Alright, let’s grab a cuppa and talk about something that’s probably been nagging at the back of your mind: mortgage rates UK prediction next 6 months . It’s a question that keeps homeowners and hopeful first-time buyers alike glued to financial news, often with a mix of anxiety and cautious optimism. And honestly? It’s easy to get lost in the jargon and conflicting headlines. What I want to do today is cut through the noise, give you an analyst’s perspective, and explain why these predictions matter, beyond just the numbers on a screen.

Here’s the thing about the UK housing market and its mortgages: it’s less about a crystal ball and more about understanding the complex dance between inflation, the Bank of England, and global economic ripples. We’re not just reporting what might happen; we’re diving into the underlying forces that shape your repayments, your ability to buy, and ultimately, your financial peace of mind. Let’s unpick this together, shall we?

The Big Picture | Why the Bank of England Holds the Key

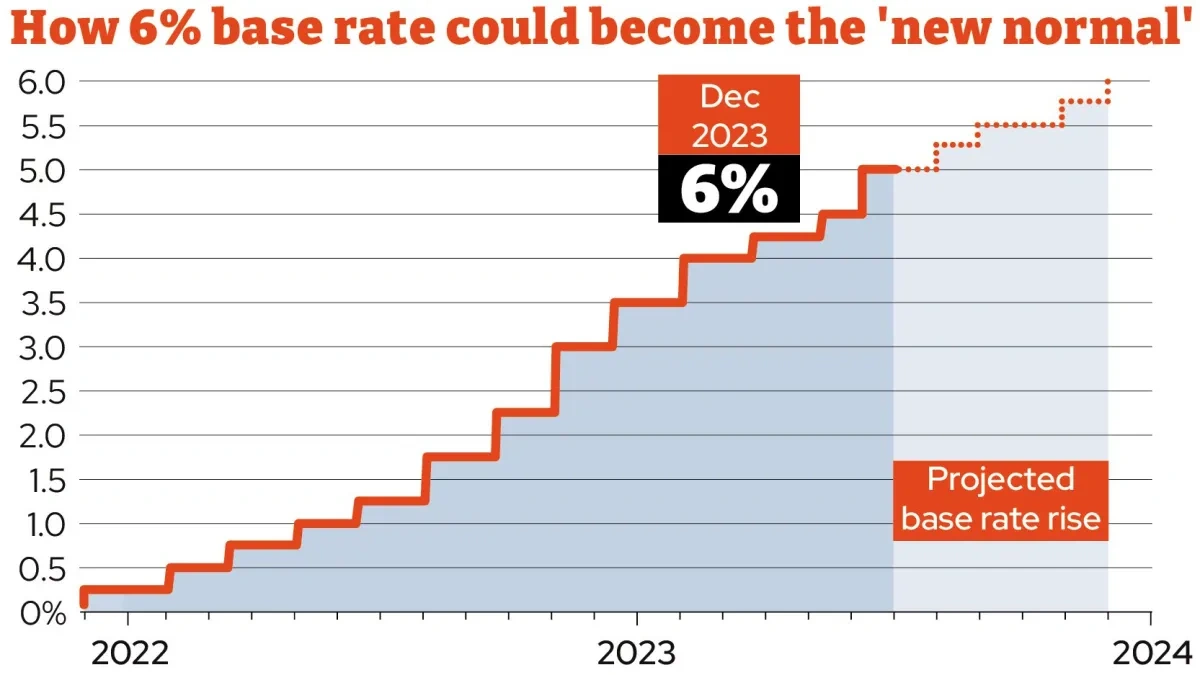

When we talk about mortgage rates UK , the first entity you need to understand is the Bank of England . Think of them as the maestro of the UK economy’s orchestra. Their Monetary Policy Committee (MPC) sets the official Bank Rate, and this single decision sends ripples throughout the entire financial system. Why? Because commercial lenders the banks and building societies offering you mortgages use the Bank Rate as a benchmark for their own lending rates. If the Bank Rate goes up, so do their costs, and they pass that on to you.

What drives the BoE’s decisions? Inflation, pure and simple. Their primary mandate is to keep inflation at 2%. When inflation runs hot, as it has been, the Bank’s go-to move is to hike interest rates to cool the economy down. This makes borrowing more expensive, which ideally reduces spending and brings prices back under control. But it’s a tightrope walk – too many hikes, and you risk tipping the economy into recession. What’s truly fascinating is how this delicate balance impacts the everyday finances of millions. The current `UK mortgage market outlook` is inextricably tied to this battle against rising prices. We’ve seen a period of aggressive rate rises, but are we at the peak? That’s the million-dollar question.

Decoding the Crystal Ball | What Analysts Are Whispering

So, what’s the general interest rate forecast for the next six months? Let me be clear: nobody has a perfect crystal ball, and anyone claiming absolute certainty is selling you something. However, we can look at prevailing economic data and market consensus to form a highly informed view. Many analysts, especially after the recent slowdown in inflation, are starting to lean towards a period of stability, with potential for modest cuts in the latter half of 2024 or early 2025. This isn’t a guarantee of falling `Bank of England interest rates` immediately, but it signals a shift from the relentless upward trajectory we’ve witnessed.

Several factors contribute to this sentiment. First, inflation is easing, albeit slowly. Secondly, the economy isn’t exactly roaring; there’s a delicate balance to strike. And finally, global economic conditions, particularly in the US and Europe, also play a role. If major central banks elsewhere signal cuts, it gives the BoE more room to manoeuvre without weakening sterling too much. For anyone contemplating a move or a remortgage , this nuance is critical. A significant `housing market forecast UK` suggests that while house price growth has been subdued, a more stable, or even slightly declining, interest rate environment could bring a much-needed boost in confidence. But remember, “modest cuts” often means small, incremental steps, not a sudden plunge back to ultra-low rates.

Fixed vs. Variable | Navigating Your Options

This is where things get really personal. If you’re currently on a variable-rate mortgage or your fixed-rate mortgages deal is coming to an end, the choice between fixing and staying variable is paramount. For a long time, fixed rates offered certainty in an uncertain world, albeit at higher prices. Now, with the expectation of rates potentially stabilising or even slightly falling, the appeal of a shorter fix or even a tracker (variable) mortgage is returning for some.

Understanding `fixed vs variable mortgages UK` is more than just picking a number; it’s about your personal risk appetite and financial stability. A fixed rate offers predictability in your monthly payments, insulating you from any unexpected hikes, but you might miss out if rates fall further. A variable rate, conversely, means your payments could decrease if the Bank Rate drops, but they could also increase if things take an unexpected turn. My personal take? It really depends on your circumstances. If you value budgeting certainty above all else, a fix, even for a shorter term, might still be prudent. If you have a larger financial cushion and are comfortable with some volatility, a variable product might offer more flexibility. This is where getting bespoke `remortgaging advice UK` becomes invaluable, as what’s right for one person isn’t for another.

Beyond the Headlines | What This Means for You (The “Why” Angle)

So, what do these mortgage rates UK prediction next 6 months really mean for your life? It’s not just about percentages; it’s about financial planning, peace of mind, and the ability to achieve your long-term goals.

- For Homeowners Due to Remortgage: Don’t wait until the last minute. Start talking to a mortgage advisor 6-9 months before your current deal ends. They can lock in rates for you in advance, sometimes for a period of up to six months. This strategy gives you a safety net if rates rise further but also allows you to switch to a better deal if rates fall before your completion. Being proactive, much like understanding all the terms for a used car loan, ensures you don’t get caught off guard by unexpected shifts in the market.

- For First-Time Buyers: The landscape might be less daunting than it was a year ago, but affordability remains a challenge. The potential for stable or slightly lower rates could ease the burden somewhat, but don’t expect a return to the historic lows. Focus on building a strong deposit, improving your credit score, and understanding all the schemes available for `first-time buyer UK mortgage` applicants. It’s a marathon, not a sprint, and every bit of preparation helps.

- Managing the `Cost of Living UK Impact on Mortgages`: Even if rates stabilise, the broader cost of living crisis continues to bite. This means budgeting is more critical than ever. Review your household spending, look for areas to save, and build an emergency fund. This financial resilience will serve you well, regardless of rate movements. Think of it as holistic financial health; being mindful of your overall debt, whether it’s your mortgage or even just knowing about car loan interest rates in the USA, is part of managing your financial ecosystem.

The truth is, even a small shift in the economic outlook can have a tangible impact on your monthly budget. That’s why understanding the ‘why’ behind the numbers empowers you to make smarter, more informed decisions. It’s about taking control, not just reacting to headlines.

Preparing for the Future | Practical Steps Now

In this dynamic environment, preparation is your superpower. Here are some actionable steps you can take today:

- Consult a Mortgage Advisor (Independent is Best): They have access to a wider range of products and can offer impartial `remortgaging advice UK` tailored to your specific situation. This isn’t a sales pitch; it’s genuinely the best way to navigate complex financial products.

- Review Your Credit Score: A good credit score is crucial for securing the best mortgage rates UK. Check it regularly with services like Experian, Equifax, or TransUnion. Identify any errors and work to improve it.

- Stress Test Your Finances: Can you comfortably afford your mortgage if rates were to tick up by another 0.5% or 1%? Understanding your tolerance for risk helps you choose the right product.

- Research, Research, Research: Keep an eye on official sources. The Bank of England’s website provides updates on interest rates and economic commentary, which can be invaluable. For broader economic data, the Office for National Statistics is your friend.

Frequently Asked Questions About UK Mortgage Rates

Will UK mortgage rates definitely fall in the next 6 months?

While many analysts anticipate potential cuts later in 2024, there’s no guarantee. The exact timing and extent of any changes depend heavily on inflation data and the broader economic outlook . It’s more likely we’ll see stability, with perhaps marginal downward shifts, rather than a significant drop.

What’s the main factor influencing mortgage rates UK?

The primary driver is the Bank of England ’s official Bank Rate, which they adjust to control inflation. Secondary factors include lender competition, the cost of funds in wholesale money markets, and broader economic sentiment.

Should I fix my mortgage now or wait?

This is a personal decision based on your risk appetite. If you value payment certainty and peace of mind, a fixed-rate mortgages deal might be preferable. If you have a higher risk tolerance and believe rates will fall significantly, a variable product might be considered. Consulting an independent advisor is highly recommended.

How does the cost of living affect my ability to get a mortgage?

The `cost of living UK impact on mortgages` is significant. Lenders assess your affordability based on your income versus your outgoings. Higher everyday expenses mean less disposable income, which can reduce the amount you’re eligible to borrow or make meeting stress tests harder. This is particularly relevant for `first-time buyer UK mortgage` applications.

Where can I get personalized remortgaging advice UK?

For tailored advice, your best bet is to speak with an independent mortgage broker. They can assess your individual financial situation, discuss various remortgage options , and recommend products from across the market that suit your needs.

Ultimately, navigating the world of mortgage rates UK prediction next 6 months isn’t about fortune-telling. It’s about empowering yourself with knowledge, understanding the ‘why’ behind the numbers, and taking proactive steps to protect your financial future. The market will always have its ups and downs, but with a solid strategy and reliable advice, you can approach the next six months – and beyond – with far greater confidence. Stay informed, stay proactive, and remember that your financial well-being is the most important forecast of all.