Ever found yourself staring at a bank’s website, scrolling through endless paragraphs about business loan eligibility criteria UK , and feeling like you need a degree in finance just to understand it? You’re not alone. Here’s the thing: securing UK business loans can feel like a daunting quest, especially when you’re trying to figure out if your brilliant idea or growing venture even qualifies. But what if I told you it doesn’t have to be a mystery?

Having advised countless entrepreneurs and small business owners, I’ve seen firsthand the confusion and frustration. My goal today isn’t just to list the requirements; it’s to peel back the layers, show you how lenders think, and equip you with a clear, actionable roadmap to boost your chances of approval. Consider this your personal guide to cracking the code of small business loan requirements in the UK. Let’s demystify this together, shall we?

Understanding the Foundation | What Lenders Really Look For

Before diving into specific checkboxes, it’s crucial to grasp the fundamental mindset of a UK lender. They’re not just looking at your current numbers; they’re assessing risk. They want to know you can repay the loan, and that means scrutinizing several key areas. Think of it as building a strong case for your business. This isn’t just about ticking boxes; it’s about presenting a compelling narrative of financial stability and growth potential.

One of the first things they’ll consider is your trading history. Most traditional lenders prefer businesses that have been operating for at least 1-2 years. Why? Because a track record provides tangible evidence of your business’s viability and revenue generation. If you’re a startup loan UK applicant, don’t despair! While traditional routes might be tougher, there are specialist business funding options UK tailored for new ventures, often backed by government schemes like the Start Up Loans programme, a component of broadergovernment business support initiatives. It’s about finding the right fit for your stage.

Next up, and perhaps the most critical, is your business credit score UK . Just like personal credit scores, your business’s credit rating is a numerical representation of its creditworthiness. Lenders use this to gauge your past financial behaviour. A strong score signals responsible borrowing and repayment. Conversely, a poor score can be a significant hurdle. This is where proactive financial management really pays off. Regularly checking your business credit report and addressing any inaccuracies or late payments can make a huge difference. Think of it as your business’s financial reputation – you want it to be impeccable.

The Nitty-Gritty | Key Eligibility Criteria You Can’t Ignore

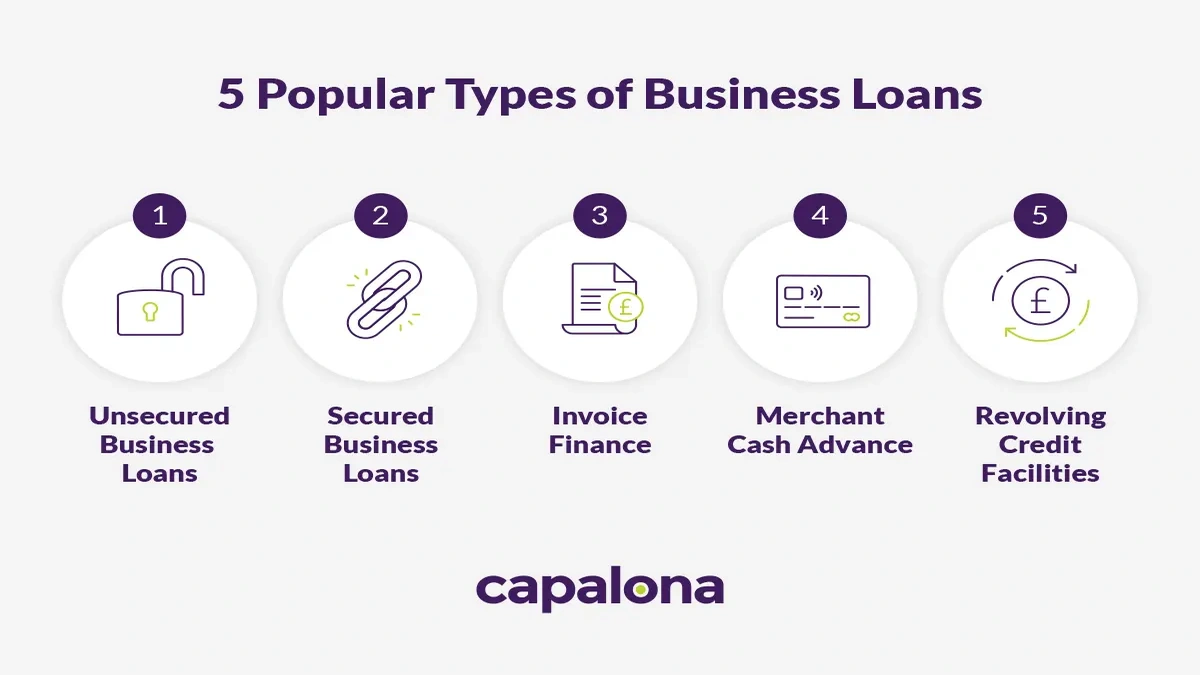

Now, let’s get into the specifics. While criteria can vary slightly between lenders and loan types (e.g., secured vs. unsecured business loan UK ), there’s a common eligibility checklist that almost every lender will review. Knowing these beforehand allows you to prepare meticulously, turning a stressful application into a confident submission.

1. Business Age and Trading History

As mentioned, most lenders prefer established businesses. Typically, they look for:

- Minimum Trading Period: Often 1-2 years, sometimes 6 months for alternative lenders.

- Registration: Your business must be registered in the UK (Companies House for limited companies, HMRC for sole traders/partnerships).

If your business is relatively new, focus on demonstrating strong projections, a solid business plan, and any personal guarantees you can offer. This is where your passion and strategic foresight really shine through.

2. Financial Health and Turnover

This is where your numbers do the talking. Lenders want to see healthy cash flow and sufficient turnover to comfortably cover loan repayments. They’ll typically ask for:

- Minimum Annual Turnover: This varies wildly, from £50,000 for some smaller loans to £250,000+ for larger facilities. Make sure your financial records are up-to-date and accurate.

- Profitability: While not always a deal-breaker for growth-focused loans, consistent profitability strengthens your case significantly.

- Cash Flow Statements: These are vital. Lenders want to see a clear picture of money coming in and going out, ensuring you have the instant liquidity to manage your day-to-day operations and debt obligations.

Preparing detailed financial forecasts and management accounts can significantly impress a lender, showing you have a firm grip on your business finance .

3. Business Credit Score and Personal Credit History

Your business credit score is paramount. Companies like Experian, Equifax, and Creditsafe provide these scores. Factors influencing it include your payment history with suppliers, any County Court Judgements (CCJs), and your company’s financial structure. But here’s a detail many overlook: your personal credit history. For smaller businesses, especially sole traders or directors of limited companies, your personal credit score will often be considered. It provides an additional layer of assurance to the lender, reflecting your broader financial responsibility. It’s a holistic view of your financial health .

4. Loan Purpose and Business Plan

Lenders aren’t just handing out money; they want to know why you need it and how it will be used to grow your business. A well-articulated business plan is your opportunity to demonstrate:

- Clear Purpose: Is it for expansion, equipment purchase, working capital, or marketing? Be specific.

- Market Analysis: Show you understand your industry and target market.

- Financial Projections: Realistic forecasts of how the loan will impact your revenue and profitability.

This isn’t just a formality; it’s your chance to convey confidence and strategic thinking. A solid plan shows you’re serious about growth, not just seeking a quick fix.

Beyond the Basics | Boosting Your Application and Exploring Alternatives

So, you’ve checked the boxes, but what else can you do to stand out? Or what if you don’t quite meet all the traditional loan requirements ?

Crafting a Winning Loan Application Process UK

The loan application process UK is your moment to shine. Don’t rush it. Double-check every detail. Ensure all supporting documents bank statements, accounts, business plan, tax returns are accurate, up-to-date, and presented professionally. A common mistake I see is incomplete applications or poorly organised documents. Lenders are busy; make their job easier by providing everything they need in a clear, concise manner.

Consider writing a cover letter that briefly outlines your business, the loan purpose, and why you believe you’re a strong candidate. It adds a human touch and allows you to highlight aspects not immediately apparent in the financial statements. This personal touch, coupled with meticulous preparation, can significantly improve your chances.

Exploring Diverse Business Funding Options UK

Let’s be honest, not every business will qualify for a traditional bank loan right off the bat, especially if you’re a new startup or have a less-than-perfect credit history. But here’s where expertise comes in: the UK SME finance UK landscape is incredibly diverse. Don’t put all your eggs in one basket. Explore:

- Alternative Lenders: Online lenders, peer-to-peer platforms, and specialist finance providers often have more flexible eligibility criteria and faster application processes. They might focus more on current cash flow than historical financials.

- Government-Backed Schemes: Programmes like the British Business Bank’s Enterprise Finance Guarantee (EFG) scheme can help businesses with viable plans but insufficient security get loans from traditional banks. It’s designed to lower the risk for lenders.

- Invoice Finance/Asset Finance: If you have outstanding invoices or valuable assets, these can be leveraged for funding. These options focus on specific assets rather than the overall business health.

It’s about matching your business’s unique profile and needs with the right type of funding options . Sometimes, a smaller, more specialized loan can provide the initial boost you need, leading to greater eligibility for larger loans down the line. It’s a stepping stone approach to managing your loan terms and growth.

On a slightly different note, thinking about long-term financial planning for your business might also involve considering how different types of loans or investments could impact future opportunities, much like how individuals plan for something likehigher educationfunding. It’s all about strategic financial foresight.

FAQs | Your Quick Questions Answered

Frequently Asked Questions About Business Loan Eligibility UK

What if my business is new and has no trading history?

While challenging, it’s not impossible. Focus on a robust business plan, strong personal credit history, and consider government-backed startup loans (like the Start Up Loans programme) or alternative lenders who are more open to new ventures. Personal guarantees might also be required.

How important is my personal credit score for a business loan?

Very important, especially for sole traders, partnerships, and directors of small limited companies. Lenders often look at both your business and personal credit scores to assess overall risk and financial responsibility. Make sure both are in good shape.

What annual turnover do I need for a business loan in the UK?

This varies significantly. Some micro-lenders might consider businesses with £25,000+ turnover, while traditional banks often require £50,000 to £100,000+ annually. For larger loans, this figure can easily exceed £250,000. Always check the specific lender’s requirements.

Can I get a business loan with bad credit?

It’s harder, but not impossible. You might need to explore specialist bad credit business loan providers, secured loans (where you offer an asset as collateral), or government-backed schemes designed to support businesses with less-than-perfect credit. Be prepared for higher interest rates.

What documents will I need for a business loan application?

Typically, you’ll need your business plan, bank statements (usually 6-12 months), latest filed accounts, management accounts, tax returns, and proof of identity/address for directors/owners. Some lenders may ask for cash flow forecasts and details of assets/liabilities.

How long does the business loan application process take?

It depends on the lender and the complexity of your application. Online alternative lenders can offer decisions and funding within days, sometimes even hours. Traditional banks typically take longer, from a few weeks to a couple of months, especially for larger or more complex loans.

The Bottom Line | Preparation is Power

The journey to securing business loan eligibility criteria UK doesn’t have to be a confusing one. It’s about understanding the landscape, meticulously preparing your application, and knowing where to look beyond the traditional avenues. Remember, lenders are looking for confidence, clarity, and a solid plan for repayment. By focusing on your financial health , bolstering your credit profile, and presenting a compelling case for your business’s growth, you’re not just applying for a loan; you’re investing in your future. Go forth, prepare wisely, and unlock the funding your business deserves!