Let’s be honest, the idea of needing a loan but not having a traditional salary slip can feel like hitting a brick wall, right? You’re in the UK, you need some financial breathing room, but your income isn’t neatly packaged into a monthly payslip. Maybe you’re self-employed, working a gig economy job, or perhaps you’re relying on benefits. The good news? That brick wall isn’t impenetrable. What fascinates me about the modern lending landscape is how it’s evolving to recognise diverse financial realities. This isn’t just about finding a workaround; it’s about understanding the system and knowing your options. So, if you’ve been wondering about personal loan without salary slip UK options, grab a cuppa, and let’s walk through this together. I’m here to guide you, step-by-step, on how to navigate this often-confusing terrain.

Understanding the “Why” | Why Lenders Ask for Payslips (and What They Really Want)

Before we dive into the ‘how,’ it’s crucial to understand the ‘why.’ Lenders aren’t just being difficult when they ask for a payslip. They’re primarily trying to assess risk. A payslip is a straightforward, universally understood document that proves consistent income, helping them gauge your ability to repay the loan. It’s their safety net, their way of ticking the ‘affordability’ box.

But here’s the thing: while a payslip is convenient, it’s not the only way to prove you can manage repayments. What lenders truly want is reliable evidence of income and financial stability. That’s where proof of income alternatives UK come into play. They need to see a clear, predictable flow of money into your account, regardless of its source. It’s about demonstrating that you have the capacity to honour your commitment, even if your income stream doesn’t fit the traditional 9-to-5 mould. This understanding is your first powerful tool in securing a personal loan without salary slip UK options.

Your Toolkit | Alternative Ways to Prove Income (Beyond the Payslip)

Okay, so you don’t have a payslip. No worries! There are several other robust ways to demonstrate your income and financial reliability. Think of these as your personal financial toolkit:

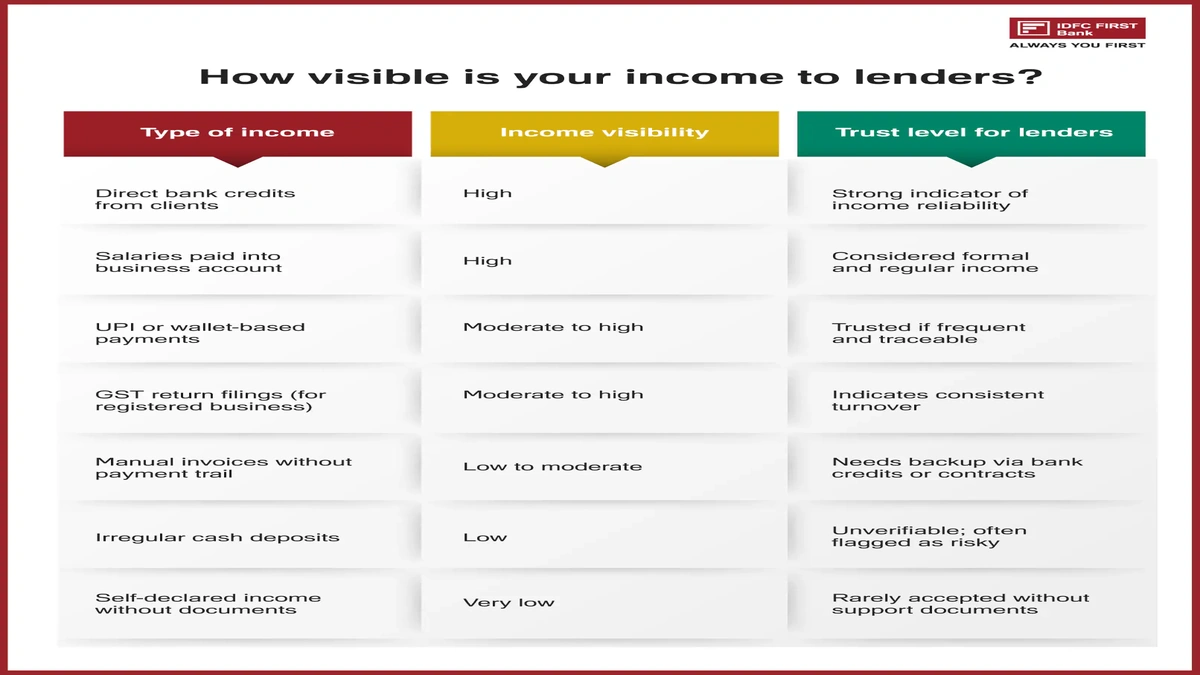

1. Bank Statements: Your Financial Storybook

This is probably the most common and effective alternative. Lenders will typically ask for 3-6 months of bank statements. They’re looking for consistent deposits that reflect your stated income, showing your financial habits, and confirming that money is regularly coming in. For example, if you’re a freelancer, your client payments will show up here. This gives them a detailed transaction history.

2. Tax Returns (SA302s): The Self-Employed’s Best Friend

If you’re self-employed, your Self-Assessment tax returns (SA302s) are gold. These documents, usually covering the last 1-2 years, provide an official record of your earnings and expenses, giving lenders a comprehensive overview of your business’s profitability and your personal income. Many lenders offering self-employed loans UK specifically request these. This is often the primary way to secure an unsecured personal loans UK without a traditional employer.

3. Benefit Statements/Letters: Proof of Support

If your income largely comes from state benefits (e.g., Universal Credit, Disability Living Allowance, Pension Credit), official letters or statements from the Department for Work and Pensions (DWP) can serve as proof. Lenders will assess these to understand the regularity and amount of your benefit income. There are specific lenders who specialise in benefits-based loans UK.

4. Rental Income & Pension Statements: Diverse Streams

Do you receive rental income from a property? Official tenancy agreements and corresponding bank statements can prove this. Similarly, if you’re retired, your pension statements clearly show your regular income. These are all valid alternative income verification methods that paint a picture of your financial capacity.

5. Accountant’s Letter: Professional Validation

For some self-employed individuals, a letter from a qualified accountant verifying your annual income can be very persuasive. This adds a layer of professional credibility to your financial claims.

The key here is transparency and consistency. The more clearly you can demonstrate a reliable income stream, even if it’s unconventional, the better your chances of securing a personal loan without salary slip UK options.

Navigating the Lenders | Where to Look for Personal Loan Without Salary Slip UK Options

Now that you know what kind of proof you can offer, where do you take it? Not all lenders are created equal, especially when you’re looking to borrow money without proof of income in the traditional sense. It’s about finding the right fit.

1. Specialist Lenders: The Flexible Ones

Many mainstream banks are quite rigid with payslip requirements. However, there’s a growing market of specialist lenders who are more accustomed to dealing with non-traditional income sources. These might include lenders focusing on no guarantor loans direct lender products or those catering specifically to the self-employed or individuals on benefits.

2. Credit Unions: Community-Focused Lending

Credit unions are member-owned financial cooperatives that often offer more flexible lending criteria than high street banks. They tend to take a more holistic view of your financial situation and may be more open to alternative proofs of income, especially if you have a good savings history with them. You might also be interested in exploring options likestudent financingif that’s a path you’re considering.

3. Guarantor Loans: A Helping Hand

While not strictly a ‘no payslip’ solution, if you have a friend or family member with a good credit score and stable income willing to act as a guarantor, this can open doors. The guarantor essentially promises to make repayments if you can’t, significantly reducing the lender’s risk. This can be an option if you’re struggling to find bad credit loans no payslip from other avenues.

4. Short-Term Loans: For Smaller, Urgent Needs

For smaller amounts and shorter repayment periods, some lenders offering short term loans UK no income proof might be more lenient. However, be extremely cautious with these, as interest rates can be significantly higher. Always check the total cost of the loan and ensure you can comfortably repay it. If you’re looking for emergency cash without employment verification, these might appear tempting, but due diligence is paramount.

Remember, always check if the lender is regulated by the Financial Conduct Authority (FCA). You can verify this on theFCA Register. This ensures they adhere to strict responsible lending practices UK and protect consumers.

The Application Journey | Your Step-by-Step Guide to Success

Alright, you’ve got your documents, you know where to look. Now, let’s talk about the application itself. This is where preparation meets opportunity.

Step 1: Get Your Finances in Order

Before you even start, review your bank statements, tax returns, and any other income proof. Ensure everything is up-to-date and easily accessible. Understanding your overall financial health, much like planning forhome loan down payment assistance programs, is key. Lenders will also look at your outgoings, so having a clear picture of your budget is vital.

Step 2: Check Your Credit Score

Your credit score is a crucial factor. Even if you have alternative income proof, a strong credit score will always help your application. Use services like Experian, Equifax, or TransUnion to get a free copy of your report. If there are errors, get them corrected. If it’s low, consider ways to improve it before applying.

Step 3: Research and Compare Lenders

Don’t just go with the first option you find. Use comparison websites or brokers that specialise in loans for those without traditional payslips. Read reviews and understand the terms and conditions. Look for lenders who are transparent about their fees and interest rates.

Step 4: Make a Strong Application

When filling out the application, be honest and provide all requested information accurately. If there’s a section for ‘additional information’ or ‘notes,’ use it to explain your income situation clearly and concisely, referencing the alternative proofs you’re providing. For instance, you could state, “My income is derived from freelance graphic design work, as evidenced by my last 6 months of bank statements and my most recent SA302 tax return.”

Step 5: Be Prepared for Affordability Checks

Lenders are legally obligated to conduct affordability checks. This means they’ll scrutinise your income versus your expenses to ensure you can realistically afford the repayments without falling into financial difficulty. This is why having a clear budget is so important. For more guidance, theCitizens Advice Bureauoffers excellent resources on managing debt and money.

A common mistake I see people make is applying to too many lenders in a short period. Each application can leave a ‘hard search’ mark on your credit file, which can temporarily lower your score. Be strategic and targeted in your applications.

FAQ | Your Burning Questions Answered

Frequently Asked Questions About Loans Without Payslips

Can I get a loan if I’m on benefits?

Yes, it is possible. Many specialist lenders and credit unions consider benefits as a regular source of income. You’ll need to provide official DWP statements or letters as proof, and the lender will assess your overall affordability.

What if I have bad credit and no payslip?

This is a tougher challenge, but not impossible. Your options might include guarantor loans, very small short term loans UK no income proof (with higher interest rates), or loans from credit unions. Focusing on improving your credit score first, even slightly, can significantly enhance your chances.

Are emergency cash without employment verification loans safe?

If you choose a lender regulated by the FCA, they operate under strict rules designed to protect consumers. However, ’emergency cash’ loans often come with higher interest rates and shorter repayment terms, making them riskier if not managed carefully. Always check the lender’s FCA registration.

How long does the application process take?

This varies. Online applications with all documents ready can sometimes yield a decision within hours or a day. However, if a lender needs to manually review alternative income proofs, it might take a few business days. Be prepared for a bit of back-and-forth for verification.

What documents do I really need?

While a payslip isn’t required, you’ll generally need photo ID (passport/driving licence), proof of address (utility bill/bank statement), and your chosen proof of income alternatives UK (e.g., 3-6 months of bank statements, SA302s, benefit letters). The more comprehensive your documentation, the smoother the process.

So, there you have it. The path to securing a personal loan without salary slip UK options might seem daunting at first, but with the right approach and a clear understanding of what lenders are looking for, it’s absolutely achievable. It’s about presenting your financial story in a way that makes sense to them, proving your reliability through alternative means. Don’t let the lack of a traditional payslip deter you from exploring your options. With careful planning and smart choices, you can navigate this landscape and find the financial support you need. Just remember to always borrow responsibly and ensure any loan you take out is affordable for your unique circumstances. You’ve got this.