You’ve got that brilliant business idea, the passion, the grit. You’re working tirelessly, pouring your soul into your venture. But then, it hits you: the dreaded loan application form. And there it is, staring back at you – the requirement for GST proof. For countless small business owners and startups in India, this single hurdle can feel like an insurmountable mountain, dashing dreams before they even take flight. But here’s the thing , what if I told you that not having GST proof doesn’t have to be the end of your funding journey?

As someone who’s seen the Indian financial landscape evolve dramatically, I understand the frustration. Traditional lenders often rely heavily on GST returns as a primary indicator of a business’s legitimacy and turnover. It’s their way of verifying your financial health, your operational history, and ultimately, your ability to repay. But what if you’re a brand new startup, operating below the GST threshold, or simply navigating the initial, often chaotic, phases of growth? That’s exactly what we’re going to dissect today. We’ll explore how you can secure a business loan without GST proof India , and why looking to UK alternatives might not be the practical solution you initially thought.

The GST Conundrum | Why Lenders Ask (and Why You Might Not Have It)

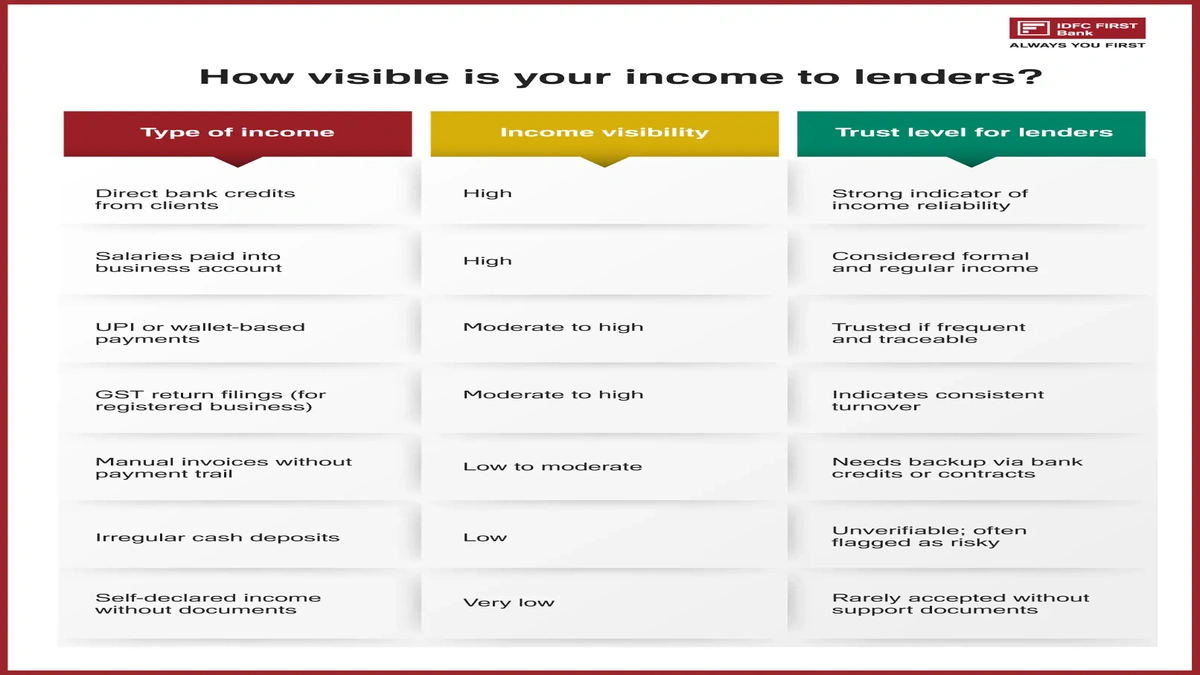

Let’s start with the ‘why’. Why is GST proof such a big deal for lenders? Well, for banks and Non-Banking Financial Companies (NBFCs), GST returns provide a clear, standardized snapshot of your business activity. They show your sales, purchases, and tax payments, offering a verifiable trail of your business’s financial transactions. It’s like a financial report card, simplifying the risk assessment process. Without it, traditional lenders often feel like they’re flying blind, leading to a quick rejection.

However, the reality on the ground in India is often different. Many budding entrepreneurs, especially those in micro-enterprises or rural sectors, operate below the GST registration threshold. Some are service providers with minimal physical goods movement, others are just starting out and haven’t hit the turnover mark, and a significant portion still conducts business with a blend of formal and informal transactions. To ask these businesses for GST proof is, frankly, to exclude a massive segment of India’s entrepreneurial spirit from formal credit. It’s a classic catch-22: you need funding to grow, but you can’t get funding without the proof of growth that funding would enable!

This gap in the traditional lending model is precisely where innovation steps in. The good news is, the financial ecosystem in India is dynamic, and new pathways for funding are emerging specifically for those who struggle with conventional documentation.

Unlocking Alternatives | Business Loans Without GST Proof in India

Okay, so you don’t have GST proof. Does that mean you’re out of options? Absolutely not! This is where you need to be smart, strategic, and open to exploring avenues beyond your typical bank branch. The market is evolving, and with it, the loan eligibility criteria .

1. The Rise of Fintech Lenders and Alternative Lending Platforms

This is arguably your strongest bet. Digital lenders andalternative lending platformsare disrupting the traditional banking model. Instead of solely relying on GST statements, they leverage a broader spectrum of data points to assess creditworthiness. What kind of data, you ask? Think:

- Bank Statements: Consistent cash flow, even without GST, can speak volumes. They’ll scrutinize your current account statements for the last 6-12 months.

- Payment Gateway Data: If you accept digital payments (Paytm, Google Pay, Razorpay, etc.), these platforms can analyze your transaction history, providing a clear picture of sales volume.

- E-commerce Sales Data: Selling on Amazon, Flipkart, or your own online store? Your sales data can be a powerful indicator of your business’s health.

- Utility Bills & Rent Receipts: Proof of consistent payments shows responsibility.

- Personal Credit Score (CIBIL): Even if your business lacks formal history, a strong personal credit score can significantly boost your chances for unsecured business loans India, especially for sole proprietorships or smaller firms. Much like how your history with an education loan interest rates India can impact future lending, your personal financial discipline matters.

- Proprietary Algorithms: Many fintech loans India providers use sophisticated AI and machine learning to analyze these diverse data points, giving them a more holistic view of your business than traditional methods.

These platforms are tailor-made forMSMEsand startups that might not fit the conventional mold. They often offer micro-loans for small businesses with quicker disbursement times.

2. Government Schemes & MSME Loans Without Collateral

India has several government-backed schemes aimed at promoting small businesses and entrepreneurship. While some may still require basic business registration, many are designed to be more inclusive. The Pradhan Mantri Mudra Yojana (PMMY) is a prime example, offering loans up to ₹10 Lakh to micro and small enterprises. While GST proof might be preferred, if your turnover is below the threshold, other documents like business registration (Udyam Aadhaar), income statements, and bank statements can often suffice. Similarly, exploring options like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) can facilitate MSME loans without collateral , significantly reducing the burden of physical asset pledges.

3. Peer-to-Peer (P2P) Lending

P2P platforms connect borrowers directly with individual investors. The lending criteria here can be more flexible, as individual lenders might be more willing to take on perceived higher risk in exchange for better returns. While you’ll still need to demonstrate repayment capacity, the documentation requirements can be less rigid than traditional banks.

4. Angel Investors & Venture Capital for Startup Funding India

If your business has a high-growth potential, particularly in technology or innovative sectors, seeking equity funding from angel investors or venture capitalists (VCs) is another avenue. This isn’t a loan, but an investment in exchange for ownership stakes. Here, your business plan, market potential, team, and traction are far more important than GST proof. This is a different ball game entirely, focused on scale and future returns, and a significant pathway for startup funding India .

Beyond Borders? The UK Alternative (and Why It’s Tricky for India)

Now, let’s address the ‘UK alternatives’ part of your query. It’s an interesting thought, isn’t it? If India is rigid, why not look elsewhere? The truth, however, is that for a business primarily operating in India and lacking fundamental documentation like GST proof, securing a loan directly from a UK-based lender is often impractical, if not impossible. Here’s why:

- Jurisdiction & Legal Entity: UK lenders primarily serve UK-registered businesses. To get a loan, you’d typically need a UK legal entity, a UK bank account, and demonstrable operations within the UK. This isn’t just about documents; it’s about legal and operational presence.

- KYC & Compliance: Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are stringent globally. A UK lender would face immense challenges verifying an Indian business without local presence or substantial documentation, including proof of tax compliance (like VAT, which is the UK equivalent of GST).

- Currency & Repayment Risk: Managing currency exchange rates and the logistics of international repayments adds significant complexity and risk for both lender and borrower.

- Collateral & Guarantees: Even if you could theoretically get a loan, securing it (if collateral is required) across international borders is a legal and logistical nightmare.

So, while the UK has its own vibrant alternative lending scene, it’s generally not a viable direct route for an Indian business struggling to get a loan without local tax proof. Unless you’re a highly scalable Indian startup looking for global VC funding (which is equity, not a loan, and a very different process), focusing your efforts on the rapidly evolving Indian fintech and government scheme ecosystem is a far more pragmatic approach. It’s like considering aused car loan interest rates USAif you live in Delhi and primarily drive in India; the systems and requirements just don’t align for direct application.

Strategies for Success | Boosting Your Chances

Even if you lack GST proof, you can significantly improve your chances by presenting a strong case using other means:

- Maintain Impeccable Bank Records: Clean, consistent bank statements showing regular transactions, sales, and expenses are critical. Avoid sudden large deposits or withdrawals that look suspicious.

- Develop a Robust Business Plan: A well-articulated business plan demonstrating market understanding, revenue projections, and repayment strategy can sway lenders, especially newer ones.

- Show Digital Presence & Sales: If you sell online or have a strong digital footprint, highlight it. Lenders are increasingly interested in your online reputation and customer engagement.

- Strengthen Your Personal Credit Score: As mentioned, your personal CIBIL score is crucial for small businesses. Pay personal EMIs and credit card bills on time.

- Keep Other Documents Ready: Udyam Aadhaar registration, shop and establishment license, local municipality permits, partnership deed (if applicable), PAN card, Aadhaar card – all these contribute to your legitimacy.

- Explore Invoice Discounting/Factoring: If you have invoices from reputable clients, you can get immediate cash by selling these invoices to financial institutions at a small discount. This isn’t a loan, but a way to manage working capital.

The journey to securing funding without conventional documents like GST proof might require a bit more effort and research, but it’s far from impossible. The Indian financial market is ripe with innovative solutions for the ‘new-age’ entrepreneur. Focus on building a transparent financial history through other means, and leverage the growing number of lenders who understand that a great business idea doesn’t always come with a perfect paper trail from day one.

Frequently Asked Questions About Business Loans Without GST Proof

What documents are typically accepted instead of GST proof?

Many lenders accept recent bank statements (6-12 months), Aadhaar card, PAN card, business registration proof (like Udyam Aadhaar), proof of address, income tax returns (personal or business, if filed), and sometimes payment gateway transaction history or e-commerce sales reports.

Are these alternative loans more expensive?

Potentially, yes. Lenders taking on higher perceived risk (due to lack of conventional documentation) might charge slightly higher interest rates. However, the exact rates depend on the lender, your creditworthiness, and the loan product.

Can I get an unsecured business loan without GST proof?

Yes, absolutely. Many fintech lenders and NBFCs specialize in providing unsecured business loans India based on alternative data points and without requiring collateral or GST proof. Your bank statements and personal credit score become very important here.

What is the typical repayment period for these loans?

Repayment periods can vary widely, from short-term daily or weekly repayments (especially for smaller micro-loans or daily revenue-based financing) to more conventional monthly EMIs over 12-36 months for larger amounts. It largely depends on the lender and the specific loan product.

Is a strong personal CIBIL score crucial if my business doesn’t have GST?

Yes, for sole proprietorships and smaller firms, your personal CIBIL score is extremely crucial. It acts as a proxy for your financial discipline and creditworthiness, significantly influencing a lender’s decision when business-specific documentation is limited.

Are there any government schemes specifically for businesses without GST registration?

Yes, schemes like the Pradhan Mantri Mudra Yojana (PMMY) are designed to support micro and small enterprises, and while GST is preferred for some larger loan amounts, smaller loans under Shishu and Kishore categories often have more flexible documentation requirements, focusing on Udyam Aadhaar, bank statements, and business proposals.