So, you’ve got your heart set on that new set of wheels, haven’t you? The gleaming paint, the smell of fresh upholstery, the freedom of the open road… it’s a beautiful dream. But then, reality hits: the dreaded car loan interest rates . Suddenly, that dream car starts looking a little less affordable, doesn’t it? Trust me, I’ve seen countless hopeful buyers walk into showrooms only to be blindsided by high EMIs. It’s a common story, but it doesn’t have to be yours.

Here’s the thing: securing a cheap car loan isn’t just about finding the lowest advertised rate. It’s a strategic game, a dance between your financial profile, the lender’s policies, and a bit of savvy negotiation. And yes, you absolutely can win this game. My goal today is to walk you through the trenches, arming you with the insider knowledge to not just get a car loan, but to get the best car loan interest rates possible in India. Think of me as your personal finance co-pilot, guiding you away from those costly detours.

We’re going beyond the surface-level advice you’ll find everywhere. We’re diving deep into the ‘how’ and ‘why’ of securing those elusive low interest car loans . Ready to save some serious cash on your dream car? Let’s get started.

The Unseen Power Play | Understanding Car Loan Interest Rates

Before we even talk about getting a better rate, let’s demystify what drives these numbers. Many people assume interest rates are fixed, a take-it-or-leave-it scenario. But that’s rarely the full picture. Lenders assess risk, and your interest rate is essentially a reflection of how risky they perceive you to be as a borrower. This is why two different people can apply for the same car loan from the same bank and get wildly different EMI figures.

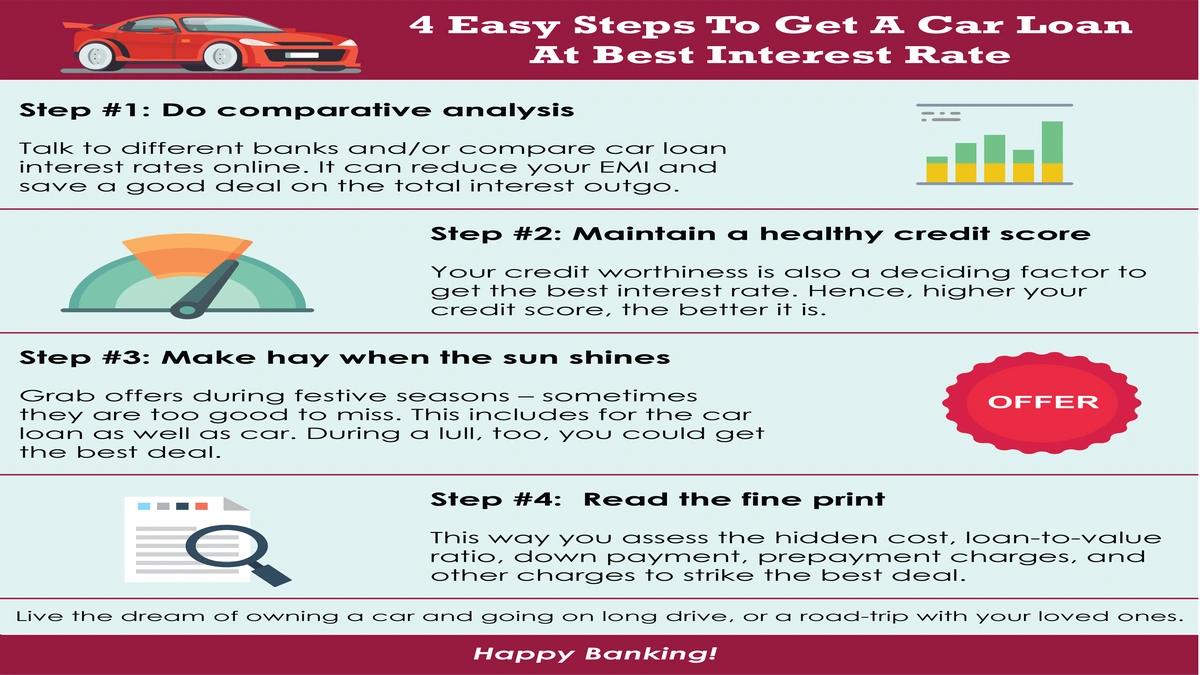

What factors influence this ‘risk assessment’? Primarily, it’s your credit history, income stability, existing debt, and even the type of car you’re buying. New cars generally attract slightly lower rates than used cars, for instance, because they’re seen as less of a depreciation risk. What fascinates me is how many people overlook the basics of how their financial behavior impacts these rates. Understanding this fundamental power play is your first step towards getting those juicy cheap car loan interest rates .

It’s also crucial to understand the difference between fixed and floating interest rates. Most car loans in India come with fixed rates, meaning your EMI remains constant throughout the loan tenure. This offers predictability, which is great for budgeting. However, if market rates drop significantly, you won’t benefit unless you refinance. Knowing this helps you make an informed decision when comparing offers.

Your Credit Score | The Golden Ticket to Lower EMIs

If there’s one thing you absolutely must double-check before even thinking about a car loan, it’s your credit score for car loan eligibility. This three-digit number, typically ranging from 300-900, is your financial report card. A score of 750 or above is generally considered excellent and puts you in a prime position to negotiate for the best car loan rates. Anything below that, and lenders might see you as a higher risk, offering less favorable terms or even rejecting your application.

A common mistake I see people make is applying for a loan without checking their score first. Each loan application can slightly ding your score, so you want to be strategic. You can get a free credit report from agencies like CIBIL, Experian, or Equifax. Look for any errors and get them rectified. A clean, strong credit history signals trustworthiness to lenders, which translates directly into lower interest rates . It’s like having a VIP pass to the best deals.

Building a good credit score takes time, but it’s worth the effort. Always pay your existing EMIs and credit card bills on time, keep your credit utilization low, and avoid applying for too many loans simultaneously. These are basic tenets of good financial health, and they pay dividends when you’re seeking significant financing like a car loan.

Beyond the Showroom | Pre-Approval and Negotiation Secrets

Here’s where many buyers go wrong: they walk into a dealership, fall in love with a car, and then let the dealer arrange the financing. While convenient, this often means you’re not getting the cheapest car loan . Why? Because dealerships often have tie-ups with specific lenders and might push options that give them a higher commission, not necessarily the best deal for you.

The smarter play? Get a loan pre-approval from a bank or financial institution before you visit the showroom. This gives you immense bargaining power. You’ll know exactly how much you can borrow and at what interest rate. It’s like walking into a negotiation with cash in hand dealers take you more seriously. You can then use this pre-approval as leverage to get the dealership’s finance partner to match or beat that offer. This is one of the most effective negotiation tactics car loan applicants can employ.

Don’t be afraid to shop around. Compare offers from at least 3-4 different banks or NBFCs. Look beyond just the interest rate; consider processing fees, foreclosure charges, and other hidden costs. Sometimes, a slightly higher interest rate with zero processing fee might be better than a lower rate with hefty upfront charges. It requires a bit of homework, but that homework can save you lakhs over the loan tenure .

Smart Moves | Down Payments, Tenure, and Hidden Fees

Let’s talk about the mechanics of the loan itself. Your down payment car loan amount is a significant factor in your overall cost. The larger your down payment, the less you need to borrow, which directly reduces your EMI and the total interest paid over time. It’s simple math, but often overlooked in the excitement of a new purchase. Aim for at least 15-20% of the car’s value as a down payment if you can manage it.

Then there’s the loan tenure. While a longer tenure (e.g., 7 years) might make your monthly car loan EMI seem more manageable, it significantly increases the total interest you pay. For example, a loan for 5 lakhs at 9% interest over 5 years will cost you less in total interest than the same loan over 7 years. My advice? Opt for the shortest tenure you can comfortably afford. It’s a disciplined approach that saves you money in the long run.

And those hidden fees? Oh, they’re real. Look out for processing fees, documentation charges, stamp duty, and pre-closure penalties. Always ask for a detailed breakdown of all costs associated with the loan. Sometimes, a bank offering a slightly higher interest rate but with fewer or no processing fees might turn out to be the cheaper option overall. Transparency is key, and if a lender isn’t upfront about all costs, that’s a red flag. This also applies when considering financial products like student loans, where understanding all charges is crucial, just like when youcompare education loan interest rates in India.

Picking Your Partner | Banks vs. NBFCs and Special Offers

When it comes to securing the best way to get cheap car loan interest rates , where you borrow from matters. Public sector banks often offer the lowest interest rates due to their lower operating costs and government backing. However, their processing times can sometimes be longer, and their eligibility criteria might be stricter. Private sector banks, on the other hand, might have slightly higher rates but offer faster processing and more flexible terms.

Non-Banking Financial Companies (NBFCs) are another option, especially if your credit score isn’t stellar or if you need quick disbursal. While they might be more lenient with eligibility, their car loan interest rates India can be significantly higher. It’s a trade-off between convenience/flexibility and cost. Always weigh these factors carefully.

Keep an eye out for special promotional offers. During festive seasons or at the end of financial quarters, banks and manufacturers often roll out attractive deals, including reduced interest rates or zero processing fees. These can be golden opportunities to snag a better deal. Also, if you have an existing relationship with a bank (e.g., salary account, home loan), leverage it. They might offer preferential rates to loyal customers. This strategy can be quite effective, similar to how one might approachapplying for a student loan in the UK, where existing banking relationships can sometimes smooth the process.

Don’t forget about manufacturer tie-ups. Car companies often collaborate with specific banks to offer special finance schemes, sometimes with subsidized rates. While these can be attractive, always compare them with independent offers you’ve researched. Sometimes, what looks like a great deal might come with hidden conditions or a slightly higher car price. Always do your due diligence, and remember, good car finance tips are about thorough comparison.

For more detailed insights into car loans and financial planning, you might find resources likeWikipedia’s page on Car Financehelpful in understanding the broader context of vehicle financing.

FAQs | Your Quick Car Loan Queries Answered

What is the ideal credit score for a car loan?

While lenders may approve loans for lower scores, an ideal credit score of 750 or above significantly increases your chances of securing the best way to get cheap car loan interest rates and favorable terms from banks.

Can I get a car loan without a down payment?

While 100% funding options exist, they are rare and usually come with higher interest rates. A healthy down payment car loan amount (15-20%) is always recommended to reduce your EMI and total interest burden.

How can I calculate my car loan EMI?

Most bank websites offer an online car loan calculator . You input the loan amount, interest rate, and tenure, and it instantly shows your estimated monthly EMI. This is a great tool for planning your finances.

Should I opt for a fixed or floating interest rate?

Most car loans in India are offered at fixed interest rates, providing stable and predictable EMIs. Floating rates are less common for car loans but could be considered if you anticipate a significant drop in market interest rates.

What documents are typically required for a car loan?

Common documents include identity proof (Aadhaar, PAN), address proof (utility bills), income proof (salary slips, bank statements, ITR), and bank statements for the last 6-12 months. Specific requirements can vary by lender.

Is it better to get a car loan from a bank or a dealership?

It’s generally better to get a loan pre-approval from a bank before visiting a dealership. This gives you more leverage and ensures you’re getting the most competitive interest rates, rather than relying solely on the dealership’s tied-up finance options.

Your Road to Lower Interest Rates Starts Now

Getting a car loan doesn’t have to feel like navigating a maze blindfolded. By understanding the factors that influence your rates, diligently improving your credit score, strategically shopping for lenders, and being smart about your down payment and tenure, you are well on your way to finding the best way to get cheap car loan interest rates .

Remember, your dream car shouldn’t come with the nightmare of exorbitant EMIs. Arm yourself with this knowledge, be patient, and don’t settle for the first offer you get. Your wallet will thank you. Happy driving, and even happier saving!