Ever felt that little knot of confusion when banks talk about ‘secured’ and ‘unsecured’ loans? You’re not alone. It’s like standing at a crossroads, knowing you need a loan, but unsure which path leads to your best financial future. Here’s the thing: understanding the core differences between a secured personal loan and an unsecured personal loan isn’t just about jargon; it’s about making a smart decision that impacts your wallet, your peace of mind, and your future borrowing power. As someone who’s seen countless individuals navigate these waters, I can tell you, the ‘how’ of choosing is far more important than just knowing the ‘what’. Let’s break it down, simple and clear, so you can walk away feeling confident.

Demystifying the Basics | What’s the Real Difference?

At its heart, the distinction is about risk – specifically, whose risk it is. Think of it like this:

The Secured Personal Loan: Your Assets on the Line (But for a Good Reason)

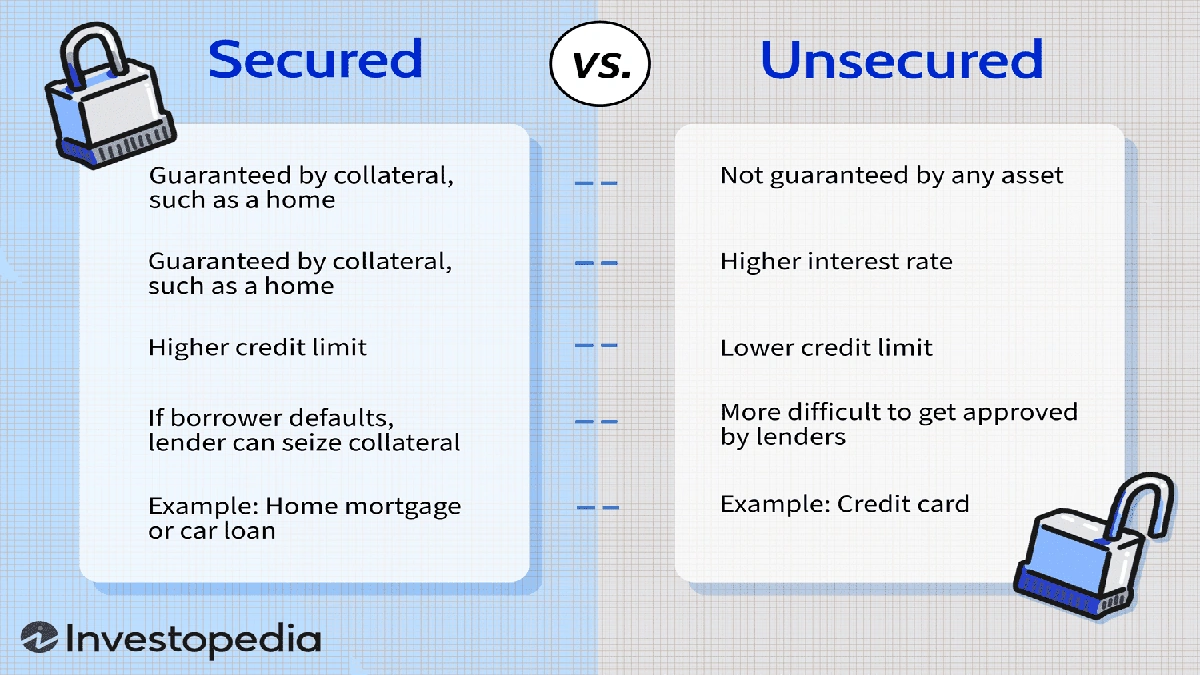

When you opt for a secured personal loan , you’re essentially offering something valuable you own as ‘collateral’. This could be your car, your house (like amortgage loan, for example), gold, or even fixed deposits. The bank, seeing this collateral, views you as a lower risk. Why? Because if for some reason you can’t repay the loan, they have a claim on your asset to recover their money. This reduced risk for the lender often translates to benefits for you:

- Lower Interest Rates: Generally, you’ll find the interest rates personal loan for secured options are more attractive.

- Higher Loan Amounts: Lenders are often willing to offer larger sums.

- Longer Repayment Terms: You might get more flexible loan repayment terms.

- Potentially Easier Approval: Especially if your credit score isn’t stellar, the collateral can be a big help.

The catch? If you default, you risk losing that asset. It’s a significant commitment, and you need to be sure you can honor the loan tenure .

The Unsecured Personal Loan: Freedom, But at a Price

Now, an unsecured personal loan is the more common type you hear about. Here, there’s no collateral for personal loan involved. Your eligibility hinges entirely on your financial standing – your income, employment stability, and most importantly, your credit score . This is why lenders assess your creditworthiness so stringently. Because there’s no asset backing the loan, the bank takes on more risk. And more risk for them usually means:

- Higher Interest Rates: To compensate for the added risk, interest rates are typically higher than secured loans.

- Stricter Eligibility Criteria Personal Loan: A good credit history is paramount.

- Lower Loan Amounts: Generally, the maximum amount you can borrow is less compared to secured options.

- Quicker Approval: Often, these loans are processed faster since there’s no collateral to evaluate.

The upside? No asset is at risk. This makes it a popular choice for immediate needs like medical emergencies, wedding expenses, or fundingtuition fees.

The ‘How’ of Choosing | Factors That Truly Matter

So, how do you decide between a secured personal loan and a loan without collateral ? It’s not a one-size-fits-all answer. It’s about aligning the loan with your specific needs and financial situation. Let me walk you through the key considerations:

1. Your Need for Funds & Purpose of the Loan

Are you looking for a small amount to cover an unexpected expense, or a substantial sum for a major investment? If it’s a smaller, urgent need (say, under ₹5-10 lakhs), an unsecured personal loan might be ideal due to its quick disbursal. For larger aspirations, like home renovations or business expansion, where you might need ₹20 lakhs or more, a secured loan often makes more sense due to lower interest rates and longer loan repayment terms .

2. Your Credit Score & History

This is probably the most critical factor for an unsecured personal loan . A highcredit score(typically 750+) signals to lenders that you’re a responsible borrower, opening doors to better rates and higher limits. If your score is on the lower side, or you’re just starting your credit journey, getting a secured personal loan might be your only viable option, as the collateral mitigates the risk associated with your credit history. The credit score impact personal loan approval and its terms cannot be overstated.

3. Availability of Collateral

Do you have an asset you’re comfortable pledging? Gold, property, fixed deposits, even certain investments can serve as collateral. If you have these assets lying dormant, a secured personal loan can unlock their value at a lower cost. If you prefer not to risk your assets, or simply don’t have suitable collateral, then an unsecured personal loan is your path.

4. Interest Rates and Overall Cost

While an unsecured personal loan offers convenience, that convenience comes at a higher price in the form of elevated interest rates personal loan . Over a long loan tenure , even a percentage point difference can amount to significant savings. Always calculate the total cost of the loan – including processing fees, prepayment charges, and interest – before making a decision. Sometimes, the peace of mind of not risking an asset is worth the extra interest, but sometimes it isn’t.

When to Go Secured | The Strategic Borrower’s Playbook

I’ve seen many people smartly leverage secured loans. Here are scenarios where this option truly shines:

- Large Funding Needs: If you need a substantial amount, say for a child’s higher education abroad or a major medical procedure, a secured personal loan can provide the necessary capital at a much more manageable interest rate.

- Building Credit (or Rebuilding It): If your credit score needs a boost, or you have a limited credit history, a secured loan can be a stepping stone. Showing responsible repayment on a secured loan can positively impact your credit profile.

- Accessing Lower Interest Rates: When every rupee saved matters, and you have valuable assets, pledging them can get you the most competitive interest rates personal loan, significantly reducing your overall cost of borrowing. This is crucial for long-term financial planning.

- Longer Repayment Periods: If you require a longer period to comfortably repay your loan without straining your monthly budget, secured loans often offer more extended loan repayment terms.

When to Go Unsecured | The Need for Speed & Simplicity

Conversely, unsecured personal loans are fantastic for different situations:

- Emergencies and Immediate Needs: When time is of the essence – a sudden medical bill, a car repair, or an unexpected travel expense – the swift approval and disbursal of an unsecured personal loan can be a lifesaver. You can often find some of the best personal loan India options for quick access.

- No Collateral Available or Desired: If you don’t own assets you can pledge, or simply don’t want the risk of losing them, an unsecured personal loan offers the flexibility of borrowing without putting your property on the line.

- Smaller Loan Amounts: For amounts under ₹10-15 lakhs, where the difference in interest rates might not be as impactful over a shorter loan tenure, the convenience often outweighs the slightly higher cost.

- Excellent Credit History: If you have an impeccable credit score, you might qualify for competitive interest rates personal loan even on unsecured options, making them a very attractive choice.

The Hidden Costs and What to Watch Out For

Beyond interest rates, there are other costs and considerations in any personal loan comparison :

- Processing Fees: Most banks charge a one-time fee to process your loan application. This usually ranges from 0.5% to 2.5% of the loan amount.

- Prepayment/Foreclosure Charges: If you decide to pay off your loan early, some lenders might charge a penalty. Always check this beforehand, especially if you anticipate having extra funds later.

- Late Payment Penalties: Missing an EMI can lead to significant late fees and a negative impact on your credit score.

- Impact on Credit Score: While timely repayments boost your score, defaulting on either a secured personal loan or an unsecured personal loan will severely damage it, affecting future borrowing.

Choosing between a secured personal loan and an unsecured personal loan isn’t just about what banks offer; it’s about what you need, what you can afford, and what level of risk you’re comfortable with. Don’t rush into a decision. Take the time to evaluate your financial health, consider the purpose of the loan, and compare offers from multiple lenders. Your future self will thank you for making an informed financial decision . Remember, the best loan is the one that fits your life, not just your immediate need.

Your Burning Questions About Personal Loans, Answered!

Can I get an unsecured personal loan with a low credit score?

It’s challenging, but not impossible. Lenders might offer smaller amounts at higher interest rates personal loan , or require a co-applicant with a good credit score. However, a secured personal loan might be a more accessible option in this scenario.

What kind of collateral is accepted for a secured personal loan?

Common types of collateral for personal loan include property (residential or commercial), gold, fixed deposits, shares, and sometimes even vehicles. The value of the collateral directly influences the loan amount you can get.

Are interest rates fixed or floating for these loans?

Both secured and unsecured personal loans in India can come with either fixed or floating interest rates . Fixed rates remain constant throughout the loan tenure , offering predictability. Floating rates fluctuate with market conditions, potentially leading to lower or higher payments over time. Always clarify this with your lender during your personal loan comparison .

How quickly can I get an unsecured personal loan?

Often, unsecured personal loans can be approved and disbursed within 24-72 hours, especially if you have a strong credit profile and all your documents are in order. Some digital lenders even offer instant approvals.

What if I can’t repay my secured personal loan?

If you default on a secured personal loan , the lender has the legal right to seize and sell the collateral you pledged to recover their dues. This is why it’s crucial to assess your repayment capacity thoroughly before opting for such a loan and understand the full implications of your borrowing options .