Alright, let’s grab a coffee and talk about something genuinely important for anyone dreaming of owning a home in the States: the great debate between fixed vs adjustable mortgage rates USA . It’s not just a financial decision; it’s a peek into your future financial peace of mind. And frankly, the way we often approach it is a bit… simplistic. Most articles will just list pros and cons, but here’s the thing: that misses the deeper ‘why’ behind which one really makes sense for you right now. What fascinates me is not just what these rates are, but what they signal about the broader economy and, more importantly, your personal risk tolerance.

I’ve seen countless homebuyers wrestle with this, and the truth is, it’s rarely a black-and-white choice. It’s about understanding the subtle currents of thehousing market, anticipatinginterest rate predictions, and being honest about your own financial flexibility. So, let’s peel back the layers, shall we? This isn’t just about numbers; it’s about navigating uncertainty and securing your slice of the American dream.

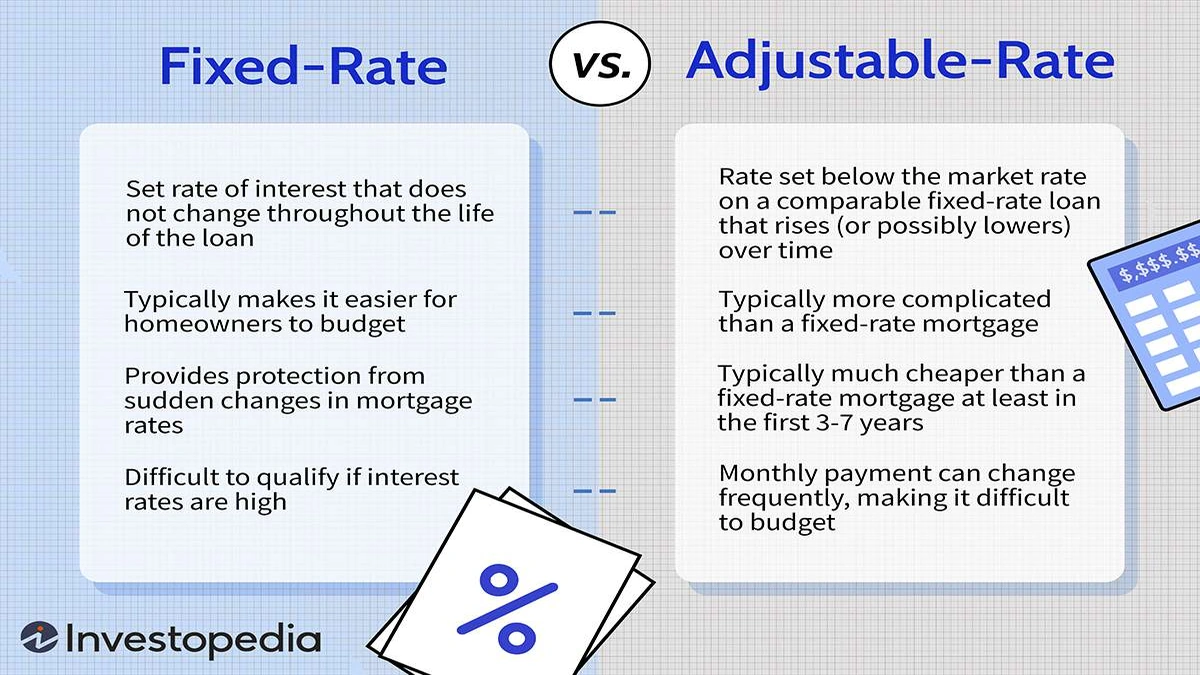

The Predictability Paradox | Why Fixed Rates Offer Peace of Mind

Picture this: you get a fixed-rate mortgage, and for the next 15, 20, or 30 years, your principal and interest payment stays exactly the same. Come rain or shine, economic boom or bust, that part of your monthly budget is locked in. For many, especially first-time homebuyers, this predictability is a huge sigh of relief. It’s the ultimate set-it-and-forget-it approach to your largest household expense. This stability is precisely why a fixed-rate mortgage is often seen as the gold standard inlong-term financial planning.

But let’s be honest, there’s a paradox here. While it offers immense peace of mind, you’re essentially paying a premium for that certainty. When mortgage rates are low, a fixed rate feels like a steal. But if rates drop significantly after you’ve locked in, you might feel a pang of regret. You could refinance, sure, but that comes with its own costs and paperwork. The main benefit, though, remains unwavering: protection from future rate hikes. It’s a powerful shield, especially in an unpredictable economic climate.

The Allure of the Unknown | Decoding Adjustable-Rate Mortgages (ARMs)

Now, let’s talk about the other side of the coin: the adjustable-rate mortgage (ARM). These loans start with an initial, often lower, fixed interest rate for a set period say, 5, 7, or 10 years. After this introductory period, your interest rates can adjust periodically based on a predetermined index, plus a margin. This is where the ‘unknown’ part comes in, and for some, it’s a thrilling prospect; for others, a source of anxiety.

Why would anyone choose an ARM? Well, the initial lower rate can make homeownership more affordable in the short term, allowing you to qualify for a larger home loan or simply save money each month. This can be a smart home loan strategy if you know you’ll be moving or refinancing before the fixed period ends. Many people use ARMs as a stepping stone. However, the risk, and it’s a significant one, is that your payments could increase sometimes substantially when the adjustment period hits. This is where financial risk management becomes crucial. While ARMs usually have caps on how much the rate can increase per adjustment period and over the life of the loan, those caps can still mean a hefty jump in your monthly outflow. It’s a gamble, albeit a calculated one, on future interest rate trends.

Beyond the Numbers | Understanding Mortgage Market Trends and Your Wallet

Choosing between fixed vs adjustable mortgage rates USA isn’t just about what’s cheaper today; it’s about what the tea leaves are telling us about the future. What are the current mortgage market trends? Are interest rates expected to rise or fall? Historically, when the Federal Reserve signals potential rate hikes to combat inflation, fixed rates tend to climb, making ARMs look more attractive initially. Conversely, in periods of economic uncertainty or when the Fed is cutting rates, fixed rates might become more appealing as they lock in a lower cost for the long haul.

This is where your personal financial outlook really comes into play. Do you anticipate a significant increase in your income in the next 5-7 years? Are you planning to sell your home within that same timeframe? Your answers here can dramatically shift the calculus. For instance, if you’re an ambitious professional expecting rapid career growth, an ARM might allow you to get into a better home now, with the expectation that you’ll either refinance or be better equipped to handle higher payments later. But if stability is your mantra, and you foresee your income remaining relatively static, the potential for payment shock with an ARM is a risk that might not be worth taking. It’s about aligning your mortgage choice with your life’s trajectory, not just the current rate sheet.

The Refinance Riddle | When to Switch and Why It Matters

One common misconception is that your mortgage choice is set in stone. Not true! Refinancing options offer a lifeline, allowing homeowners to switch from an ARM to a fixed rate, or even from a high fixed rate to a lower one. The decision to refinance is essentially a new mortgage application, complete with closing costs, but it can be a powerful tool for adapting to changing market conditions or personal financial circumstances.

For someone with an ARM, refinancing to a fixed rate before their introductory period ends (or before rates climb too high) can be a brilliant move to lock in stability. Conversely, if you have a high fixed rate and the overall mortgage rates have dropped significantly, refinancing can lead to substantial long-term savings. The key here is timing and understanding the costs involved. Don’t just jump at the lowest rate; calculate whether the savings outweigh the closing costs. It’s a strategic pivot, not a casual switch, and demands careful consideration of your financial goals and the prevailing market.

Making Your Call: A Personal Home Loan Strategy

Ultimately, the choice between fixed vs adjustable mortgage rates USA boils down to a deeply personal assessment. It’s about your comfort level with risk, your short-term and long-term financial goals, and your belief in where the economy is headed. If you value predictability above all else, a fixed-rate mortgage is likely your best friend. It’s a steadfast companion through economic ups and downs, ensuring your housing cost is a known quantity.

However, if you’re comfortable with a bit of calculated risk, anticipate a higher future income, or plan to sell/refinance within a few years, an adjustable-rate mortgage could offer a lower initial payment and potentially save you money in the short run. It’s a more dynamic choice, suited for those who are actively managing their finances and keeping an eye on interest rate predictions. There’s no single ‘right’ answer, only the answer that’s right for your unique situation. Think of it as tailoring a suit; one size doesn’t fit all, and what looks great on one person might not be the best fit for another. Your home loan strategy should reflect your life strategy.

FAQs | Unpacking Your Mortgage Questions

What is the main difference between fixed and adjustable mortgage rates?

The primary difference is how your interest rate changes over time. A fixed-rate mortgage has an interest rate that remains constant for the life of the loan, providing predictable monthly payments. An adjustable-rate mortgage (ARM) starts with a fixed introductory rate, but then adjusts periodically based on market indexes, meaning your payments can go up or down.

When is an adjustable-rate mortgage (ARM) a good idea?

An ARM might be a good idea if you plan to sell or refinance your home before the fixed-rate period ends (e.g., within 5-7 years). It can also be beneficial if you expect your income to significantly increase, making potential future rate hikes more manageable, or if current fixed rates are unusually high.

Can I switch from an ARM to a fixed-rate mortgage?

Yes, you can typically refinance an ARM into a fixed-rate mortgage. This is a common strategy to lock in a stable payment if interest rates are favorable or as your introductory fixed period on the ARM is nearing its end. Be aware of closing costs associated with refinancing.

Do adjustable-rate mortgages have limits on how much they can increase?

Yes, most adjustable-rate mortgage products include caps that limit how much the interest rate can increase (or decrease) during each adjustment period and over the entire life of the loan. These caps provide some protection against extreme payment shocks, but increases can still be substantial.

How do current economic conditions impact the choice between fixed and adjustable rates?

Current economic conditions, especially inflation and the Federal Reserve’s monetary policy, heavily influence mortgage market trends. When the Fed is raising rates, fixed rates tend to rise, potentially making ARMs with lower initial rates more attractive. Conversely, when rates are falling, fixed rates become more appealing as they lock in long-term savings.

Choosing your mortgage isn’t just signing papers; it’s signing up for a financial journey. Understanding the deeper implications of fixed vs adjustable mortgage rates USA means looking beyond the immediate numbers and truly grasping how each choice aligns with your life, your aspirations, and your tolerance for financial twists and turns. Don’t just pick a product; craft a strategy that serves your future self well. Because in the end, it’s not about the loan; it’s about the life you build within those walls.