Dreaming of owning a home in the USA? It’s a powerful aspiration, especially for those of us watching from afar or navigating the complex financial landscape for the first time. But let’s be honest, the idea of buying your first home can feel like trying to solve a Rubik’s Cube blindfolded. Mortgages, down payments, closing costs – it’s a lot! And then you hear whispers of “grants” for first time home buyer grants USA 2026, and a little spark of hope ignites. But what are these grants, really? Are they truly free money? And more importantly, how do YOU get your hands on them?

Here’s the thing: while the term ‘grants’ conjures images of endless free cash, the reality is a bit more nuanced. My goal today isn’t just to tell you what’s available, but to be your personal guide, helping you understand the landscape of first time home buyer grants USA 2026 and how to navigate it like a pro. We’re going to peel back the layers, step-by-step, so you can transform that homeownership dream into a tangible plan.

Demystifying “Grants” | What Are We Really Talking About?

When people talk about first time home buyer grants USA 2026, they’re often referring to a broader category of financial assistance designed to make homeownership more accessible. It’s not always a straightforward check handed to you. Instead, it encompasses several types of aid:

- True Grants: These are the closest to “free money.” They don’t need to be repaid, provided you meet specific conditions, like living in the home for a certain number of years. They’re often tied to specific local or state initiatives.

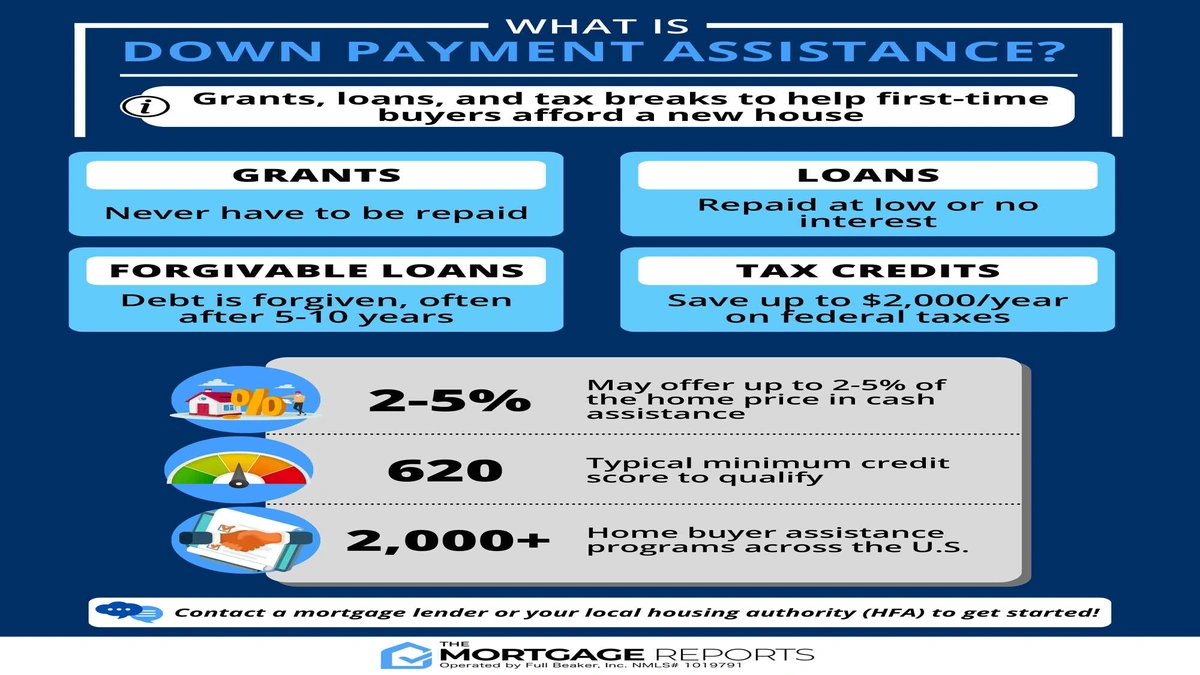

- Down Payment Assistance Programs: This is arguably the most common form of help. These programs offer funds to cover your down payment, often as a second mortgage with a very low interest rate, or even forgivable loans that disappear after a set period. Many people confuse these with outright grants, and while they function similarly for the initial purchase, the repayment structure can differ.

- Closing Cost Assistance: Beyond the down payment, closing costs can be a significant hurdle, sometimes 2-5% of the loan amount. Many programs specifically target these fees, helping you reduce your out-of-pocket expenses.

- First Mortgage Subsidies: Sometimes, the assistance comes in the form of a lower-than-market interest rate on your primary mortgage, making your monthly payments more affordable.

Understanding this distinction is crucial. It’s not just about finding any grant; it’s about finding the right type of down payment assistance programs that align with your financial situation and long-term goals. The hidden context here is that many programs are structured to incentivize long-term homeownership and community stability, not just to give away money.

The Big Players | Federal Programs to Watch in 2026

While direct federal grants for individuals are rare, several federal programs act as powerful enablers for first time home buyer grants USA 2026 by making mortgages more accessible and affordable. Think of them as the foundational layers upon which state and local programs build.

1. FHA Loans | A First-Timer’s Best Friend

The Federal Housing Administration (FHA) doesn’t give you grant money directly, but it insures loans made by private lenders. This insurance protects lenders, making them more willing to offer mortgages to borrowers with lower credit scores and smaller down payments. For many first time home buyer grants USA 2026 hopefuls, FHA loans are a game-changer because they require as little as 3.5% down, significantly less than conventional loans. This lower barrier to entry effectively frees up more of your savings, which could then be combined with other down payment assistance programs.

2. VA Loans | A Huge Benefit for Service Members

If you’re a veteran, active-duty service member, or eligible surviving spouse, VA loans are arguably the best mortgage program available. Backed by the U.S. Department of Veterans Affairs, these loans often require no down payment at all and typically come with competitive interest rates. This means you could potentially achieve homeownership dreams with zero money down, a massive form of assistance in itself. You can learn more about these invaluable benefits on the officialU.S. Department of Veterans Affairs website.

3. USDA Loans | Rural Opportunities

The U.S. Department of Agriculture (USDA) offers loans to help low- and moderate-income individuals purchase homes in eligible rural areas. Like VA loans, many USDA programs require no down payment, making them incredibly attractive. The catch, of course, is that the property must be in a designated rural area, which might surprise you as some areas are quite close to urban centers. If you’re looking outside the bustling cities, a USDA loan could be your ticket to affordable homeownership.

These federal housing programs aren’t grants in the traditional sense, but they are crucial components that reduce the financial burden, making it easier to qualify for a mortgage and potentially combine with other forms of assistance.

State-Specific Goldmines | Your Local Advantage

This is where the real magic happens for many first time home buyer grants USA 2026 seekers. Every state, and often many cities and counties, have their own housing finance agencies (HFAs) that offer a plethora of programs specifically designed for first-time homebuyers. These are the unsung heroes of affordable housing!

These state housing finance agencies (HFAs) often provide:

- Down Payment and Closing Cost Assistance: These are usually second mortgages that are either forgivable (you don’t repay if you stay in the home for X years) or deferred (you repay when you sell or refinance).

- First-Time Homebuyer Bonds: These programs can offer lower interest rates on your primary mortgage.

- Special Programs: Some states have programs for specific professions (e.g., teachers, first responders), specific areas, or for renovating distressed properties.

A common mistake I see people make is only looking at federal options. The truth is, your state and local HFA website should be one of your first stops! They are specifically mandated to help residents achieve homeownership. For instance, while you’re looking into home loans, it’s always good to understand the broader financial landscape, perhaps even comparing how different loan types, like agold loan interest rate today, might differ from home loan rates, giving you a holistic view of financing options.

Cracking the Code | Eligibility & Application in 2026

Now for the nitty-gritty: how do you actually qualify for these programs? While specific eligibility criteria vary wildly, some common themes emerge across most first time home buyer grants USA 2026 programs:

1. First-Time Homebuyer Definition

Generally, you’re considered a first-time homebuyer if you haven’t owned a home in the last three years. However, there are exceptions, especially for single parents, displaced homemakers, or those buying in certain targeted areas.

2. Income Limits

Most assistance programs are designed for low-to-moderate income earners. There will be specific income limits based on your household size and the area you’re buying in. It’s not about being poor, but about fitting within a defined bracket that shows you need assistance but can also afford a mortgage.

3. Credit Score Requirements

While FHA loans are more forgiving, most programs, especially those offering the best terms, will have minimum credit score requirements. Lenders want to see a history of responsible financial behavior. If your credit score isn’t where you want it to be, start working on it now. Small steps can make a big difference over time. And just like understanding your eligibility for home loans, knowing your standing for other financial products, such as performing apersonal loan eligibility check UK, can give you a good benchmark for your overall financial health.

4. Homebuyer Education

Many programs require you to complete a homebuyer education course. Don’t see this as a hurdle; see it as an invaluable tool! These courses teach you about budgeting, mortgage types, home maintenance, and the responsibilities of homeownership. It’s truly an investment in your financial literacy.

5. Property Type and Location

Some programs are restricted to certain property types (e.g., single-family homes, condos) or specific geographic areas (e.g., revitalized neighborhoods, rural zones). Always double-check these details.

My advice? Start early. Gathering documents, improving your credit, and completing education courses take time. For 2026, the groundwork you lay in 2024 and 2025 will be absolutely critical.

Beyond the Grant | Smart Strategies for First-Time Buyers

Even with first time home buyer grants USA 2026, your personal financial habits are paramount. No grant can replace solid planning. Here are some key strategies:

- Build Your Savings Aggressively: Even if a program covers your down payment, you’ll still have earnest money, inspection fees, and initial moving costs. A healthy emergency fund is non-negotiable for homeowners.

- Get Pre-Approved: This is a crucial step. A pre-approval letter from a lender shows sellers you’re a serious buyer and gives you a clear budget. It also helps you understand what kind of mortgage you qualify for before you even start house hunting.

- Work with a Knowledgeable Lender: Not all lenders specialize in grant programs. Seek out a mortgage loan officer who has extensive experience with state housing finance agencies and down payment assistance programs. They can be your best advocate in finding the right combination of aid.

- Understand the Market: Keep an eye on the housing market trends. While you can’t predict the future, understanding current conditions can help you make informed decisions.

Frequently Asked Questions About First-Time Home Buyer Grants USA 2026

Are these grants truly “free money”?

Many programs offer assistance that doesn’t need to be repaid if you meet certain conditions, like living in the home for a set number of years. Others are low-interest or forgivable loans. It’s crucial to understand the specific terms of each program you consider.

What’s the minimum credit score I need for first-time home buyer grants?

While FHA loans can accept scores as low as 580 (with a higher down payment), many grant and assistance programs prefer a credit score of 620 or higher to qualify for the best terms. It varies significantly by program.

Can I combine multiple assistance programs?

Absolutely! This is often the smartest strategy. Many state housing finance agencies programs are designed to be layered on top of federal loans like FHA or VA. A knowledgeable lender can help you stack compatible programs.

How early should I start planning for homeownership in 2026?

Start now! Seriously. Improving your credit, saving for a down payment, attending homebuyer education, and researching programs takes time. The earlier you begin, the stronger your position will be.

Do I need to use a specific lender to access these grants?

Often, yes. Many state housing finance agencies and local programs partner with a network of approved lenders. It’s vital to work with a lender who is authorized to offer the specific programs you’re interested in.

What if I don’t qualify for a grant? Are there other options?

Yes, even without a direct grant, programs like FHA loans, VA loans, and USDA loans significantly reduce barriers to entry. Additionally, some employers offer homeownership benefits, and you can always pursue conventional loans with a smaller down payment if you have good credit.

Your Homeownership Journey Starts Now

The journey to securing first time home buyer grants USA 2026 might seem daunting, but it’s entirely achievable with the right knowledge and a proactive approach. Remember, you’re not just looking for a house; you’re building a future. By understanding the nuances of federal programs, tapping into state and local assistance, and diligently preparing your finances, you can turn that elusive dream into a solid reality. Don’t wait for 2026 to arrive; start laying the foundation for your homeownership dreams today. Your future self will thank you for taking these crucial steps.