Alright, let’s be honest. We’ve all been there, right? That moment when life throws a financial curveball, and you need cash, fast. Maybe it’s an unexpected medical bill, a sudden business opportunity, or even just consolidating some nagging debts. In India, two popular contenders often pop up when you’re looking for quick funds: the ever-reliable gold loan and the seemingly flexible personal loan . But here’s the thing – choosing between them isn’t as straightforward as picking your favourite chai. It’s a decision loaded with implications for your finances, your assets, and even your peace of mind. And what fascinates me is how many people jump into one without truly understanding the ‘why’ behind their choice, the hidden contexts, and the long-term ramifications.

This isn’t just about comparing interest rates; it’s about understanding the very DNA of these financial products and how they fit into the unique tapestry of an Indian household’s financial needs. We’re going to dive deep, peel back the layers, and figure out which one truly serves your purpose better. Because, let’s face it, your hard-earned money (or your family’s precious gold) deserves an informed decision, not a rushed one.

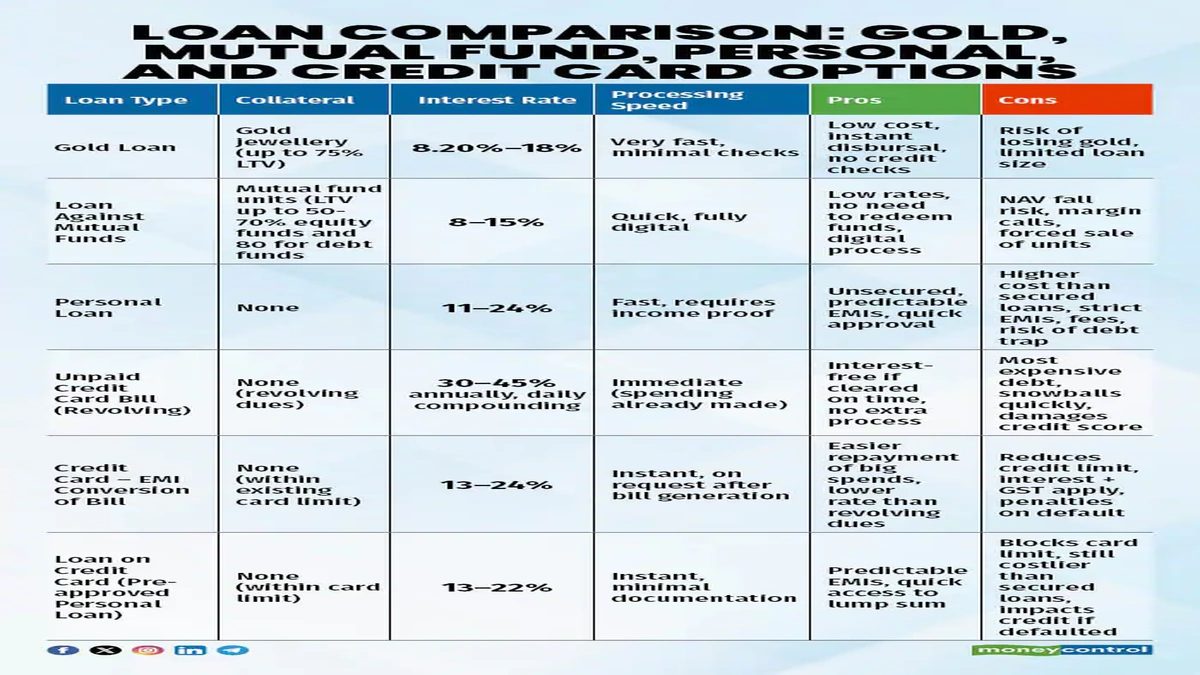

The Core Difference | Secured vs. Unsecured, and Why It Matters

At the heart of the gold loan vs personal loan comparison lies a fundamental distinction: collateral. Think of it like this: a secured loan is like borrowing money from a friend, and you give them your watch as a guarantee that you’ll pay them back. An unsecured loan? That’s when your friend trusts you purely on your word, or in the financial world, on your creditworthiness. That’s the difference between a secured loan (like a gold loan) and an unsecured loan (like a personal loan).

With a gold loan , you pledge your physical gold – jewellery, coins, biscuits – as collateral. This gold acts as security for the lender. If, for some reason, you can’t repay the loan, the lender has the right to auction your gold to recover their money. This reduces the risk for the lender significantly, which, as we’ll see, has a direct impact on the interest rates they offer and the ease of approval. According to financial experts, this risk mitigation is precisely why secured loans often come with more favourable terms. You can even read more about the general concept of collateralon Wikipedia.

A personal loan , on the other hand, requires no collateral. Your creditworthiness, primarily reflected in your CIBIL score and your income stability, is your only guarantee. This inherently makes it riskier for the lender. And what happens when there’s more risk? Well, the cost of borrowing usually goes up. This is a critical point to grasp, as it shapes everything from eligibility to the final amount you end up repaying.

Gold Loan | Your Family Heirloom as a Lifeline (or a Trap?)

Ah, the gold loan . For generations in India, gold has been more than just an ornament; it’s been a liquid asset, a symbol of wealth, and often, a silent saviour during financial distress. The beauty of a loan against gold is its speed. Need cash in a hurry? Walk into a branch with your gold, complete some minimal paperwork, and often, you can walk out with funds within hours, sometimes even minutes. This is a huge advantage when you’re facing an emergency.

The gold loan benefits are quite compelling: generally lower interest rates compared to personal loans because of the collateral, minimal documentation requirements (often just ID and address proof), and here’s a big one – your CIBIL score doesn’t play as dominant a role. Lenders are more concerned with the purity and weight of your gold than your past borrowing history. This makes it accessible even for those with a less-than-perfect credit history, or those who are new to credit.

However, it’s not all glitter. One of the main drawbacks is the sentimental value attached to gold. Many families view their gold as an heirloom, and the thought of losing it is distressing. While lenders don’t want to auction your gold, they will if you default. Also, the loan amount is typically a percentage of your gold’s market value, known as the Loan-to-Value (LTV) ratio, usually capped at 75-80%. So, if you have gold worth ₹1 lakh, you might only get ₹75,000-₹80,000. This might not be enough for larger financial needs. Plus, you need to be mindful of thegold loan interest rate today, as it can vary.

Personal Loan | The Freedom of Funds, But At What Cost?

Now, let’s talk about the personal loan . It’s often seen as the ultimate flexible friend. No collateral needed, which means your ancestral jewellery stays safe in your locker. You can use the funds for literally anything – a dream vacation, a wedding, home renovation, or even debt consolidation. The loan amounts can also be significantly higher than a gold loan, depending on your income and credit profile, making it suitable for bigger expenses.

But this freedom comes at a price. The most significant aspect is the higher interest rates . Since there’s no collateral, the lender is taking on more risk, and they price that risk into the interest. This can make the overall cost of a personal loan substantially higher over its repayment tenure . Furthermore, eligibility is much stricter. Lenders will scrutinize your CIBIL score with a magnifying glass. A low CIBIL score can lead to rejection or even higher interest rates. You’ll need a stable income, a good credit history, and usually a decent debt-to-income ratio.

The documentation process can also be more extensive, requiring salary slips, bank statements, IT returns, and more. And while some banks offer quick approval , the entire process, from application to disbursement, can take several days, sometimes even a week or two, which might not work if you’re in an urgent situation. These are the crucial personal loan drawbacks that often get overlooked in the allure of ‘no collateral’.

Beyond the Basics | Hidden Costs, Flexibility, and Repayment Realities

When you’re doing a gold loan vs personal loan comparison , it’s easy to just look at the advertised interest rates. But savvy borrowers know that the devil is in the details, specifically in the hidden costs and the fine print. Both types of loans can come with processing fees, which are usually a percentage of the loan amount. Some lenders might also charge pre-payment penalties if you decide to close your loan early. Always ask about these upfront!

Repayment tenure is another key differentiator. Gold loans often have shorter tenures, typically ranging from a few months to 3 years, with more flexible repayment options like bullet repayment (pay interest monthly, principal at the end) or EMI. Personal loans usually have longer tenures, from 1 to 5 years, sometimes even 7, with fixed EMIs. This longer tenure can make the monthly burden lighter but increases the total interest paid over time. It’s similar to how different factors influencecar loan interest rate comparison– the specifics truly matter.

What happens if you default? For a gold loan , after repeated reminders, your gold will eventually be auctioned. For a personal loan , defaulting will severely damage your CIBIL score, making it incredibly difficult to get credit in the future. Lenders might also initiate legal proceedings or engage collection agencies, which can be a stressful experience. Understanding these ‘what ifs’ is crucial for responsible borrowing.

Making the Right Choice | A Decision Tree for Your Wallet

So, how do you decide? There’s no one-size-fits-all answer, but we can create a little decision tree to guide you:

- Urgency and Speed: If you need quick access to funds within hours, a gold loan is often the winner.

- Collateral Availability & Sentiment: Do you have physical gold you’re comfortable pledging? Is its sentimental value less important than your immediate financial need? If yes, gold loan. If not, or if you prefer to keep your gold untouched, then a personal loan without collateral is your path.

- CIBIL Score & Credit History: Is your CIBIL score strong (750+)? Do you have a stable income? Then a personal loan is a viable option. If your CIBIL score is low or non-existent, a gold loan is likely easier to secure.

- Interest Rates & Overall Cost: Generally, gold loan interest rates are lower. If minimizing interest outflow is your top priority, and you have gold, lean towards a gold loan. Always compare the effective annual percentage rate (APR) including all fees.

- Loan Amount Needed: For very large sums that exceed the LTV of your gold, a personal loan might be the only option. For smaller to medium amounts, a gold loan is often sufficient.

- Repayment Flexibility: Consider your cash flow. If you prefer flexible repayment options or a bullet payment, a loan against gold might suit you. If consistent, fixed EMIs over a longer period work better, a personal loan is ideal.

Remember, this isn’t just about getting money; it’s about getting money on terms that work for your specific situation. My experience tells me that most financial troubles stem not from taking a loan, but from taking the wrong loan.

Your Burning Questions Answered

Is a gold loan always cheaper than a personal loan?

Generally, yes. Because a gold loan is a secured loan with collateral, the risk for the lender is lower, leading to lower interest rates. However, always compare the effective APR, which includes all fees, before making a final decision.

Can I get a personal loan with a low CIBIL score?

It’s challenging. Most banks require a good CIBIL score (typically 700-750+) for personal loan eligibility. With a low score, you might face rejection or be offered extremely high interest rates by alternative lenders.

What documents are typically needed for each?

For a gold loan , you usually need basic KYC documents (ID proof like Aadhaar/PAN, address proof). For a personal loan , expect to provide extensive documents including ID proof, address proof, income proof (salary slips, bank statements, IT returns), and employment verification.

What happens if I can’t repay my gold loan?

If you default on a gold loan , the lender will first try to contact you for repayment. If unsuccessful, they have the right to auction your pledged gold to recover the outstanding loan amount. This will also impact your credit score.

How quickly can I get funds from each?

A gold loan offers almost instant disbursement, often within a few hours, making it ideal for quick access to funds . A personal loan typically takes 2-7 working days, as it involves more extensive verification and approval processes.

Does a personal loan require collateral?

No, a personal loan is an unsecured loan , meaning it does not require you to pledge any asset as collateral. It’s approved based on your creditworthiness and income.

At the end of the day, both the gold loan and the personal loan serve as powerful financial tools. The key isn’t to declare one universally superior, but to understand their nuances and align them with your specific situation. Are you looking for the lowest interest rates and have gold to spare? A gold loan might be your best bet. Do you need a larger sum, prefer not to pledge assets, and have a stellar CIBIL score? Then a personal loan could be the answer. The real power lies in making an informed decision, one that respects your financial health and helps you navigate life’s unexpected turns with confidence. Don’t just borrow; borrow smart.