Alright, let’s grab a cuppa and talk about something that’s probably been buzzing in your head if you own a home in the UK: your mortgage. Specifically, those ever-shifting mortgage refinance rates UK today . It’s not just about a number on a screen; it’s about your financial future, your peace of mind, and frankly, a significant chunk of your monthly budget. And trust me, what’s happening right now in the UK mortgage market isn’t just news; it’s a pivotal moment demanding a deeper look.

I get it. The world of mortgages can feel like a labyrinth, especially with headlines screaming about inflation, interest rates, and the general cost of living crisis. You might be wondering: Is it time to remortgage? Am I missing out on a better deal? Or perhaps, should I just ride it out? Here’s the thing: understanding the ‘why’ behind these rates is far more powerful than just knowing the ‘what’. Let’s peel back the layers and see what’s really going on.

What’s Really Driving UK Mortgage Rates Right Now?

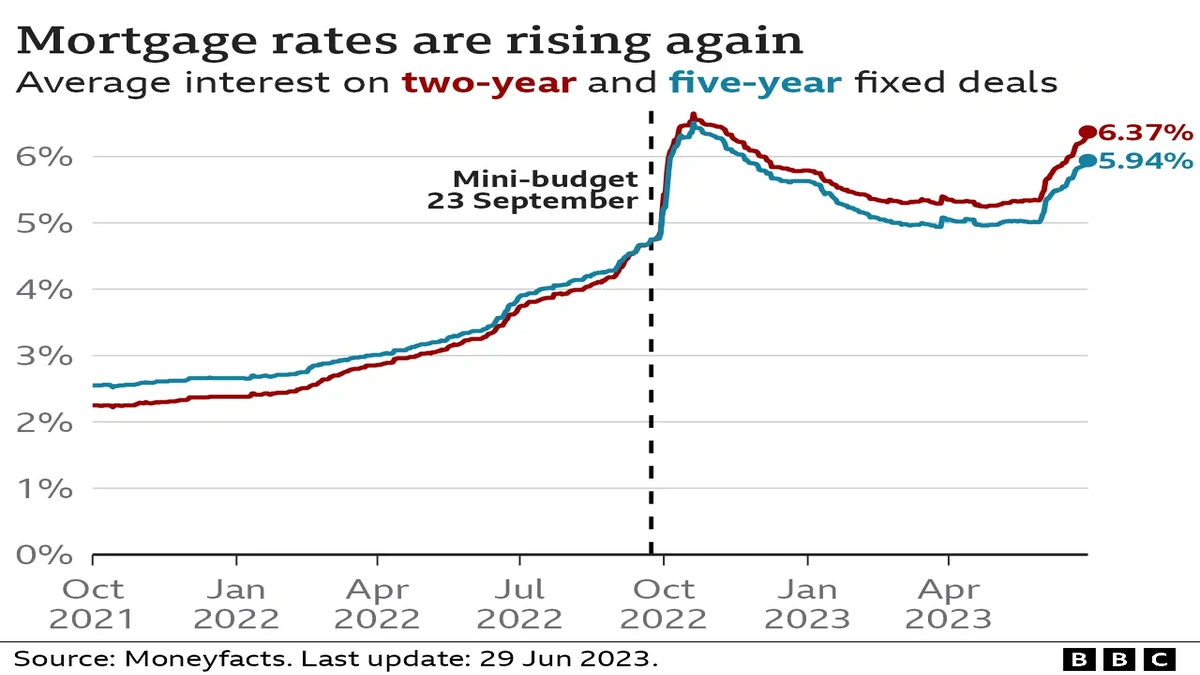

To truly grasp the current landscape of mortgage refinance rates UK today , we need to talk about the big elephant in the room: the Bank of England. The BoE’s Monetary Policy Committee (MPC) sets the base rate, and that rate is the bedrock upon which almost all other lending rates, including mortgages, are built. When the BoE raises or lowers its base rate, lenders react, often quite quickly.

But it’s not just the BoE. Inflation, that relentless upward march of prices, plays a huge role. The BoE’s primary mandate is to keep inflation at 2%. When inflation soars, as it has done recently, the bank’s main weapon is to hike interest rates to cool down the economy. This, in turn, makes borrowing more expensive across the board. So, when you see a shift in your potential remortgaging rate, it’s often a direct ripple effect from these macroeconomic forces. The UK mortgage market outlook is intrinsically linked to these broader economic indicators. It’s a complex dance between global energy prices, supply chain issues, and consumer spending habits, all influencing the BoE’s decisions.

What fascinates me is how quickly sentiment can shift. A few months ago, predictions for rate cuts were everywhere. Now? It’s a more cautious tone, with analysts closely watching wage growth and service inflation. This uncertainty is why staying informed about the Bank of England interest rate impact is absolutely critical for anyone considering their mortgage options.

Fixed vs. Variable | Why Your Choice Matters More Than Ever

So, you’re looking at your options. Should you go for a fixed-rate mortgage or a variable-rate mortgage ? This isn’t just a preference; it’s a strategic decision that could save or cost you thousands, especially in today’s volatile environment.

Fixed-rate mortgage deals UK offer stability. You lock in an interest rate for a set period – usually 2, 3, or 5 years. This means your monthly payments remain predictable, no matter what the Bank of England does. For many, especially those grappling with the cost of living crisis UK mortgage pressures, this certainty is invaluable. A common mistake I see people make is waiting too long, hoping for rates to drop further, only to see them tick up again. If stability is your priority, and you find a rate you’re comfortable with, sometimes securing it is the best move.

On the flip side, variable-rate mortgage pros and cons are all about flexibility and risk. Your interest rate can go up or down, tracking the BoE’s base rate. If rates fall, you benefit. If they rise, so do your payments. This option is often favored by those who believe rates will fall in the near future or those who have significant savings to absorb potential payment hikes. But let’s be honest, that’s a gamble. My experience tells me that while the allure of lower payments if rates drop is tempting, the stress of potential increases often outweighs it for most homeowners. It’s about understanding your personal risk tolerance and financial resilience.

The Hidden Costs and Opportunities of Remortgaging

When you start thinking about remortgaging , it’s easy to get fixated solely on the interest rate. But that’s just one piece of the puzzle. The entire remortgaging process UK involves several other factors that can significantly impact the true cost or benefit.

First, there are fees. Arrangement fees, valuation fees, legal fees – these can quickly add up. Some of the best refinance rates might come with hefty fees, making a slightly higher rate with lower fees a better overall deal. Always ask for the ‘total cost of credit’ or compare the Annual Percentage Rate of Charge (APRC) to get a clearer picture. Don’t forget, if you’re still within an existing fixed-rate period, you might face early repayment charges, which can be substantial. This is where an expert’s eye really helps, as they can weigh these charges against the savings from a new rate.

Secondly, consider the equity in your home. With recent property value trends UK , many homeowners might find they have more equity than they think. This can open doors to better loan-to-value (LTV) ratios, potentially unlocking even better mortgage deals. Or, if you’re looking to consolidate other debts or fund home improvements, a remortgage can sometimes be a more cost-effective way to release equity, much like how some might considergold collateral for quick funds, though a mortgage is a far more substantial financial instrument.

Trustworthiness in this process comes from being transparent about all potential costs and benefits. While sources might suggest certain trends, always get a personalized quote and breakdown from a reputable advisor. It’s your money, after all.

Navigating the Current Housing Market | A Pro’s Perspective

Beyond your personal mortgage, it’s crucial to consider the broader housing market UK . What’s happening with house prices, supply, and demand can subtly influence lender appetites and, by extension, the availability and competitiveness of mortgage refinance rates UK today .

We’ve seen periods of incredible growth, followed by plateaus and even slight dips in certain regions. The current mortgage market forecast UK suggests a period of stabilization, but with regional variations. Factors like affordability, employment rates, and even government housing policies all play a part. For someone looking to climb theproperty ladder or even just stay put, understanding these macro trends provides invaluable context.

My advice? Don’t get swept up in the hype or the doom and gloom. Focus on your personal circumstances. Is your job secure? Do you have an emergency fund? What are your long-term financial goals? The ‘best’ time to remortgage isn’t a universal date on the calendar; it’s when it aligns with your financial strategy and offers you the most security or saving.

Frequently Asked Questions About UK Mortgage Refinance Rates

What’s the difference between remortgaging and product transfer?

Remortgaging involves switching your mortgage to a completely new lender, often to get a better deal or release equity. A product transfer, on the other hand, means staying with your current lender but moving to a different mortgage product (e.g., from a fixed to a variable rate) they offer. Product transfers are often quicker and involve less paperwork, but may not always offer the absolute best rates available across the whole market.

How far in advance should I start looking at remortgage rates?

It’s generally recommended to start looking at least 3 to 6 months before your current deal ends. Many lenders will allow you to lock in a new rate up to 6 months in advance, giving you peace of mind. If rates drop significantly before your deal starts, you might even be able to switch to a better one.

Will my credit score affect my ability to remortgage?

Absolutely. Your credit score is a crucial factor. Lenders use it to assess your reliability as a borrower. A strong credit score can open access to the best refinance rates , while a poor one might limit your options or result in higher interest rates. It’s wise to check your credit report well in advance and address any inaccuracies.

What documents do I need for remortgaging?

Typically, you’ll need proof of identity and address, bank statements, payslips or proof of income, details of your current mortgage, and potentially information about any other debts or financial commitments. Having these ready can significantly speed up the remortgaging process UK .

Is it always better to get the lowest advertised interest rate?

Not necessarily. As discussed, the lowest interest rate might come with high arrangement fees or other charges that make the overall cost more expensive. Always look at the total cost over the term of the mortgage deal, including all fees, to determine the true value. Sometimes a slightly higher rate with no fees is the more economical choice.

Wrapping It Up | Your Next Steps

Navigating mortgage refinance rates UK today is less about predicting the future and more about making informed decisions based on the present. The market is dynamic, influenced by everything from global economics to the Bank of England’s latest pronouncements. But by understanding the ‘why’ behind these movements, by weighing the pros and cons of fixed versus variable, and by looking beyond just the headline rate, you empower yourself.

Don’t let the complexity paralyze you. Take the time to assess your situation, perhaps chat with an independent financial advisor who can help you sift through the myriad of mortgage deals . Because in this intricate dance of finance, knowledge isn’t just power; it’s peace of mind.