Let’s be honest, the idea of getting a new set of wheels when your credit score isn’t exactly sparkling can feel like trying to solve a Rubik’s Cube blindfolded. You’re probably thinking, “Is a car loan approval with low credit score USA even possible?” I hear you. It’s a common worry, and frankly, a lot of folks in the same boat feel stuck before they even start. But here’s the thing: it’s not impossible. It just requires a different playbook, a bit more strategy, and knowing exactly where to look and what to say.

I’ve seen countless people navigate this maze, and what fascinates me is how often a few simple, actionable steps can turn a ‘no’ into a ‘yes’. My goal today isn’t just to tell you it can be done, but to walk you through how it’s done. Think of me as your personal guide, sitting across from you with a coffee, sharing the insider tips that lenders don’t always advertise. We’re going to break down the process, step-by-step, so you can increase your loan approval chances and drive away in that car you need (or simply want!).

Understanding Your Credit Score (And Why It Matters for a Car Loan)

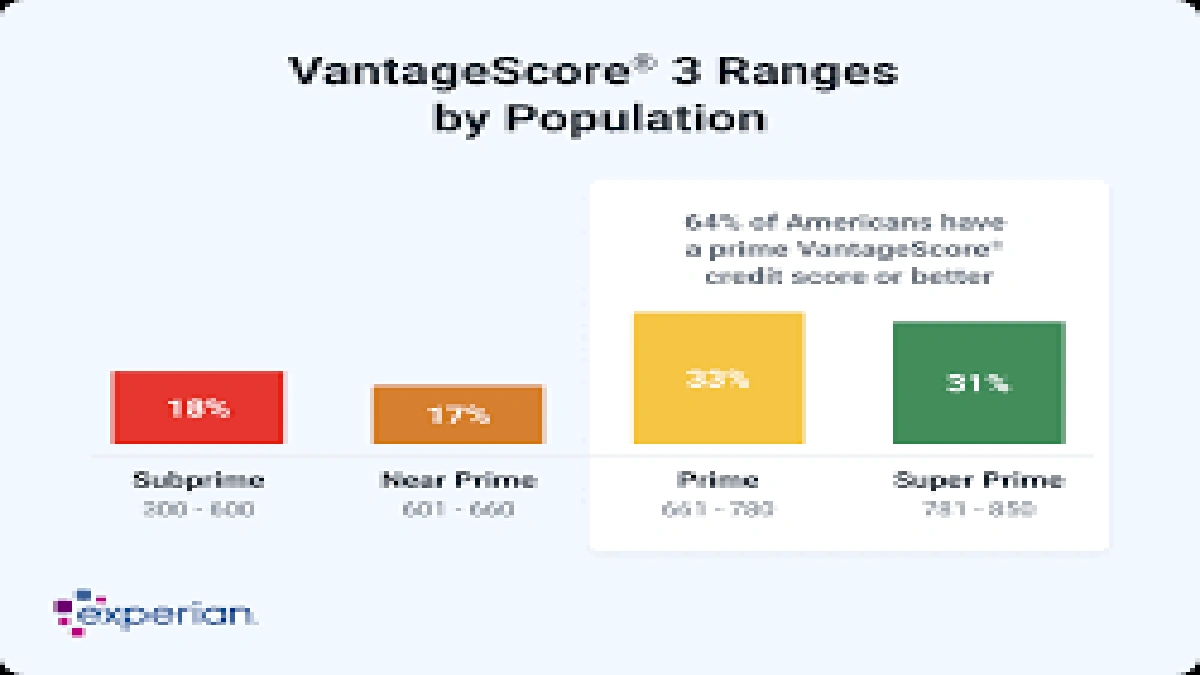

First off, let’s demystify that three-digit number that seems to hold so much power: your credit score. In the USA, this number (typically FICO or VantageScore) is a snapshot of your financial reliability. A “low” score usually means anything below 620-660, though some lenders consider anything under 600 as truly subprime. This score tells lenders how risky it might be to lend you money. The lower the score, the higher the perceived risk, and consequently, the higher the interest rates you’re likely to be offered (if approved at all).

But why does it matter so much for an auto loan specifically? Well, a car is a significant asset, and lenders want assurance they’ll get their money back. Your credit history, reflected in that score, shows your past payment behavior. If you’ve missed payments, defaulted on loans, or have a high credit utilization, it signals caution. However, understanding why your score is low is the first step towards getting around it. Is it a few late payments from years ago? Or something more recent? Knowing this helps you explain your situation and, more importantly, target areas where you can start toimprove credit scorefor car loan over time. Yes, even if you need a car now, every little bit helps in the long run.

The “How-To” Guide | Navigating Car Loan Approval with Low Credit

Alright, let’s get to the practical stuff. This is where we roll up our sleeves and tackle the challenge of securing a bad credit car loan. It’s not about magic; it’s about preparation and strategy.

Step 1 | Know Your Numbers – Pull Your Credit Report

Before you even think about stepping onto a dealership lot, get a copy of your credit report from all three major bureaus (Experian, TransUnion, and Equifax). You can do this for free once a year at AnnualCreditReport.com. Why? Because errors happen! I’ve seen countless cases where a simple mistake on a report was dragging down someone’s score. Dispute any inaccuracies immediately. Beyond that, it helps you understand your financial landscape. What accounts are open? What’s your debt-to-income ratio? This knowledge is power for your loan application.

Step 2 | Save for a Substantial Down Payment

This is arguably one of the most impactful steps for anyone seeking car loan approval with low credit score USA. A larger down payment directly reduces the amount you need to borrow, which in turn reduces the lender’s risk. If you can put down 10-20% (or more!) of the car’s value, you instantly become a more attractive borrower. It shows commitment and reduces the loan-to-value ratio, making lenders much more comfortable with the prospect of offering bad credit auto loans. Seriously, a soliddown payment for bad credit car loancan be a game-changer.

Step 3 | Consider a Co-Signer

If you have a trusted friend or family member with excellent credit, asking them to be a co-signer could significantly boost your chances. A co-signer essentially pledges to repay the loan if you default, adding their strong credit history to your application. This reduces the lender’s risk dramatically. However, understand the gravity of this: it impacts their credit, too, and if you miss payments, it affects both of you. So, choose wisely and ensure you’re absolutely confident in your ability to make payments. This isn’t a decision to take lightly for either party.

Step 4 | Explore Different Lender Types

Don’t just walk into the first dealership you see and expect the best deal. For those with lower credit, exploring various financing options is crucial. Think beyond traditional banks:

- Credit Unions: Often more forgiving and community-focused than big banks, sometimes offering better rates for members.

- Online Lenders: Many specialize in subprime auto lenders and low-credit loans, and they can offer quick pre-approvals. Companies like Capital One Auto Finance or MyAutoLoan are good places to start.

- Dealership Financing Bad Credit: While convenient, dealership financing (especially buy-here, pay-here lots) can come with very high interest rates. However, some larger dealerships have relationships with multiple lenders and might find a fit for you. Just be cautious and compare offers.

Step 5 | Be Realistic About Vehicle Choice

This might sting a little, but it’s important. When you have a low credit score, aiming for a brand-new, luxury vehicle is likely out of reach – at least for now. Focus on reliable, affordable used cars. A less expensive car means a smaller loan amount, which again, reduces risk for the lender and makes your payments more manageable. The goal here is to get approved, build a positive payment history, and improve your credit for future purchases. Think practical, not aspirational, for this first step.

Step 6 | Get Pre-Approved

Getting pre-approved for a loan before you visit a dealership is like having a secret weapon. It gives you a clear budget, shows you’re serious, and empowers you to negotiate the car price without feeling pressured by the financing. Lenders will do a soft credit inquiry for pre-approval, which doesn’t hurt your score. Once you have a pre-approval in hand, you know what kind of auto loan you can get, and you can compare it to any offers the dealership might present.

Step 7 | Negotiate Smart

When you’re at the dealership, remember to negotiate the car price and the financing terms separately. Don’t let them roll everything into one confusing package. If you have a pre-approval, use it as leverage. Be prepared to walk away if the terms aren’t right. There’s always another car and another lender. This is where your preparedness truly pays off.

Beyond the Loan | Rebuilding Your Credit for the Future

Securing a car loan approval with low credit score USA is a victory, but it’s also an opportunity. This loan, if managed responsibly, can be a powerful tool for rebuilding your credit. Make every single payment on time, every month. Seriously, this is non-negotiable. Consistent, on-time payments are the fastest way toimprove credit scoreover time. As your score improves, you’ll gain access to better financing options and lower interest rates for future loans, whether it’s another car, a home, or even just a credit card. It’s a journey, not a sprint.

FAQs | Your Burning Questions Answered

Can I get a car loan with a credit score below 500?

While challenging, it’s not impossible. You’ll likely face higher interest rates and may need a significant down payment or a co-signer. Exploring specialized subprime auto lenders or credit unions might yield better results than traditional banks.

How much of a down payment do I need for a bad credit car loan?

There’s no fixed rule, but generally, the more, the better. Aim for at least 10-20% of the car’s price. A larger down payment reduces the loan amount and signals financial stability to lenders, significantly improving your loan approval chances.

Will applying for multiple car loans hurt my credit score?

Multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, minimizing the impact on your credit score. This allows you to rate-shop for the best auto loan without undue worry.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a soft inquiry, giving you an estimate of what you might qualify for without impacting your score. Pre-approval involves a hard inquiry and means a lender has conditionally agreed to lend you a specific amount at a certain rate, subject to final verification. Always aim for pre-approval.

Can I get a car loan without a co-signer if I have bad credit?

Yes, it’s possible. Focus on maximizing your down payment, demonstrating stable income, being realistic about the car you choose, and exploring lenders who specialize in bad credit auto loans. A co-signer helps, but it’s not the only path.

How long does it take to get a car loan approved with low credit?

With online lenders, pre-approval can happen in minutes. The full approval process, once you’ve selected a vehicle and submitted all documentation, can range from a few hours to a couple of days. Being prepared with all necessary documents (ID, proof of income, residence) speeds things up.

The Road Ahead | Drive with Confidence

So, there you have it. Getting car loan approval with low credit score USA isn’t a myth; it’s a mission that requires strategy, patience, and a bit of savvy. By knowing your credit, saving for a down payment, exploring all your lender options, and being realistic about your purchase, you’re not just getting a car – you’re taking a significant step towards financial empowerment. Remember, this isn’t just about a transaction; it’s about building a stronger financial future, one responsible payment at a time. Go forth, prepare well, and get ready to hit the road!