Ever stared at a car ad, seen that shiny new vehicle, and then thought, “Okay, but what’s my auto loan calculator monthly payment USA really going to look like?” You’re not alone. It’s a question that keeps many of us up at night, right alongside “Did I leave the stove on?” or “Where did I put my keys?” But here’s the thing: understanding your car loan isn’t some dark art reserved for financial gurus. It’s a crucial skill that empowers you, the car buyer, to make smart decisions, avoid buyer’s remorse, and ultimately save a good chunk of change. And trust me, in today’s market, every penny counts.

My goal today isn’t just to tell you what an auto loan calculator does. Anyone can Google that. Instead, I want to walk you through how to use it effectively, why certain numbers matter more than others, and what common pitfalls to avoid. Think of me as your personal financial guide, sitting across from you with a cup of coffee, ready to demystify the process. We’re going to dive deep, beyond the surface-level figures, so you can approach your next car purchase with confidence and clarity. Because let’s be honest, buying a car should be exciting, not anxiety-inducing!

Demystifying the Auto Loan Calculator | Your First Step to Smart Buying

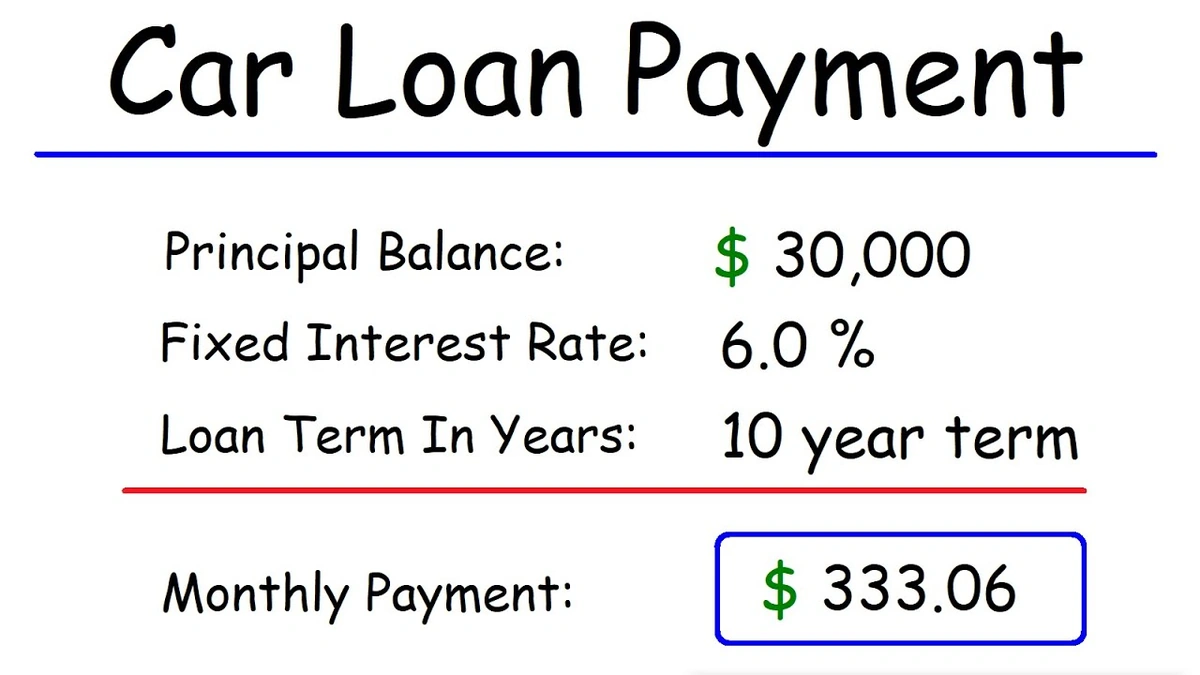

Okay, so you’ve heard of an auto loan calculator. Maybe you’ve even tinkered with one online. But do you really understand what’s happening behind the scenes? It’s more than just a magic box that spits out a number. At its core, an auto loan calculator monthly payment USA tool takes a few key pieces of information and, using a bit of financial wizardry (read: a formula), tells you what you’ll owe each month. The main ingredients? The principal loan amount (how much you need to borrow), the car loan interest rates , and the loan term (how long you have to pay it back). Simple, right?

Well, yes and no. What often gets overlooked is the profound impact each of these variables has on your final monthly payment . A slightly higher interest rate? It can add hundreds, if not thousands, to your total cost over the life of the loan. A longer loan term ? Your monthly payments might look lower, but you’ll likely pay a lot more in interest over time. It’s a delicate balance, and understanding this interplay is your superpower. I’ve seen too many people focus solely on the lowest monthly payment without considering the long-term cost, and that’s where lenders often make their money.

Before you even step foot in a dealership, playing around with anonline car loan calculatoris your secret weapon. It allows you to model different scenarios: what if I put down more money? What if I get a slightly better interest rate? What if I choose a 48-month term instead of 72? This foresight is invaluable, giving you a clear picture of what you can truly afford and what you should be aiming for when negotiating. It’s about being proactive, not reactive, in your financial journey.

Crunching the Numbers | How to Calculate Your Car Payment Like a Pro

Now, let’s get practical. You’re ready to use that car payment estimator . First, gather your data. You’ll need a target vehicle price (or at least a ballpark), an idea of your down payment, and a realistic expectation of your credit score, which directly influences your potential car loan interest rates . Most online calculators are pretty straightforward. You input the loan amount (car price minus your down payment), the interest rate (pre-qualify with a few lenders to get a good estimate!), and the loan term in months (e.g., 60 for five years, 72 for six).

A crucial element often underestimated is your down payment strategy . Putting more money down upfront directly reduces the principal amount you need to borrow. Less principal means less interest paid over the life of the loan, and a lower monthly payment . It’s simple math, but powerful. I always advise clients, if possible, to aim for at least a 10-20% down payment. It creates immediate equity and reduces your risk of being “upside down” on your loan, which means owing more than the car is worth. Trust me, you don’t want to be in that situation.

What if you’re exploring options for different types of financing, perhaps comparing various student loan structures? The principles of understanding interest, principal, and repayment terms are universally applicable. Just like you’d analyze the long-term cost of a car loan, it’s vital to dissect the implications of variousstudent loan refinance rates USA. The mechanics of how interest accrues and how different terms affect your total repayment amount are very similar, making the practice with an auto loan invaluable for other financial decisions.

Beyond the Monthly Figure | What Else Impacts Your Auto Loan?

Okay, so you’ve got a solid handle on the basic inputs. But a true financial wizard knows there’s more to the story than just principal, interest, and term. Your credit score, for instance, is a massive player. A higher credit score (generally 700+) can unlock the best auto loan rates , sometimes shaving off percentage points that translate into hundreds or even thousands saved over the loan’s duration. Lenders see you as less risky, and they reward that with better terms. If your credit isn’t stellar, don’t despair, but be realistic about the rates you’ll qualify for.

Then there are the “hidden” costs, or rather, the easily forgotten ones. Sales tax, registration fees, documentation fees – these can add a significant chunk to your total out-the-door price, which in turn increases the amount you need to finance. Always ask for an “out-the-door” price that includes all fees and taxes before you even start talking about financing. This transparency is key to truly understanding your commitment. And speaking of transparency, remember to explore all your auto financing options . Don’t just take the dealership’s first offer. Shop around!

I can’t stress this enough: comparison shopping for loans is just as important as comparison shopping for the car itself. Get pre-approved from your bank, credit union, and a few online lenders. This gives you leverage at the dealership. When you walk in with a pre-approval in hand, you’re negotiating from a position of strength, not desperation. This is one of the most effective auto financing tips I can give you. It allows you to do an effectiveauto loan rates comparisonand pick the best deal for you, not for the dealer.

Navigating Tricky Waters | Special Scenarios and Solutions

Life isn’t always a straight line, and neither are financial situations. What if your credit score isn’t ideal? Or what if you’re already in a loan you don’t love? Let’s talk about it. For those with less-than-perfect credit, securing an auto loan can feel daunting. While you might not qualify for the absolute best auto loan rates , there are still options. Many lenders specialize in bad credit car loans , though they will come with higher interest rates. The key here is to demonstrate stability: a steady job, a decent down payment, and a clear plan to make payments on time. Focus on improving your credit score while you repay, and you might even consider to refinance auto loan down the line.

Speaking of refinancing, it’s a strategy many people overlook. If your credit score has improved significantly since you first got your loan, or if interest rates have dropped, refinancing could save you a substantial amount. It essentially means taking out a new loan to pay off your old one, ideally with a lower interest rate or better terms. It’s a smart move to periodically check if refinancing makes sense, especially if you’re several years into a loan with a high rate. Always do anaffordability checkbefore committing to any new loan, whether it’s for a car or even comparing federal vs. private student loans. The principle remains: understand your capacity to pay.

The ultimate goal here is loan affordability . Don’t let the excitement of a new car push you into a loan you can’t comfortably manage. Use your auto loan calculator monthly payment USA tool to assess not just if you can make the payment, but if you can make it comfortably without stretching your budget thin. Leave room for unexpected expenses, because life, as we know, loves to throw curveballs. A little financial wiggle room can make all the difference between a joyful car ownership experience and a stressful one.

FAQ | Your Auto Loan Questions Answered

How does my credit score affect my auto loan calculator monthly payment USA?

Your credit score is a major factor. A higher score (generally 700+) signals less risk to lenders, allowing you to qualify for lower car loan interest rates . This directly reduces your principal, and thus, your monthly payment . A lower score means higher rates to offset the perceived risk.

Should I make a large down payment on my car?

Yes, if you can! A larger down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. It also helps avoid being “upside down” on your loan, where you owe more than the car is worth.

What’s the difference between a short and long loan term?

A shorter loan term (e.g., 36-48 months) means higher monthly payments but significantly less interest paid overall. A longer term (e.g., 60-72 months) offers lower monthly payments but results in paying much more in total interest. It’s a trade-off between monthly budget and total cost.

Can I get an auto loan with bad credit?

Yes, it’s possible to get bad credit car loans , but expect higher interest rates. Lenders specializing in these loans will look for other indicators of your ability to pay, such as stable employment and a reasonable down payment. Focus on improving your credit for better rates in the future.

When is it a good idea to refinance auto loan?

Refinancing is a good idea if your credit score has improved, if current interest rates are lower than your existing loan, or if you want to adjust your monthly payment (e.g., lower it by extending the term, or shorten it to pay less interest). Always compare the new terms carefully.

Are there any hidden fees not included in the auto loan calculator?

While the calculator covers principal and interest, it typically doesn’t include sales tax, registration fees, documentation fees, or extended warranty costs. Always ask the dealer for an “out-the-door price” that includes all charges to get a full picture of your total cost.

Your Journey to a Smarter Car Loan Starts Now

So, there you have it. The auto loan calculator monthly payment USA isn’t just a tool; it’s your personal financial compass in the complex world of car buying. By understanding its components, leveraging a smart down payment strategy, and diligently comparing auto financing options , you transform yourself from a passive borrower into an empowered decision-maker. Don’t let the numbers intimidate you. Instead, let them guide you. Because when you truly understand your loan, you’re not just buying a car; you’re investing in your financial peace of mind. Go forth, calculate with confidence, and drive away happy!