Let’s be honest, buying a home in India is a monumental dream for many of us. It’s not just bricks and mortar; it’s security, a legacy, a space to call your own. But here’s the thing: that dream often comes with a hefty price tag and, perhaps more daunting, the intricate maze of securing a home loan . The phrase “mortgage approval tips to get approved fast” isn’t just a search query; it’s a heartfelt plea from countless hopeful homebuyers. And if you’re reading this, you probably know that sinking feeling of uncertainty, the ‘will I or won’t I get it?’ anxiety.

I’ve seen it all, from first-time buyers overwhelmed by paperwork to seasoned investors trying to navigate fluctuating interest rates. What fascinates me is that while the goal is always the same – getting that loan approved quickly and smoothly – the path isn’t always clear. That’s why I’m here, sitting with you, metaphorically speaking, to walk you through the essential steps. We’re not just going to talk about what to do; we’re going to dive into how you can strategically position yourself for a swift and successful mortgage approval. Consider this your personal playbook.

The Foundation | Building Your Strongest Application from the Ground Up

Think of your mortgage application as your financial resume. Lenders in India, whether it’s SBI, HDFC, ICICI, or any other major bank, are looking for a compelling story of reliability and capability. The first, and arguably most crucial, chapter of that story is your CIBIL score for home loan . This three-digit number (ranging from 300-900) is your creditworthiness report card. A score of 750 or above is generally considered excellent and puts you in a strong position. Anything below that, and you might face higher interest rates or even rejection. So, before you even think about applying, pull your credit report. Check for errors, pay off small debts, and avoid applying for new credit cards just before your home loan application.

But it’s not just about your CIBIL score. Lenders also scrutinize your debt-to-income ratio (DTI). Simply put, this is the percentage of your gross monthly income that goes towards debt payments. Most banks prefer a DTI of 35-40% or lower. If too much of your income is already committed to other loans (car loans, personal loans, credit card EMIs), a bank will see you as a higher risk. This is where smart financial planning comes in. Can you pre-pay any existing loans? Can you consolidate debt? These moves significantly improve your DTI and, consequently, your home loan eligibility criteria .

Understanding eligibility isn’t just about your personal finances; it’s also about the loan product itself. Different loan types, much like understanding the nuances betweenSME business loan eligibility, have specific requirements. While SME loans cater to businesses, the core principle of demonstrating financial health and meeting specific criteria remains universal for all lending institutions. Be sure to research the specific eligibility for the home loan you’re eyeing.

Documents & Details | Don’t Let Paperwork Be Your Downfall

Oh, the paperwork! It’s the bane of many an applicant’s existence, but it’s also where you can truly shine. Having all your documents required for home loan ready, accurate, and organized is a game-changer for getting mortgage approval fast . I’ve seen applications get delayed by weeks, sometimes months, just because one crucial document was missing or had a minor discrepancy. Here’s a quick checklist of the essentials:

- Identity Proof: PAN Card, Aadhaar Card, Passport, Voter ID.

- Address Proof: Aadhaar Card, Passport, Utility Bills (latest).

- Income Proof (Salaried): Latest 3 months’ salary slips, 2 years’ Form 16, Latest 6 months’ bank statements (salary account).

- Income Proof (Self-Employed): Latest 3 years’ ITR with computation of income, Latest 3 years’ Balance Sheet & Profit & Loss A/c, Business Proof (e.g., Shop & Establishment Act Certificate), Latest 1 year’s bank statements (personal & business).

- Property Documents: Sale Agreement, Occupancy Certificate, Approved Plan, Title Deed.

My advice? Create a dedicated folder, physical and digital, and start gathering these well in advance. Cross-check every single detail. Ensure names match across all documents, dates are correct, and signatures are consistent. Any mismatch, however small, will raise a red flag and lead to requests for clarification, slowing down your loan application process significantly. An external resource like theState Bank of India’s home loan eligibility pagecan give you a general idea of the comprehensive list they require, and it’s a good benchmark for what most Indian banks will ask for.

The Money Talk | Down Payment and Strategic Financial Health

Beyond your eligibility and documents, the financial muscles you flex are paramount. The down payment for home loan is a critical factor. While banks can finance up to 80-90% of the property value, having a larger down payment reduces your loan amount, which in turn lowers your EMI and your overall risk profile in the eyes of the lender. For example, if you can put down 30% instead of 20%, you’re not just saving on interest; you’re also signaling strong financial discipline and readiness. This can often translate into a faster approval process and potentially better interest rates home loan India offers.

It’s all part of a broader strategy of financial planning home purchase . This isn’t just about saving for the down payment; it’s about anticipating other costs too – stamp duty, registration fees, processing fees, and even furniture. Having a buffer for these expenses ensures you don’t deplete your savings entirely and maintain financial stability post-purchase. Lenders appreciate this foresight. They want to see that you’re not just scraping by to make the EMI, but that you have a robust financial plan in place.

Strategic Moves | Pre-Approval and Expert Guidance for a Swift Outcome

One of the most potent weapons in your arsenal for getting a mortgage approved fast is a pre-approved mortgage . This isn’t a final loan, but it’s a conditional commitment from a lender based on your financial information. It tells you exactly how much you can borrow, giving you immense clarity and bargaining power when house hunting. More importantly, it streamlines the final approval process because a significant chunk of the verification (your income, credit, etc.) is already done. When you find your dream property, the bank only needs to evaluate the property itself, which drastically cuts down the time to final sanction.

Another often-overlooked strategy is seeking professional guidance. A good mortgage broker or a financial advisor specializing in home loans can be invaluable. They understand the nuances of various banks’ policies, can help you compare interest rates home loan India wide, and can even flag potential issues with your application before you submit it. They’re like your personal guide through the wilderness, helping you avoid pitfalls and choose the most efficient route. Much like comparingfederal vs private student loans comparison USA, understanding the different offerings and terms from various lenders is key to making an informed decision, regardless of the loan type or country.

Frequently Asked Questions About Mortgage Approval

FAQ | Your Quick Answers to Common Home Loan Queries

What is the ideal CIBIL score for a home loan in India?

While there’s no official minimum, most Indian banks prefer a CIBIL score of 750 or higher. A score below 700 might make approval difficult or lead to less favorable terms.

How much down payment do I need for a home loan in India?

Generally, banks in India finance 75-90% of the property value. This means you’ll need to arrange for 10-25% of the property cost as a down payment from your own funds.

Can I get a home loan with no income proof?

It’s extremely challenging. Banks require stable income proof (salary slips, ITRs, bank statements) to assess your repayment capacity. Without it, securing a traditional home loan is nearly impossible.

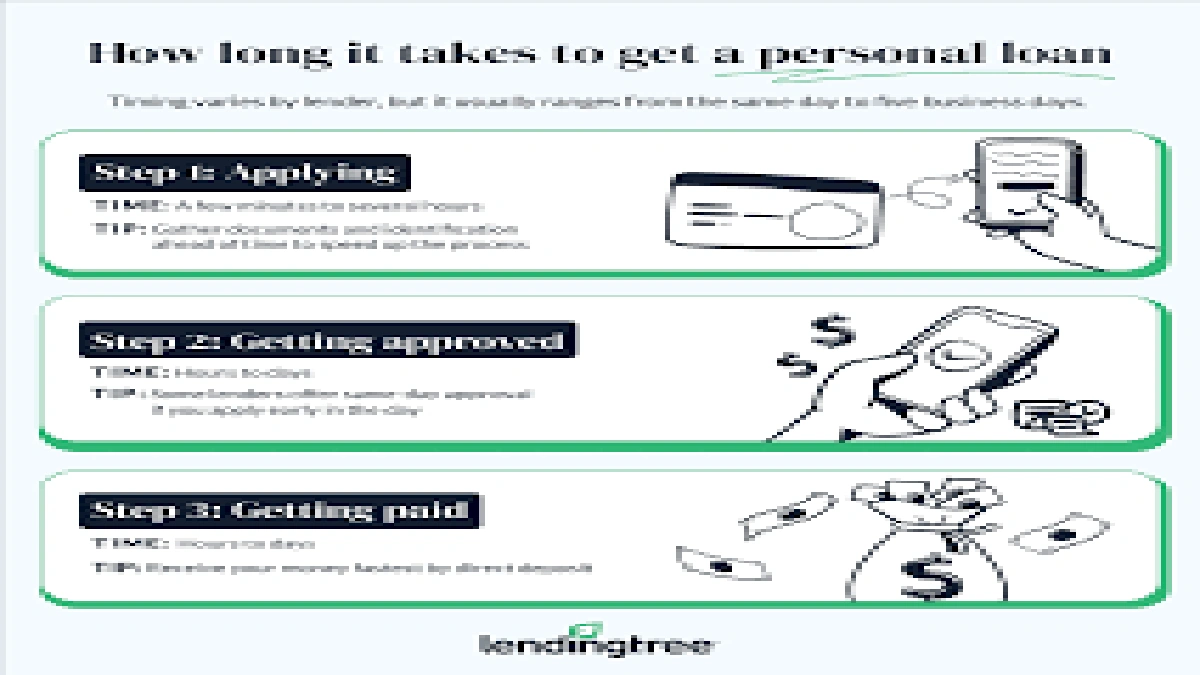

How long does it typically take to get a home loan approved?

If all your documents are in order and your financial profile is strong, approval can take anywhere from 10 days to 3 weeks. However, delays due to incomplete paperwork or property verification issues can extend this to over a month.

What is a pre-approved home loan, and how does it help?

A pre-approved home loan is a conditional offer from a bank stating the maximum loan amount you’re eligible for. It helps you know your budget, strengthens your negotiation power with sellers, and significantly speeds up the final loan disbursal process once you’ve chosen a property.

Should I apply to multiple banks for a home loan?

While it’s good to compare offers, applying to too many banks simultaneously can negatively impact your CIBIL score due to multiple hard inquiries. It’s better to get pre-approvals from 1-2 preferred banks and then proceed with one.

The Final Word | Your Home Loan Journey Starts Now

Getting your mortgage approved fast isn’t about shortcuts; it’s about being prepared, strategic, and proactive. It’s about understanding the lender’s perspective and presenting yourself as the most reliable borrower they could ask for. From meticulously managing your CIBIL score and debt-to-income ratio to having your documents perfectly organized and even securing a pre-approval, every step you take brings you closer to that moment when the bank says, “Yes.” This isn’t just about tips; it’s about empowerment. So, take these insights, apply them diligently, and get ready to unlock the doors to your dream home.