Let’s be honest, the dream of studying abroad is thrilling. But then reality bites: the costs. And for many of us, especially Indian students eyeing universities overseas, the biggest hurdle isn’t just tuition – it’s securing an education loan without a cosigner. I’ve seen countless aspirants grapple with this. It feels like a Catch-22, doesn’t it? You need the loan to get the visa, but you need a cosigner, often with a robust local credit history, to get the loan. But what if I told you there are legitimate pathways, often overlooked, to make this dream a reality?

This isn’t just about listing banks. This is about understanding the ‘how’ – the strategies, the mindset shift, and the often-hidden doors that open up for those who know where to look. Forget the standard advice; we’re going to dive deep into securing an education loan without a cosigner for international students, cutting through the noise and giving you actionable steps. Think of me as your guide, navigating the complex world offinancial aid for overseas study.

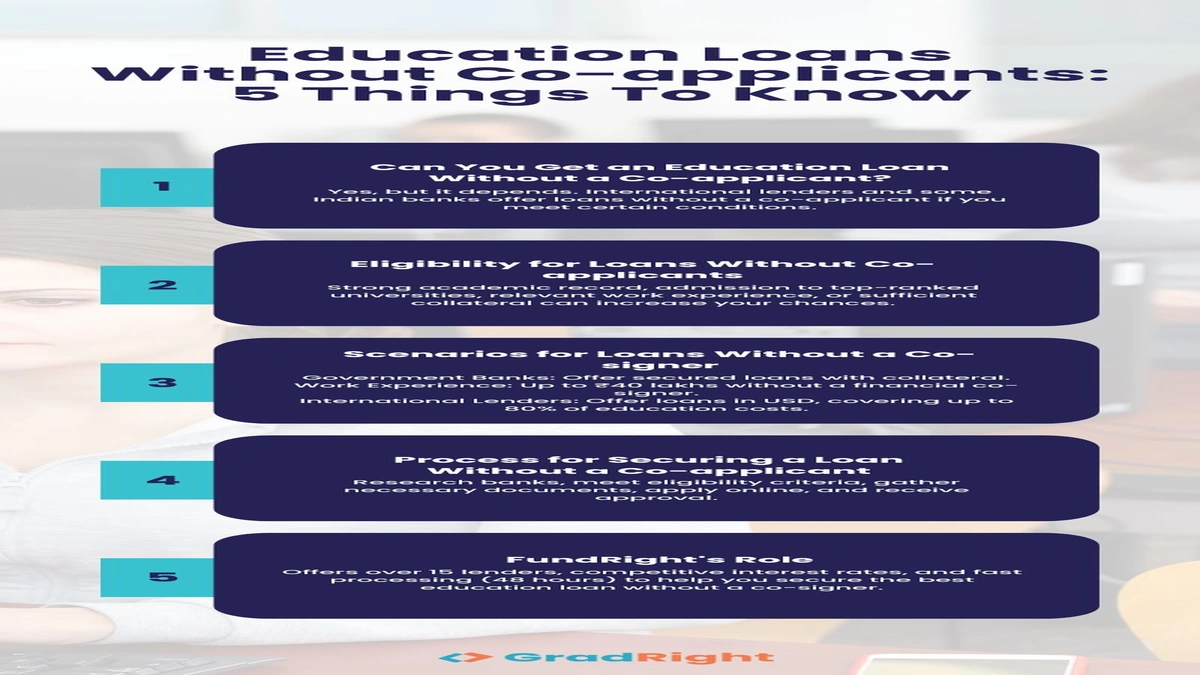

The Cosigner Conundrum | Why It’s a Hurdle and How to Leap It

Why do lenders insist on a cosigner in the first place? It boils down to risk. As an international student, you likely don’t have a credit history in your destination country. Your future income, while promising, isn’t guaranteed in the eyes of a foreign lender. A cosigner, typically a citizen or permanent resident of the destination country, acts as a guarantor, pledging to repay the loan if you can’t. This significantly reduces the lender’s risk.

But here’s the thing: not everyone has a relative or close friend living abroad with a stellar credit score willing to take on that responsibility. And that’s perfectly okay. What many don’t realize is that the market for international student loans USA and other popular study destinations has evolved. There are specialized lenders who’ve recognized this gap and developed products specifically designed for students like you.

The key isn’t to bypass the need for assurance, but to find lenders who accept alternative forms of assurance. This could be based on your academic merit, your chosen course’s future earning potential, or a unique underwriting model. It’s about presenting yourself as a low-risk investment, even without that local cosigner.

Charting Your Course | Pathways to No-Cosigner Loans

So, how do you actually get one of these elusive loans? It typically involves focusing on lenders who specialize in loans for Indian students without cosigner or who offer specific programs for international students. Here are the main avenues:

1. Merit-Based Lenders | Your Grades are Your Gold

Many specialized lenders focus heavily on academic merit. If you have a strong academic record (high GPA, competitive test scores like GRE/GMAT/SAT), they see you as a lower risk. Why? Because historically, students with strong academic backgrounds tend to complete their degrees and secure high-paying jobs, making them more likely to repay their loans. These lenders often look at the reputation of your chosen university and the career prospects of your field of study.

2. Future Income-Based Lending | Betting on Your Potential

This is a fascinating model, particularly relevant for graduate students in high-demand fields like STEM. Some lenders assess your potential future earnings based on your program, university, and career projections. They underwrite the loan assuming you’ll land a well-paying job after graduation. This requires detailed information about your course, its duration, and estimated post-graduation salaries in your field. This is essentially a sophisticated form of unsecured lending, focusing on your human capital.

3. Loans with Collateral (Non-Traditional) | An Indirect Cosigner Alternative

While the focus is on no-cosigner, some international students might have access to collateral in India (e.g., property, fixed deposits) that Indian banks might accept for an education loan without collateral in the destination country. This isn’t strictly a ‘no-cosigner’ loan in the traditional sense, but it bypasses the need for an international cosigner, which is often the biggest hurdle. This means you’re essentially securing the loan against assets back home, allowing you tostudy abroad loan without collateralin the host country.

Decoding the Lender Landscape | Who Offers What?

The landscape of no cosigner student loans for international students is constantly evolving. While traditional banks in your destination country might be a tough nut to crack without a local cosigner, several niche lenders have emerged as game-changers. Names like MPOWER Financing and Prodigy Finance are often at the forefront of this discussion, though others exist.

- MPOWER Financing: Known for merit-based lending, they often don’t require a cosigner or collateral. They look at your academic success and career path. Their focus is often on students attending highly-ranked universities and pursuing degrees that lead to strong employment prospects. This aligns perfectly with the future income-based model we discussed.

- Prodigy Finance: Similar to MPOWER, Prodigy Finance offers loans to international graduate students (primarily MBA, Masters in Engineering, Public Policy, etc.) at top universities without requiring a cosigner or collateral. They assess your future earning potential.

- Sallie Mae/Discover/College Ave (with caveats): While these are major US lenders, obtaining a loan from them typically does require a US citizen or permanent resident cosigner. However, it’s worth noting their existence as a comparison point, and occasionally, specific programs or university partnerships might offer exceptions or alternatives, so always check with your university’s financial aid office.

It’s crucial to compare interest rates, repayment terms, and disbursement processes across multiple lenders. What works for one student’s program or university might not be the best fit for another. Always read the fine print!

Application Arsenal | Preparing for Success

Applying for an education loan without a cosigner demands meticulous preparation. Think of it as building your case. Here’s what you’ll generally need:

- Admission Letter: This is non-negotiable. Lenders need proof of your acceptance into a recognized institution.

- Academic Transcripts: Highlight your strong grades. This directly feeds into merit-based assessments.

- Proof of Identity: Passport, student visa (or proof of application), etc.

- Proof of Funds: Even if you’re getting a loan for the bulk, showing you have some personal funds or savings can strengthen your application.

- GRE/GMAT/SAT Scores: If applicable, strong scores bolster your academic profile.

- University & Program Details: Lenders will want to know the cost of attendance, the duration of your program, and sometimes even the curriculum.

- Credit History (if any): While you may not have a local credit history, if you have a history in India or another country, sometimes lenders might consider it, though it’s less common for these specific no-cosigner products.

The loan eligibility criteria for international students can vary significantly between lenders. Some might have minimum GPA requirements, others might only fund students attending specific universities or studying particular fields. Don’t get discouraged if one lender says no; keep exploring! This is where persistence pays off. It’s often a case of finding the right fit, rather than a universal ‘yes’ or ‘no’.

Beyond Loans | Creative Funding Strategies for International Students

While the focus is on the education loan without cosigner, it’s wise to consider a holistic funding approach. Diversifying your sources can reduce your overall loan burden and make your financial journey smoother.

- Scholarships and Grants: Apply for every single one you’re eligible for! University-specific scholarships, external grants from foundations, and even government scholarships from your home country or destination country can significantly reduce the amount you need to borrow. This is truly financial aid at its best, as it doesn’t need to be repaid. For example, many universities offer specific grants for international students or those in STEM fields.

- Assistantships (Graduate Students): For Master’s and PhD students, research assistantships (RA) or teaching assistantships (TA) often come with a tuition waiver and a stipend. This is essentially a paid job within the university that helps cover your living expenses and reduces tuition costs.

- Part-time Work: Most student visas allow for part-time work during studies and full-time work during breaks. While this won’t cover major tuition costs, it can certainly help with living expenses, books, and day-to-day spending, easing the burden of your study abroad experience. Check the specific regulations of your student visa requirements for allowable work hours.

Combining these strategies can make a significant difference. Imagine reducing your loan by 20-30% through scholarships and part-time work – that’s a huge saving on interest over the years!

The Bottom Line | Your Dream is Achievable

Securing an education loan without a cosigner for international students isn’t a myth; it’s a challenge that many have overcome. It requires diligence, research, and a clear understanding of your unique profile and the evolving financial landscape. The days of a cosigner being an absolute prerequisite for every international student loan are slowly fading, thanks to innovative lenders and specialized programs. Your academic potential, your chosen field’s demand, and your perseverance are powerful assets. So, arm yourself with information, prepare your application meticulously, and take that bold step towards your global education dream. It’s more within reach than you might think.

Frequently Asked Questions

Is it really possible to get an education loan without a cosigner as an international student?

Yes, absolutely! While challenging, specialized lenders like MPOWER Financing and Prodigy Finance offer education loan without cosigner options for international students, primarily based on academic merit and future earning potential.

What are the key eligibility criteria for such loans?

Eligibility often hinges on your academic record (GPA, test scores), the reputation of your university, your chosen field of study (especially high-demand fields like STEM), and your potential post-graduation income. Some lenders also have minimum loan amounts and specific country restrictions.

Will my interest rate be higher without a cosigner?

Generally, yes. Loans without a cosigner are considered higher risk by lenders, which often translates to higher interest rates compared to those with a strong co-signer or significant collateral. However, the exact rate depends on your profile, the lender, and prevailing market conditions.

How long does the application process typically take?

The loan application process can vary. Pre-qualification might be quick (a few minutes), but full application review and disbursement can take anywhere from a few weeks to several months. It’s always best to apply as early as possible once you have your acceptance letter.

Can I get a loan without collateral as well?

Many of the lenders who offer no-cosigner loans for international students also offer them without collateral. This is a key feature of merit-based and future income-based lending models, focusing on your human capital rather than physical assets.

What if my chosen university isn’t on a lender’s approved list?

If your university isn’t on one lender’s list, don’t despair. Different lenders have different approved university lists. You might need to explore other specialized lenders or look into alternative funding options like scholarships or loans from your home country that might accept Indian collateral.