Let’s be honest, the daily news cycle on home loan interest rates today USA can feel like a dizzying rollercoaster. One day they’re up, the next they’re down, and it often leaves you wondering: what does any of this actually mean? Especially if you’re an Indian tracking the global economy, or perhaps an NRI considering property in the States, these numbers aren’t just statistics; they’re signals. But here’s the thing: merely reporting ‘rates are X today’ misses the entire point. What truly matters is understanding the ‘why’ behind the ‘what.’ Why are rates behaving this way? What are the implications for the broader US housing market ? And most importantly, what does it mean for your potential decisions?

My goal isn’t just to tell you what the rates are; it’s to pull back the curtain and show you the intricate dance of economic forces, policy decisions, and market sentiment that truly dictates these figures. Think of me as your knowledgeable friend, sitting across the table, explaining the complex interplay in a way that actually makes sense. We’re going to dive deep into the currents beneath the surface, exploring not just the numbers, but the narrative they’re telling about the American economy and, by extension, the world.

Beyond the Headlines | What’s Really Driving US Home Loan Rates Today?

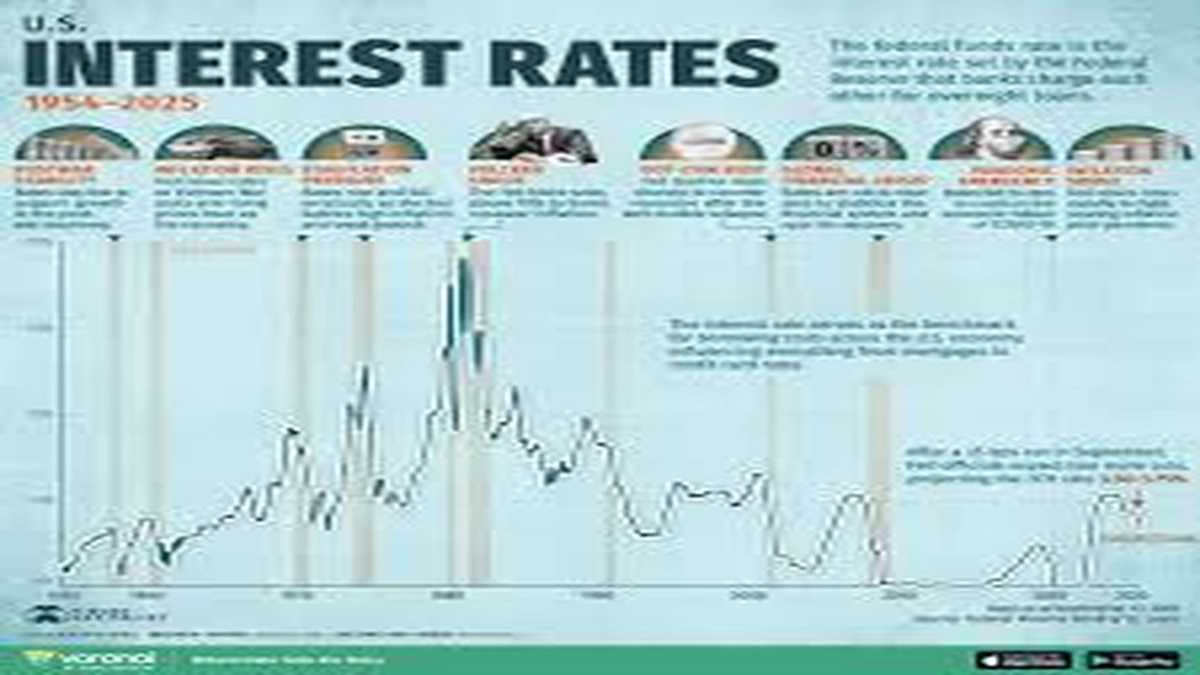

When we talk about home loan interest rates today USA , it’s easy to get caught up in the immediate fluctuations. But to truly grasp the picture, we need to look at the big players. The most significant force at play, without a doubt, is the Federal Reserve. While the Fed doesn’t directly set mortgage rates, its monetary policy decisions particularly changes to the federal funds rate send powerful ripples throughout the entire financial system. When the Fed raises its benchmark rate to combat inflation, as we’ve seen recently, the cost of borrowing for banks increases. Naturally, banks pass these higher costs onto consumers in the form of elevated lending rates, including those for mortgages. It’s a classic cause-and-effect scenario, though often delayed and nuanced.

But it’s not just the Fed. Inflation itself plays a massive role. Lenders need to ensure that the return on their loans outpaces the rate at which money loses its purchasing power. So, if inflation is high, mortgage rates tend to follow suit. Then there’s the bond market, specifically the yield on the 10-year Treasury note. This yield is often seen as a bellwether for current mortgage rates USA . Why? Because many mortgage-backed securities are priced off this benchmark. When bond yields rise, mortgage rates typically head north as well. It’s a complex ecosystem, but understanding these core drivers – Federal Reserve policy , inflation, and bond market movements – gives you a much clearer lens through which to view the daily rate announcements. What fascinates me is how interconnected these elements are, creating a dynamic environment where even small shifts in one area can have noticeable impacts on what you pay for your home loan.

The 30-Year Fixed | A Benchmark, Not a Dictator

When you hear about US mortgage rates in the news, more often than not, they’re referring to the average rate for a 30-year fixed mortgage rates . This is the gold standard, the benchmark that most buyers in the US aspire to, offering predictable monthly payments over three decades. It’s a powerful tool for budgeting and long-term financial planning. However, it’s crucial to remember that this is just one type of loan. The mortgage market is a diverse landscape, offering a variety of products tailored to different financial situations and risk tolerances.

For instance, adjustable-rate mortgages (ARMs) start with a lower interest rate for an initial period (say, 5 or 7 years) before adjusting periodically based on a market index. These can be attractive if you plan to sell or refinance before the adjustment period, or if you believe rates will fall in the future. Then there are government-backed loans like FHA (Federal Housing Administration) loans, designed for borrowers with lower credit scores or smaller down payments, and VA (Department of Veterans Affairs) loans, offering exceptional benefits to eligible service members and veterans. Jumbo loans cater to borrowers seeking mortgages above conventional loan limits. Each of these comes with its own set of rules, eligibility criteria, and, of course, interest rates. So, while the 30-year fixed mortgage is a great barometer, your personal best rate might come from an entirely different product. It’s about finding the right fit, not just chasing the lowest advertised number.

Decoding the US Housing Market | What It Means for You (or Your Friends Abroad)

The trajectory of home loan interest rates today USA is inextricably linked to the broader health and direction of the US housing market trends . When rates climb, borrowing becomes more expensive, which naturally cools buyer demand. This can lead to a slowdown in home sales, and in some cases, a moderation in home price appreciation. Conversely, lower rates can ignite a buying frenzy, driving up competition and prices. We’ve seen both extremes in recent years, making it a truly fascinating, if sometimes frustrating, market to observe.

For many, particularly first-time buyers or those looking to expand, the concept of housing affordability has become a significant hurdle. High interest rates coupled with already elevated home prices create a double whammy, pushing monthly mortgage payments beyond the reach of many households. This challenge isn’t just a local issue; it has broader economic implications, impacting everything from consumer spending to labor mobility. If you’re an Indian considering an investment property in the US, or helping family members navigate a purchase, understanding these dynamics is paramount. It’s not just about the cost of the loan, but the overall market environment – inventory levels, regional economic strength, and future growth projections – that will ultimately determine the wisdom of your investment. For a deeper dive into the broader economic landscape, consider exploring resources like theFederal Reserve’s official website, which offers detailed insights into monetary policy and economic data.

Is This the Time to Buy, Sell, or Refinance? Navigating the Rate Maze

With home loan interest rates today USA constantly shifting, the perennial question arises: is this the right time for a major housing move? The answer, frustratingly, is rarely simple and almost always depends on your individual circumstances. If you’re buying, current rates will dictate your purchasing power and monthly payments. A higher rate might mean you need to adjust your budget, look for a smaller home, or consider a different neighborhood. But it’s not just about the rate in isolation; it’s about your long-term financial goals, job security, and personal comfort level with debt.

For homeowners, the question of whether torefinance home loanis often top of mind. If you secured a mortgage when rates were significantly higher, a dip in current mortgage rates USA could present an opportunity to lower your monthly payments or change your loan terms. However, refinancing involves closing costs, so you need to crunch the numbers to ensure the savings outweigh the expenses. I’ve seen people make the mistake of chasing every fractional rate drop without considering the long-term impact of closing costs. It’s a strategic decision that requires careful calculation. Furthermore, don’t just go with the first offer; compare rates and terms from multiple mortgage lenders US to ensure you’re getting the best deal. Online tools and local brokers can be invaluable in this process. Remember, your home is likely your biggest asset, so treat these financial decisions with the strategic thought they deserve.

Your Burning Questions About US Home Loans, Answered

What exactly influences home loan interest rates today USA?

Primarily, the Federal Reserve’s monetary policy, inflation rates, and the yield on the 10-year Treasury bond are the biggest drivers. Global economic events and lender competition also play a role.

Are these rates good for first-time buyers?

Good is subjective! While rates might not be at historic lows, waiting indefinitely can be risky. Focus on what you can afford, and explore programs like FHA loans that often assist first-time buyers. It’s more about your personal financial readiness than chasing a ‘perfect’ rate.

Should I wait for rates to drop further?

Predicting interest rate movements is notoriously difficult. While many hope for lower rates, there’s no guarantee. Waiting means potentially missing out on current inventory or seeing home prices rise further. It’s a balance between timing the market and securing a home you love now.

How do I find the best current mortgage rates USA?

Shop around! Don’t just rely on one bank. Contact multiple mortgage lenders, both traditional and online, and compare their offers. Also, ensure your credit score is in good shape, as this significantly impacts the rates you qualify for.

What’s the deal with adjustable-rate mortgages (ARMs)?

ARMs offer a lower initial rate for a set period (e.g., 5 or 7 years) before adjusting periodically based on a market index. They can be a good option if you plan to sell or refinance before the adjustment, but they carry the risk of higher payments later if rates rise.

Can NRIs get US home loans?

Yes, absolutely! NRIs can indeed secure home loans in the US, though the process might involve additional documentation and potentially different lending criteria. It’s best to consult with lenders specializing in international borrowers or those with experience working with non-resident aliens. You might find some helpful insights when considering various financial options, such as understanding collateral requirements, which are also relevant for other types of loans like agold collateralbased loan.

So, there you have it. The world of home loan interest rates today USA is far more dynamic and intricate than the headlines often suggest. It’s not just about a single number, but a complex interplay of economic forces, policy decisions, and personal circumstances. By understanding the ‘why’ behind the ‘what,’ you’re not just a passive observer; you become an informed participant, better equipped to make decisions that truly serve your financial future. Remember, knowledge isn’t just power; it’s peace of mind in a volatile market.