means you need to be sharp about picking the right fit. And trust me, understanding the nuances of gold loan interest rates is crucial here – it’s not just about the headline number, but how that interest accrues under different repayment models.

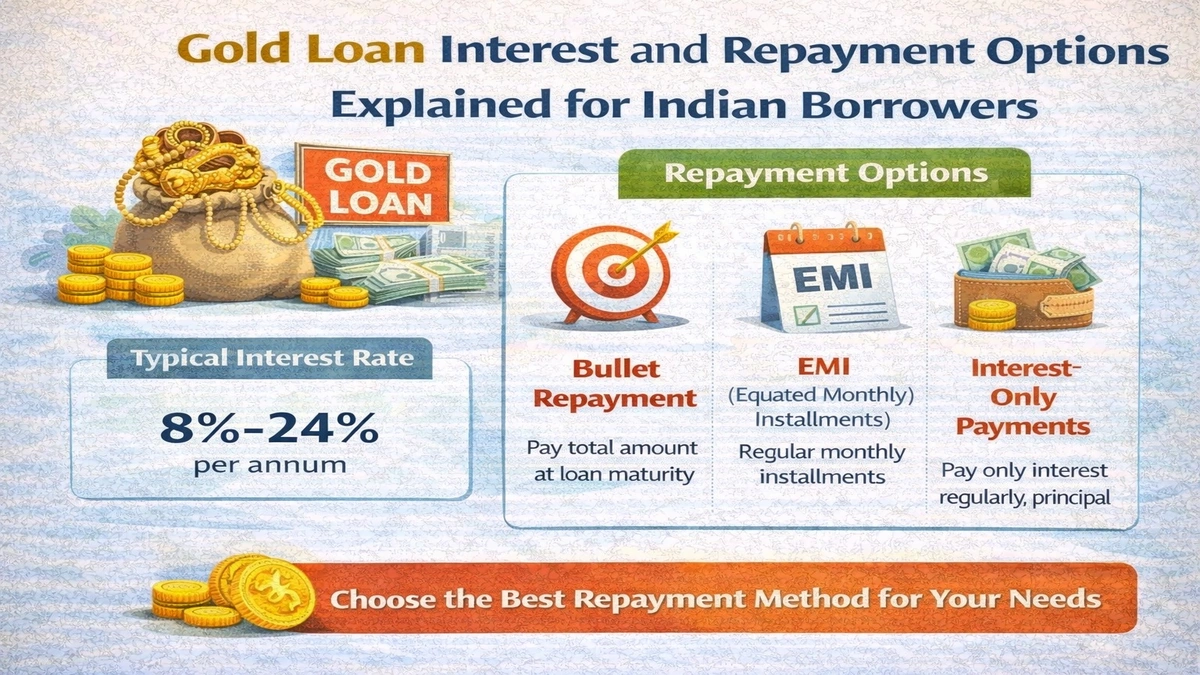

Decoding Your Repayment Choices | The Main Gold Loan Schemes

Here’s where it gets interesting, and where you can really tailor the loan to your financial pulse. Forget generic advice; let’s look at the specific repayment options you’ll typically encounter.

1. EMI Option (Equated Monthly Installment)

This is probably the most familiar repayment method, similar to what you’d find with ahome loanor a car loan. With the EMI option , you pay a fixed amount every month, which includes both a portion of the principal and the interest. It’s predictable, easy to budget for, and ideal if you have a steady income stream.

- Pros: Predictable payments, gradual reduction of principal, easy budgeting.

- Cons: Can feel restrictive if your income fluctuates, interest is calculated on the reducing balance.

Many prefer this for longer loan tenure periods, as it spreads out the financial commitment. It’s a solid, no-surprises choice for those who value consistency.

2. Bullet Repayment Scheme

Ah, the bullet repayment scheme – a true game-changer for short-term needs! This is perhaps the most unique and popular feature of gold loan schemes . Here’s how it works: you only pay the interest component of your loan every month (or quarter, depending on the lender), and the entire principal amount is repaid in one lump sum at the end of the loan tenure . It’s fantastic if you’re expecting a significant inflow of cash in the near future – maybe a bonus, a property sale, or a maturity payment from an investment.

- Pros: Low monthly outflow, great for short-term liquidity needs, ideal if you anticipate a lump sum payment.

- Cons: Requires discipline to save the principal, failure to pay the lump sum can lead to higher penalties or even auction of gold.

What fascinates me about this scheme is how perfectly it aligns with certain financial cycles in India. Just be sure you will have that lump sum ready!

3. Partial Payment / Interest-Only Scheme

Some lenders offer a hybrid approach where you can pay only the interest periodically and have the flexibility to make partial principal payments whenever you have surplus funds. The remaining principal is then paid at the end of the loan tenure . This offers more flexibility than a strict EMI and less risk than a pure bullet repayment, as you’re slowly chipping away at the principal.

- Pros: Flexibility to pay principal when convenient, reduces overall interest burden compared to bullet if principal is paid intermittently.

- Cons: Requires self-discipline to make principal payments, less predictable than EMI.

4. Upfront Interest Payment

Though less common, some specialized gold loan schemes might allow you to pay the entire interest amount upfront at the time of availing the loan. This means your only obligation at the end of the loan tenure is to repay the principal. It’s a niche option but can be beneficial if you have immediate surplus cash and want to clear your interest burden right away, ensuring no future interest calculations.

- Pros: No ongoing interest payments, clear financial commitment.

- Cons: Requires significant upfront cash, not suitable for everyone.

Smart Strategies for Managing Your Gold Loan | Beyond the EMI

Knowing the options is one thing; using them smartly is another. This is where your financial savvy truly shines.

Prepayment & Foreclosure | Don’t Get Caught Off Guard

One common mistake I see people make is not considering prepayment options. If you find yourself with extra cash, paying off your gold loan early can save you a significant amount on interest rates . Most lenders allow prepayment, but always check for any prepayment penalty clauses. Some might charge a small fee, especially if you close the loan very early. However, many public sector banks and some NBFCs have waived prepayment charges on floating rate loans, so it’s always worth asking!

On the other hand, understanding the foreclosure process is crucial. If you default on your payments, the lender has the right to auction your gold to recover their dues. This is the last thing anyone wants, so proactive communication with your lender if you face difficulties is key. They might offer restructuring options rather than immediately going for auction.

Refinancing Your Loan | A Smart Move?

Sometimes, market conditions change, or a new lender offers significantly better gold loan interest rates or more flexible repayment options . In such cases, refinancing your existing gold loan by taking a new loan from another lender (or even the same one) to pay off the old one can be a smart move. Always compare the new interest rate, processing fees, and any associated charges to ensure it’s genuinely beneficial. This is a bit like comparingloan processing feesacross different providers – every penny saved adds up.

Tips for Lowering Gold Loan Interest Rates

Believe it or not, there’s often room to maneuver. Here are a few pointers:

- Compare Lenders: Don’t just go to the first bank. Public sector banks often have lower interest rates than private banks or NBFCs, though their processing might be slower.

- Negotiate: Especially if you’re a long-standing customer or have a good credit history, you might be able to negotiate a slightly better rate.

- Choose the Right Scheme: Some gold loan schemes, like those with upfront interest payments or shorter tenures, might implicitly offer better effective rates.

- Maintain a Good Credit Score: While gold loans are secured, a strong credit score can sometimes give you an edge in negotiations.

Making the Right Choice for You | A Personalized Approach

So, how do you pick the ‘best’ option among all the gold loan repayment options explained ? It boils down to a few key questions:

- What is your income stability like? If it’s rock-solid, EMI might be best. If it’s seasonal or lump-sum dependent, bullet repayment could be your friend.

- What’s the purpose of the loan? Short-term working capital or a longer-term personal need?

- How much risk are you comfortable with? Bullet repayment offers low monthly commitment but higher end-of-term risk.

- Have you read the fine print? I can’t stress this enough. Understand the prepayment penalty, late payment charges, and foreclosure process of your specific lender.

Ultimately, the ‘best’ option isn’t universal; it’s the one that aligns perfectly with your financial situation and future expectations. Don’t be shy to ask lenders detailed questions. This is your money, your gold, and your financial peace of mind at stake.

Frequently Asked Questions About Gold Loan Repayment

Can I repay my gold loan early without penalty?

Many lenders, especially public sector banks, allow early prepayment without a penalty, particularly on floating rate gold loan schemes . However, it’s crucial to confirm this with your specific lender at the time of taking the loan, as some private banks or NBFCs might levy a small prepayment penalty .

What happens if I miss an EMI payment?

Missing an EMI payment can lead to late payment charges, an increase in the effective interest rates , and a negative impact on your credit score. If you anticipate missing a payment, it’s always best to communicate with your lender beforehand to explore possible solutions or extensions, rather than simply defaulting.

Is a bullet repayment scheme always better for short-term loans?

The bullet repayment scheme is often ideal for short-term loans if you are confident of receiving a lump sum to clear the principal at the end of the loan tenure . It offers lower monthly outflows. However, if that lump sum doesn’t materialize, the risk of default and potential foreclosure is higher. Evaluate your cash flow carefully.

How do I choose the best gold loan scheme for my needs?

To choose the best gold loan scheme , consider your income stability, the duration for which you need the funds ( loan tenure ), and your ability to manage monthly payments or save for a lump sum. Compare gold loan interest rates and repayment options across multiple lenders, and always read the terms and conditions carefully.

Can I extend my gold loan tenure?

Yes, in many cases, lenders allow you to extend your gold loan tenure , provided you meet their eligibility criteria and pay any accrued interest. This usually involves signing a new agreement or an addendum. Always discuss this with your lender well before your current tenure expires.