Let’s be honest, the phrase ” personal loan instant approval no credit check UK ” sounds like a financial magic wand, doesn’t it? Especially when you’re in a tight spot, facing an unexpected bill, or just need a bit of a financial breather. The idea of getting money quickly, without the dreaded scrutiny of your credit history, is incredibly alluring. But here’s the thing, and I want to be upfront with you: the reality is a lot more nuanced, and frankly, a bit more complex, than those catchy headlines suggest. As someone who’s seen countless individuals navigate the choppy waters of UK finance, I can tell you that understanding what’s truly on offer, and what’s not, is your first and most crucial step.

My goal isn’t to burst your bubble entirely, but rather to equip you with the knowledge to make genuinely informed decisions. We’re going to pull back the curtain on these seemingly too-good-to-be-true offers, explore what they actually entail, and crucially, guide you toward safer, more sustainable borrowing options UK that won’t leave you in a worse position than when you started. Think of me as your guide through this particular financial maze.

Decoding “No Credit Check” | The FCA’s Stance and Your Options

When you see “no credit check” advertised for a loan in the UK, it’s vital to understand the regulatory landscape. The Financial Conduct Authority (FCA) is pretty clear: all lenders in the UK, by law, must conduct affordability assessments. This isn’t just a suggestion; it’s a requirement designed to protect you from taking on debt you can’t reasonably repay. So, how do some lenders claim “no credit check”? Well, it’s often a bit of a linguistic dance.

What they usually mean is that they might perform a “soft credit check” initially. This type of check doesn’t leave a visible mark on your credit file, so it doesn’t impact your credit score . It allows them to get a preliminary idea of your financial situation without affecting your future credit applications. However, if you proceed with the application, a full, “hard” credit check is almost always performed before final approval. This is non-negotiable for FCA regulated lenders UK because it’s part of their responsible lending obligations. Any lender promising truly “no credit check” for a significant sum without any assessment is likely operating outside of these regulations, which is a massive red flag.

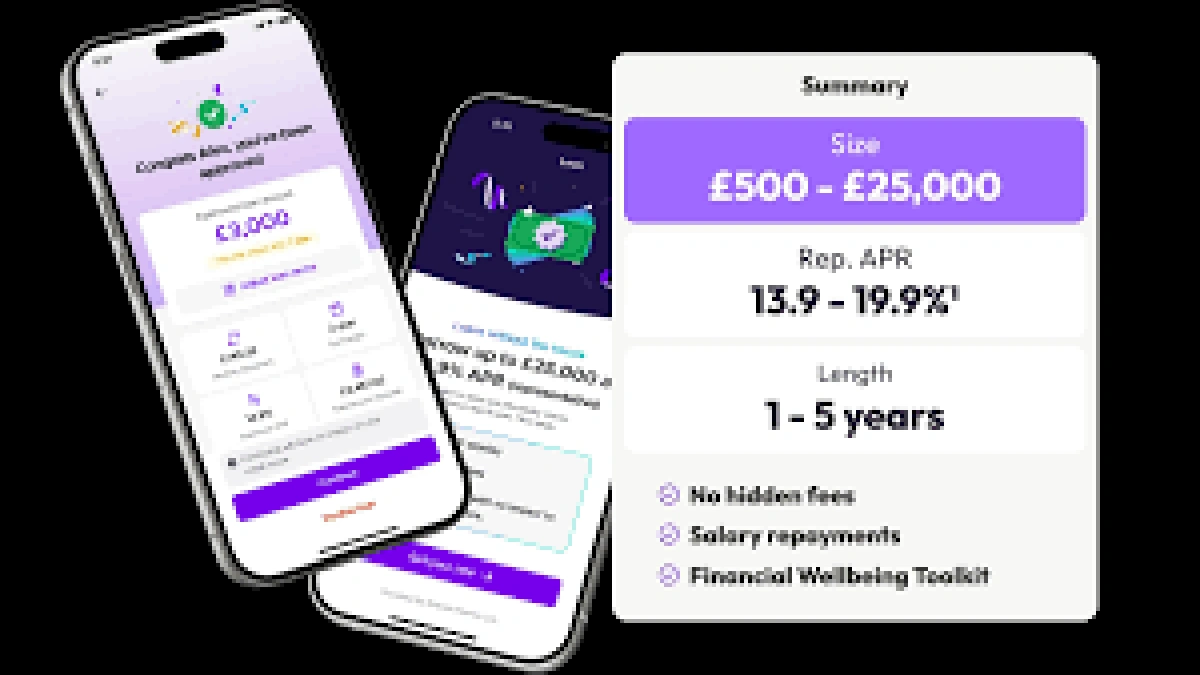

So, if you have a less-than-perfect credit history and are looking for solutions, you’re likely looking for bad credit loans UK . These are legitimate products offered by many lenders who specialize in assisting individuals with lower credit scores. They understand that life happens, and a past financial misstep shouldn’t permanently bar you from accessing finance. The key difference here is that they do perform credit checks, but their criteria are often more flexible, and they might look at other factors like your current income and outgoings more heavily. You might also encounter `short term loans no credit check` advertised, but again, be wary. These are typically high-interest loans for small amounts and very short repayment periods, and while they might have a quicker initial process, a full check is still usually part of the final approval.

The Pitfalls of “Guaranteed Approval” and High-Cost Loans

Another phrase that often accompanies “no credit check” is ” guaranteed approval loans UK .” And frankly, this is another siren song you need to be extremely cautious of. No reputable lender can guarantee approval without first assessing your ability to repay. It’s simply not how responsible lending works. If someone is promising you guaranteed money, they are either not legitimate, or they are setting you up for a loan with incredibly punitive terms.

The danger with these types of offers often lies in the fine print. While you might get seemingly “instant” access to funds, the cost can be astronomical. We’re talking about extremely high-interest rates, sometimes daily interest, and hidden fees that can quickly turn a small loan into an unmanageable debt. I’ve seen too many people fall into this trap, believing they’ve found a quick fix, only to find themselves struggling to keep up with repayments. This is why understanding loan eligibility UK is so crucial. A legitimate lender will always be transparent about their criteria and the total cost of the loan upfront.

Before you consider any loan that seems to bypass the usual checks, I strongly recommend consulting an independent body like Citizens Advice. They offer invaluable, free advice on debt and money, helping you understand your options without any pressure. You can find more information on their website: Citizens Advice – Borrowing Money . They can help you identify if a loan is genuinely suitable for your situation or if there are safer alternatives.

Smarter Moves | Building Credit and Exploring Safer Borrowing Options UK

So, if the “no credit check, instant approval” avenue is largely a myth or a high-risk gamble, what are your real options, especially if your credit score isn’t where you want it to be? The good news is, there are several proactive steps you can take to improve your financial standing and access more favourable lending terms in the long run.

One excellent strategy is to look into credit builder loans or credit builder credit cards. These are specifically designed to help you establish or repair your credit history. Typically, you borrow a small amount, and the repayments are reported to credit reference agencies. By consistently making on-time payments, you slowly but surely improve your credit score impact , opening doors to better financial products. It’s a marathon, not a sprint, but it’s a far more sustainable path than high-cost, short-term solutions.

Another crucial step is to engage with reputable direct lenders UK . These are companies that lend their own money directly to you, rather than acting as a broker. While brokers can sometimes be helpful, going directly to a lender often provides more clarity on terms and conditions, and you can build a direct relationship. Always check if they are on the FCA register – which we’ll discuss more in a moment. For those looking at larger financial commitments, understanding how to secure the best rates is key. You might find our insights on best mortgage lenders for first-time buyers UK helpful, as the principles of responsible borrowing and credit health often overlap, even for different loan types.

Navigating Emergency Needs | When Short Term Finance UK Makes Sense (and When It Doesn’t)

Life throws curveballs, and sometimes you need funds fast. This is where legitimate emergency loans UK or other forms of short term finance UK can be a lifeline, provided you approach them with caution and a clear understanding of the terms. These are typically smaller loans designed to be repaid quickly, often within a few months.

When considering short-term options, always prioritize FCA regulated lenders. They are held to strict standards, including transparent pricing, fair treatment of customers, and conducting proper affordability checks. Look for lenders who clearly display their interest rates (APR) and any fees. Never, and I mean never, take out a loan if you’re unsure about your ability to repay it on time. The penalties for missed payments on short-term loans can be severe, quickly escalating your debt.

To verify if a lender is legitimate and regulated, you can always check the Financial Services Register on the FCA’s official website. This is an indispensable tool for protecting yourself from unscrupulous operators: FCA Financial Services Register . Knowing your lender is on this register provides a significant layer of trust. And while we’re on the topic of securing finance for different needs, it’s worth noting that the principles of robust financial planning extend to all areas, whether you’re seeking personal funds or even exploring business expansion loan options – due diligence is always paramount.

Your Burning Questions Answered

Are there truly personal loan instant approval no credit check UK options?

In the strict sense of “no credit check,” no. All legitimate, FCA-regulated lenders in the UK must perform some form of affordability assessment, which typically includes a hard credit check for final approval. Offers of “no credit check” usually refer to soft checks or are from unregulated lenders, which you should avoid.

What are the risks of `short term loans no credit check`?

The primary risks include extremely high-interest rates, hidden fees, and the potential to fall into a debt cycle if you can’t repay on time. Many such loans are marketed by unregulated entities that don’t adhere to responsible lending practices, leaving consumers vulnerable.

How can I improve my credit score for future loans?

Focus on making all your payments (loans, credit cards, bills) on time, keeping credit utilization low, registering on the electoral roll, and checking your credit report for errors. Consistently demonstrating good financial habits will gradually improve your credit score impact .

Where can I find `FCA regulated lenders UK`?

You can find a comprehensive list of all authorized and regulated financial service firms, including lenders, on the Financial Services Register on the official FCA website (fca.org.uk). Always cross-reference any lender you’re considering.

What are `alternatives to no credit check loans`?

Safer alternatives include bad credit loans from regulated lenders, credit builder loans , borrowing from credit unions, local authority welfare schemes, or seeking debt advice from free services like Citizens Advice. These options prioritize your long-term financial health.

So, what’s the ultimate takeaway here? It’s this: while the allure of a ” personal loan instant approval no credit check UK ” is powerful, the reality is that genuine, safe, and regulated lending in the UK always involves a degree of scrutiny. That scrutiny isn’t there to frustrate you; it’s there to protect you. My strongest advice is to always prioritize transparency, legitimate regulation, and a clear understanding of your repayment capacity. Don’t chase the illusion of instant, unchecked money. Instead, invest your time in finding a sustainable solution that supports your financial well-being, both today and tomorrow. Your future self will thank you for it.