Ever felt that sinking feeling when you look at your personal loan statement? That hefty EMI, the seemingly endless interest payments… it’s enough to make anyone wonder, “Is there any way out of this financial treadmill?” Well, my friend, you’re not alone. Many of us jump into personal loans when we need quick funds, often without fully understanding the long-term implications of a high personal loan interest rate . But here’s the good news: you’re not stuck. There are concrete, actionable steps you can take to significantly lower interest rates and lighten your financial burden.

I’ve seen countless folks navigate this maze, and let me tell you, it’s less about magic and more about strategy. Think of it as a financial chess game where you, the borrower, have more power than you might realise. My goal today isn’t just to tell you what to do, but how to do it, step-by-step, just like we’re chatting over a cup of chai. We’ll explore the hidden levers you can pull to transform your loan from a burden into a manageable part of your financial life. So, let’s dive in, shall we?

Understanding Your Current Loan | The Starting Point

Before you can fix something, you need to understand it, right? It’s like trying to navigate a city without a map. First, grab your loan documents. What’s your current personal loan interest rate ? Is it fixed or floating? What’s the remaining tenure and principal amount? Knowing these details is your first crucial step. Many people skip this, but it’s foundational. A common mistake I see? Not knowing your exact repayment history. Lenders look at this, and so should you. Have you missed any EMIs? Are there any hidden charges you overlooked?

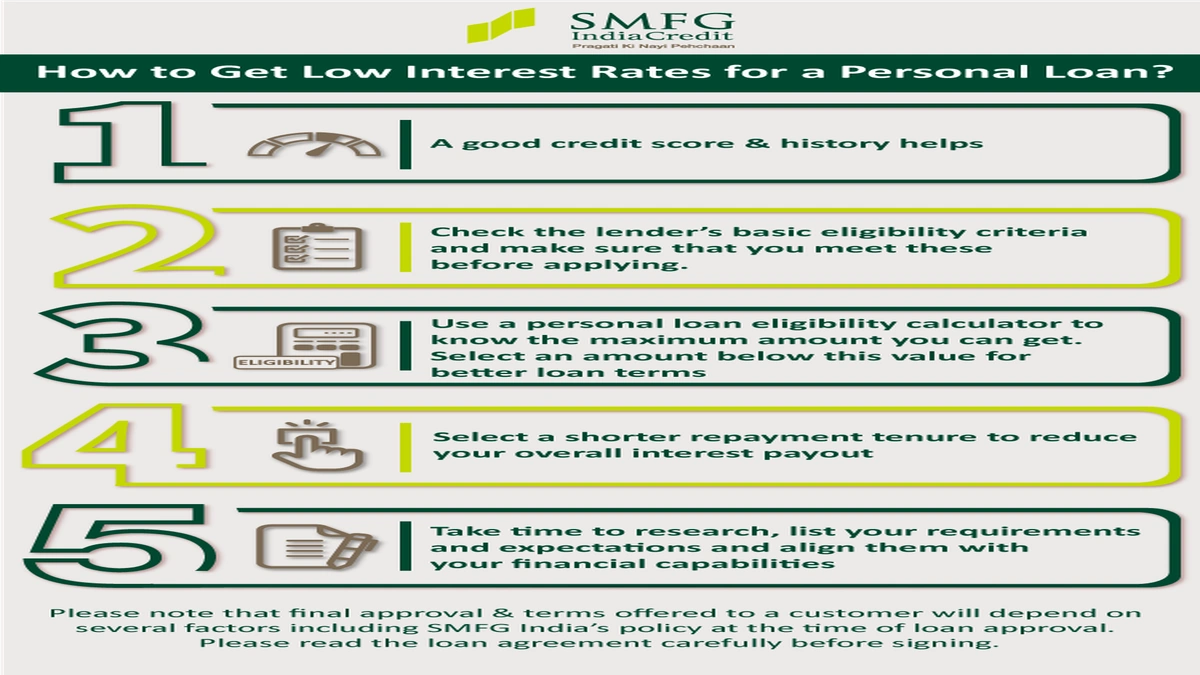

Also, take a moment to understand why your rate is what it is. Personal loan interest rates in India are largely determined by your credit score, your income stability, your relationship with the bank, and the prevailing market conditions set by the RBI. If your credit score wasn’t stellar when you took the loan, or if you were in a hurry, chances are you ended up with a higher rate. Don’t beat yourself up about it; let’s focus on moving forward.

Strategy 1 | Refinancing – A Fresh Start

This is often the most impactful move you can make. What is refinance personal loan , you ask? Simply put, it means taking out a new loan, usually from a different lender (or even your existing one), to pay off your current, more expensive personal loan. It’s like trading in an old, gas-guzzling car for a newer, more fuel-efficient model. The goal? To secure a much lower interest rate .

How to Approach Personal Loan Refinancing |

- Improve Your Credit Score (If Possible): Even a slight bump in your credit score can make a huge difference in the rates offered. Before applying for a new loan, check your credit report. Address any errors, pay off small debts, and ensure timely payments on all your existing obligations. This directly impacts your eligibility criteria for better rates.

- Shop Around Aggressively: Don’t just go with your current bank. Different lenders have different risk appetites and offers. Explore public sector banks, private banks, and even NBFCs. Compare their processing fees, prepayment penalties (more on this later), and, of course, the interest rates. Use online aggregators, but also visit bank websites directly. Sometimes, the best deals aren’t advertised everywhere.

- Negotiate with Your Current Lender: Believe it or not, your existing bank might be willing to match a competitor’s offer, especially if you have a good repayment history. They want to retain you as a customer. Approach them with a better offer from another bank and ask if they can beat or match it. It’s not guaranteed, but it costs nothing to ask, right?

- Consider a Balance Transfer: This is essentially a form of refinancing where you transfer your outstanding personal loan balance to a new lender offering a lower rate. Many banks actively promote balance transfer options for personal loans. Just be mindful of any processing fees associated with the transfer.

Refinancing can significantly reduce EMI payments and the total interest paid over the life of the loan. It’s a powerful tool, but always calculate the total cost, including any new processing fees, to ensure it’s truly beneficial. For those wondering about business financing, the principles of managing interest rates on loans can be quite similar. You might find this article ononline business loan approval timeinteresting, as quick approvals often come with their own rate considerations.

Strategy 2 | Improving Your Financial Profile

This isn’t an overnight fix, but it’s a long-term game-changer that gives you immense power over your financial future, including securing lower rates on future loans. Your financial profile is essentially your report card to lenders.

The Pillars of a Strong Financial Profile |

- Boost Your Credit Score: I can’t stress this enough. Your CIBIL score (or other credit scores like Experian, Equifax) is king. A score above 750 is generally considered excellent and opens doors to the best rates. How to improve it?

- Pay all your EMIs and credit card bills on time, every time.

- Keep your credit utilisation low (don’t max out your credit cards).

- Avoid applying for too many loans or credit cards simultaneously.

- Maintain a healthy mix of secured and unsecured loans.

- Increase Your Income Stability: Lenders love stability. A steady job, a good income-to-debt ratio, and a consistent employment history make you a less risky borrower. If your income has increased significantly since you took the loan, that’s a strong point to highlight when trying to negotiate with lender for a better rate or when refinancing.

- Reduce Other Debts: If you have multiple high-interest debts (like credit card outstanding), consider a debt consolidation loan. This can simplify your repayments and potentially lower your overall interest burden, making you a more attractive borrower for a personal loan refinance.

Building a robust financial profile is an ongoing process, but the rewards are substantial. It’s not just about lowering one loan’s rate; it’s about gaining control over your entire financial ecosystem. This dedication to financial health is paramount.

Strategy 3 | Smart Repayment Tactics & Negotiations

Sometimes, refinancing isn’t an option, or perhaps you just want to tackle your existing loan more efficiently. Here’s where smart repayment strategies come into play.

Tactics for Your Existing Personal Loan |

- Make Partial Prepayments: If you receive a bonus, an increment, or any unexpected lump sum, use a portion of it to make a partial prepayment on your loan principal. This directly reduces the amount on which interest is calculated, leading to significant savings over time. Always check for prepayment charges or penalties in your loan agreement first. Some loans have a lock-in period, or charge a fee for early payments. Make sure the savings outweigh the charges.

- Negotiate with Your Lender (Again!): If your financial profile has improved significantly since you took the loan, don’t hesitate to approach your existing bank. Present your case: “My credit score is now X, my income is Y, and I’ve been a loyal customer with a perfect repayment record. Can you review my personal loan interest rate and offer a reduction?” While not guaranteed, banks do sometimes offer rate reductions to retain good customers.

- Opt for a Shorter Tenure (If Refinancing): When you refinance, if your budget allows, choose a shorter repayment tenure. While your EMI might be slightly higher, the total interest paid will be substantially lower. It’s a trade-off, but often a smart one for long-term savings and achieving financial freedom faster. This is a key part of any effective loan repayment strategy.

- Automate Payments: This might sound basic, but automating your EMIs ensures you never miss a payment, protecting your credit score and avoiding late fees. Consistency is key in financial management.

Navigating the Pitfalls | What to Watch Out For

While the path to a lower interest rate is clear, there are a few potholes to avoid. The financial world, especially in India, can be tricky. Always read the fine print. Don’t get swayed by incredibly low “teaser rates” that might jump up later. Understand all fees involved – processing fees, late payment charges, and crucially, those prepayment charges . Sometimes, the cost of switching or prepaying can negate the benefits of a lower rate. Use an online calculator (like anauto loan calculator monthly payment, which shares similar principles for EMI calculations) to crunch the numbers before making any big decisions.

Also, beware of unsolicited offers. Always verify the legitimacy of the lender and the terms they offer. The Reserve Bank of India (RBI) provides guidelines for fair practices by lenders, and it’s always good to be aware of your rights as a borrower. This trust in official sources is paramount.

Frequently Asked Questions About Lowering Personal Loan Interest Rates

What is the easiest way to get a lower interest rate on my personal loan?

The “easiest” often depends on your current situation. For many, refinancing with a new lender after improving their credit score offers the most direct path to a significantly lower rate. Negotiating with your current bank is also worth trying.

Can I negotiate my personal loan interest rate after getting the loan?

Yes, absolutely! If your financial standing (credit score, income, repayment history) has improved since you took out the loan, you have a stronger bargaining chip. Gather evidence of your improved profile and approach your lender.

Does making extra payments reduce the interest on my personal loan?

Yes, making partial prepayments directly reduces your principal amount, which in turn reduces the total interest you pay over the loan’s tenure. Always check your loan agreement for any prepayment penalties first.

How much does my credit score affect my personal loan interest rate?

A lot! Your credit score is one of the most critical factors lenders use to assess your risk. A higher score (typically 750+) indicates lower risk, making you eligible for the most competitive personal loan interest rate offers.

Is a personal loan balance transfer always a good idea?

A personal loan balance transfer can be a great idea if it results in a substantially lower interest rate and lower overall cost, even after considering any processing fees. Always calculate the net savings before making the switch.

What if I cannot refinance or negotiate my existing loan?

If those options aren’t viable, focus on making partial prepayments whenever possible, even small amounts. Also, continue to improve your credit score and financial discipline for future financial opportunities. Every little bit helps your financial health .

The Bottom Line | Take Control

Ultimately, lowering your personal loan interest rate isn’t just about saving money (though that’s a huge perk!). It’s about regaining control over your financial narrative. It’s about empowering yourself with knowledge and taking proactive steps rather than passively accepting the status quo. It might require a bit of legwork – some research, a few phone calls, perhaps even some negotiation – but the payoff, both in rupees saved and in peace of mind, is absolutely worth it. So, go on, take that first step. Your wallet (and your stress levels) will thank you for it!